Wednesday May 10: Five things the markets are talking about

There are a number of moving parts that are currently keeping capital markets on their toes – China, ECB, Fed, N. Korea, Trump and OPEC.

Investors have been extra focused on China after a selloff erased at least -$500B from the value of stocks and bonds since mid-April, amid policy makers’ moves to crack down on leverage. Data overnight showed that prices slowed more than expected (see below).

When is the ECB going to start rate normalization? They have to get their timing correct. Today’s ECB unemployment figures support the case for ongoing stimulus. A broader measure of regional unemployment shows that around +15% of eurozone workers are "unemployed or underemployed," which suggests wages and inflation are unlikely to pick up for some time. A June Fed hike is almost fully priced in.

North Korea says it’s going ahead with its sixth nuclear test, who is pulling the strings?

President Trump fires FBI Director Comey, citing his handling of the investigation into Hillary Clinton’s email server – what’s the impact on the FBI probe into possible ties between the Trump campaign and Russia?

OPEC still does not have a consensus to maintain last November’s production cuts into H2, 2017. But, is it coming soon?

1. Global bourses see mixed results

Overnight, Asian stocks resumed a rally as Hong Kong shares jumped to a two-year high, while European shares are mixed and U.S futures see red as President Trump fired FBI Director James Comey.

In Hong Kong, the Hang Seng rose +0.5%, to its highest level since July 2015. The Hang Seng China Enterprises Index jumped +0.9%, rallying for a third consecutive day, while the Shanghai Composite Index retreated -0.9% to its lowest level since October.

In Japan, the broader Topix index increased +0.2% and the Nikkei 225 rose +0.3%. Gains were limited by yen’s rally overnight on tentative ‘risk aversion’ trading (¥113.83).

In South Korea, the Kospi slid -1% after surging +2.3% on Monday, the most since September 2015.

In Europe, indices are trading mixed this morning with notable weakness in the Swiss SMI and out-performance in the FTSE on energy prices. Corporate earnings look set to dominate the Eurostoxx 600.

U.S stocks are set to open in the red (-0.2%).

Indices: Stoxx50 -0.3% at 3640, FTSE +0.1% at 7347, DAX -0.1% at 12742, CAC-40 -0.2% at 5388, IBEX-35 -0.6% at 10985, FTSE MIB -0.4% at 21398, SMI -0.8% at 9047, S&P 500 Futures -0.2%

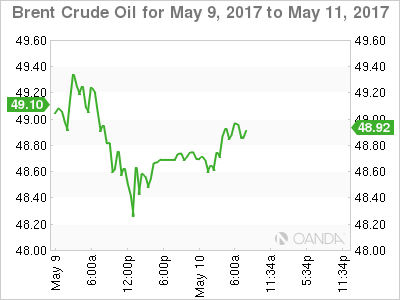

2. Crude oil prices find support on potential cut extension, gold higher

Ahead of the U.S open, oil prices are on the rise on rumoured reports that Saudi Arabia would cut supplies to the region. Prices are also supported by a larger than expected fall in yesterday’s API crude inventories last week, down -5.8m barrels compared with market expectations for a -1.8m barrels decline.

Brent futures are up +19c, or +0.4%, at +$48.92 a barrel – they fell -1.2% yesterday. U.S West Texas Intermediate (WTI) crude is up +23c, or +0.5%, at +$46.11 a barrel.

Note: WTI also fell -1.2% Tuesday, and the closing price for both contracts was the second lowest since Nov. 29, the day before OPEC agreed to cut production during H1, 2017.

There are reports this morning that State-owned Saudi Aramco will reduce oil supplies to Asian customers by about -7m barrels in June, as part of OPEC’s agreement to reduce production.

Capping price gains is higher crude output from the U.S, particularly shale producers.

Note: U.S crude production is expected to rise by more than previously expected in 2017 to +9.31m bpd from +8.87m bpd in 2016.

