Here are the latest developments in global markets:

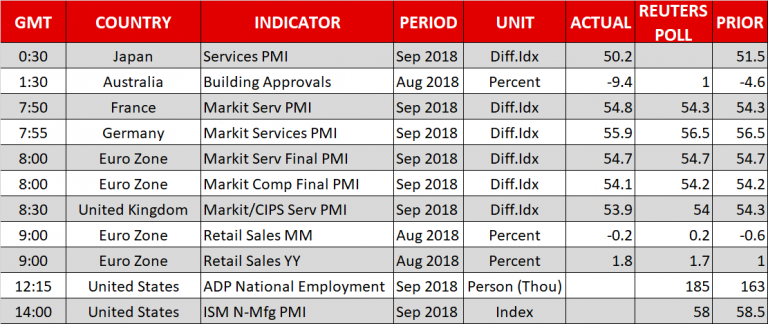

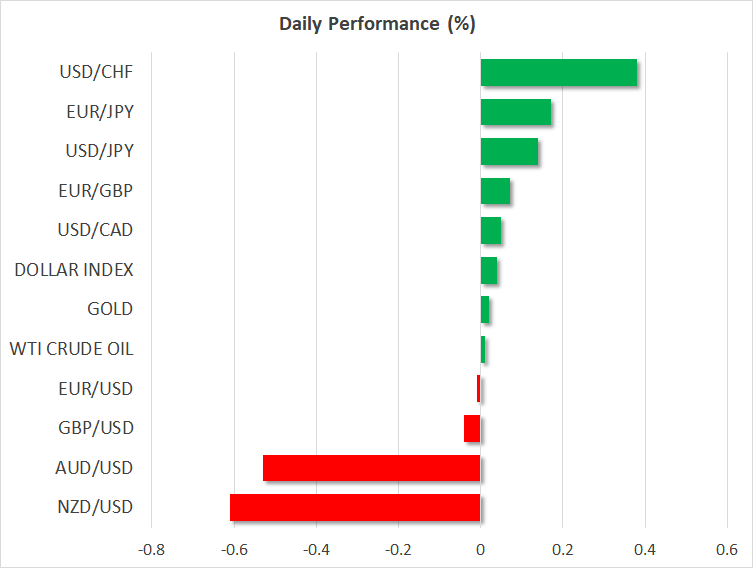

- FOREX: The common currency crawled up on Wednesday from six-week lows on news that the final version of Italy’s budget deficit could be less worse than originally reported. Government sources signalled possible reductions to the deficit targets in 2020, 2021, according to reports. Earlier today, retail sales in the Euro area dropped by 0.2% m/m in September from a downwardly revised 0.6% decline in the previous month, missing market expectations of a 0.2% gain. It was the second consecutive month of decrease in retail sales. In other data, the final IHS Markit Eurozone Services PMI was confirmed at 54.7 in September in line with preliminary estimates but slightly higher than the 54.4 mark reported in August. A downward surprise however was identified in the German services PMI which ticked down to 55.9 in September versus the forecast of 56.5. Following the data, euro/dollar continued to weaken towards 1.1543 (-0.02%), reversing earlier gains. Turning to the UK, the British Prime Minister, Theresa May, said during her speech at the Conservative Party Conference that a no-deal Brexit would be a bad outcome for both the EU and the UK, but the British government is not afraid to leave the bloc without an agreeement. In the wake of her comments, pound/dollar slipped as low as 1.2961 before inching up to 1.2973 (-0.02%). Prior May’s remarks, the UK IHS Markit services PMI for the month of September added some pressure to the pound as the indicator appeared lower than expected at 53.9 compared to 54.3 in the previous month and 54.0 forecasted. Dollar/yen was set to recoup yesterday’s losses trading below 114.00 at 113.77 (+0.11%), while dollar/loonie was struggling to recover, gaining 0.08% in the day. In monetary policy-related news, Chicago Fed President Charles Evans admitted that the US central bank is more comfortable with inflation than in previous years and appeared positive with regards to additional rate hikes to come, reiterating a gradual pace. In the antipodean sphere, aussie/dollar and kiwi/dollar slipped to two-week lows, losing 0.53% and o.61% respectively.