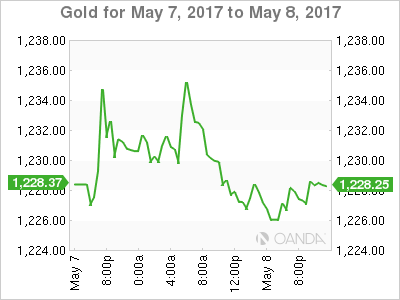

Gold (+0.2% at +$1,223.30 an ounce) has edged off the previous day’s two-month low this morning as U.S President Trump’s abrupt firing of FBI chief James Comey hit equities, but expectations of further Fed rate hike is likely to limit gains by the metal.

3. Global yields little changed, focus on Central Banks

With Euro go-political risk abating somewhat since the weekend, dealers and investors are returning to fundamentals and central bank monetary policy for guidance.

The markets main focus is on the Fed and the ECB. The current odds for a Fed hike next month are +83%, however, for Draghi, the question is not about rate hikes, but about reducing stimulus.

Central banks may be best placed to understand other central banks, and if so, the ECB is not expected to be winding down its stimulus programs anytime soon. According to today’s minutes from its April policy meeting, Sweden’s Riksbank expects the "ECB to continue to pursue a very expansionary monetary policy in the foreseeable future." And it’s for this reason why the Riksbank is prepared to extend its own bond-buying program to the end of 2017.

Yields on eurozone government bonds are declining slightly in early Wednesday trading, but a major drop seems unlikely due to supply of new debt this week. Not only are sovereigns, including Germany, in the market to place new debt, but so to are agencies. German 10-year Bunds yields have fallen -1 bps to +0.43%.

Elsewhere, the yield on 10-year Treasury notes fell -1 bps to +2.39%, while Australian 10-year yields dropped -3 bps to +2.66%.

Note: The Bank of England (BoE) publishes its interest-rate decision and quarterly Inflation Report Thursday.

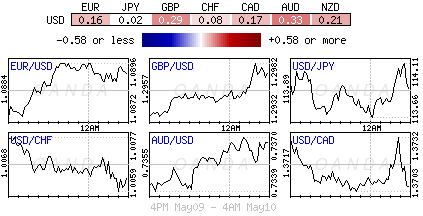

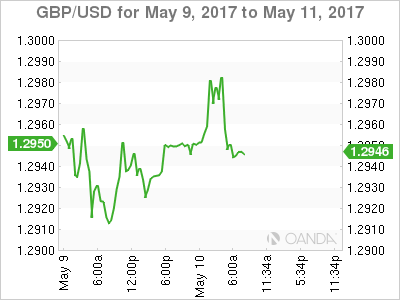

4. Sterling hovers atop key resistance, a break could trigger more gains

Ahead of the U.S open, the pound trades up +0.37% at £1.2983 outright, hovering just below the psychological £1.30 handle, a level not traded in eight-months.

Of late, sterling has been benefitting as "weaker short-positions" are been forced to close out. Ahead of the BoE rate announcement and inflation quarterly report tomorrow, do not be surprised to see more positions unwind ahead of time.

Any hints from Governor Carney that they are considering raising rates would be sterling positive. More market stop-loss orders could be executed when £1.3000 is finally breached with momentum.

Elsewhere, the FX markets saw little volatility in the session. A slightly softer USD was attributed to President Trump’s firing of his FBI director, the yen (¥113.83) found some support, while the EUR continues to hover just under the psychological €1.09 area (€1.0873).

5. China CPI rises to 3-month highs while PPI growth slows

China inflation data has also propped up sentiment, with Consumer Price Index rising to three-month highs and beat market expectations on a month-over-month (+0.1% vs. -0.3% prior) and year-over-year basis (+1.2% vs. +1.1%e).

Note: The main driver of the pick-up was an increase food price inflation, which rose from -4.4% y/y to -3.5% on the back of pick-ups in fruit and vegetable price inflation. Non-food inflation also edged up from 2.3% y/y to 2.4%, but this was largely due to a seasonal increase in tourism cost inflation.

China’s Producer Price Index (+6.4% vs. +6.7%e) was positive for the eight consecutive month, but the rate of increase was smallest in four-months as the recent free-fall in metal prices is also reflected in the results.

Note: The driver was a drop in industrial commodity prices, with factory gate prices declining most among steel and oil producers.