- STOCKS: European equities moved higher on Wednesday as investors kept an eye on Italian politics and the government’s spending plans. The pan-European Stoxx 600 was 0.59% higher with every sector in positive territory, while the blue-chip Euro STOXX 50 rose by 0.77% at 1200 GMT. The UK FTSE 100 climbed by 0.64%, the French CAC 40 increased by 0.70%, while the Italian FTSE MIB surged up by 1.11%. Futures tracking US indices such the S&P 500, Dow Jones and Nasdaq 100 were slightly up, pointing to a softer positive open. Note that German markets will be closed on Wednesday for a public holiday.

- COMMODITIES: Oil prices were moving sideways slightly below 4-year highs posted on Tuesday. West Texas Intermediate (WTI) crude and Brent were last seen at $75.27/barrel and $84.84 respectively. In precious metals, gold jumped marginally above the $1,200/ounce level (+0.02%) as the dollar softened.

Day Ahead: ADP employment report & ISM non-Manufacturing PMI next in focus; Italian budget eyed

The ADP employment report will display the number of job positions added to the US private sector in September at 1215 GMT with investors waiting for some clues ahead of the all-important Nonfarm payrolls Job statement due on Friday. According to analysts, the number of employees in the non-farm private sector increased by 185k compared to a rise of 163k in August. While an upward surprise could lift the dollar higher, that cannot be a guarantee that Friday’s NFP hiring will be more encouraging as well since the reports are not as strongly in sync as in the past.

A few hours later at 1400 GMT, the ISM non-manufacturing PMI for the month of September could be another market mover for the greenback. Forecasts are for the index to slow down by 0.5 points to 58, though that may not be much of a worry given that any mark above 50 indicates an expanding industry.

Staying in the US, the Energy Information Administration will publish data on US oil inventories for the week ending September 28 at 1430 GMT, probably bringing a fresh wave of volatility to oil prices. Predictions support an increase of 1.98 million barrels in crude stocks from a 1.85mn rise seen previously. Gasoline stocks are expected to build up too but less than in the previous week, whereas distillate inventories are projected to post a softer decline.

Elsewhere, the Australian Bureau of Statistics will update Australia’s trade figures at 0130 GMT on Wednesday, with analysts seeing the positive trade balance easing for the second straight month to A$1.40 billion in August. In July, the trade surplus stood at A$1.55bn.

Meanwhile, in the EU, the Italian budget story will continue to keep investors on toes. On Tuesday headlines showed that the Italian government is not planning to change its budget plans, which aim for a public deficit of 2.4% of GDP for the next three years. Today,however, the Italian Deputy Prime Minister, Luigi Di Maio revealed that Rome is considering lowering its deficit targets after 2019, with some official sources stating that these could drop to 2.2% and 2.0% in 2020 and 2021 respectively. This indicated that Italy is willing to appease its EU counterparts who claimed that the country’s budget goals deviated significantly from earlier commitments.

In terms of public appearances, several Fed policymakers are scheduled to speak later today, with the Fed chairman Jerome Powell attracting the most interest at 2000 GMT. Separately, remarks by Richmond Fed President, Thomas Barkin (FOMC voter, 1205 GMT), Philadelphia Fed President, Patrick Harker (non-voter, 1715 GMT), St. Louis Fed President, James Bullard (non-voter, 1800 GMT) , Cleveland Fed President, Loretta Mester (voter, 1815 GMT) and Fed Board Governor, Lael Brainard (permanent voter, 1800 GMT) will gather interest. Dallas Fed President, Robert Kaplan will be also commenting at midnight.

Chinese markets will remain closed for the rest of the week due to a public holiday.