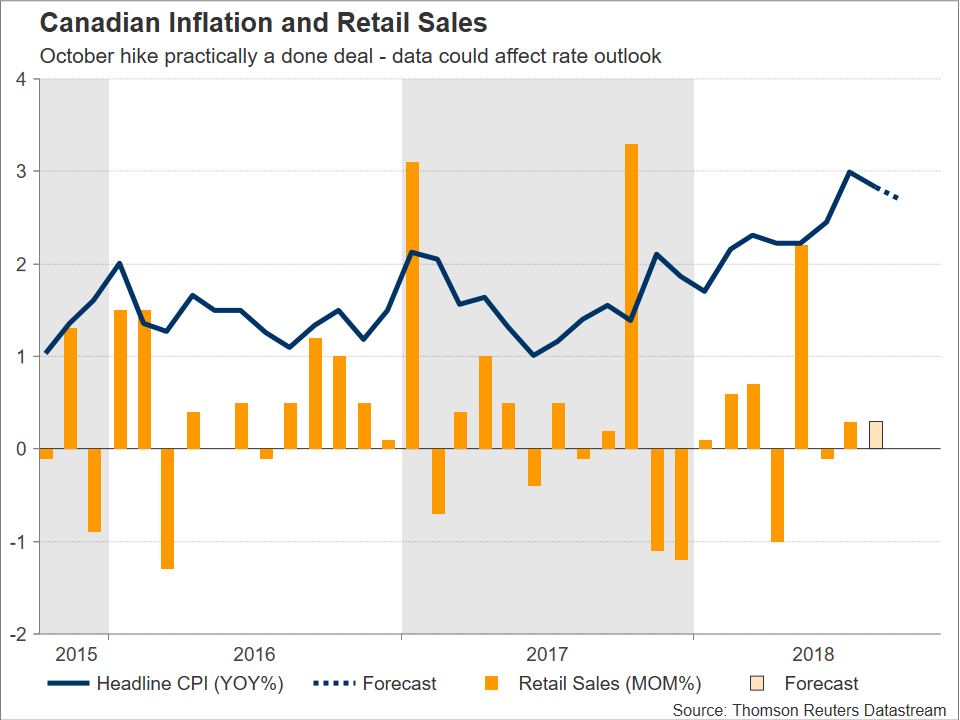

Canadian inflation and retail sales figures for September and August correspondingly will be hitting the markets on Friday at 1230 GMT. Barring a dramatic deviation from expectations, the data are unlikely to deter the Bank of Canada from hiking rates during its policy meeting next week. They can, however, affect the market’s perception on the steepness of the central bank’s rate path moving forward.

Inflation as gauged by the consumer price index (CPI) is projected to exhibit zero growth on a monthly basis after contracting by 0.1% in August. This would translate to an annual rate of 2.7%, slightly below August’s 2.8%. If the reading comes in line with forecasts, headline inflation would drift further away from July’s 3.0% y/y rate, which was the fastest rate of expansion since September 2011. Still, this would constitute the eighth straight month that the measure would exceed the BoC’s target for annual inflation of 2.0%, at the same time remaining within the upper bound of the 1-3% target band.

Higher energy prices were largely to ‘blame’ for the rise in headline CPI at current levels. Thus, the Canadian central bank may instead decide to focus on underlying price pressures when setting policy, namely on core CPI that excludes energy from its calculations. That stood at 1.7% y/y in August, matching a high last experienced in February 2017. Additionally, the three measures of core inflation monitored by the BoC – CPI median, trim and common – have proved market moving in the past and are worth monitoring. The three came in at 2.1%, 2.2% and 2.0% y/y respectively in August. In terms of projections, CPI common is expected to hold at the 2.0% y/y rate, with no polls available for the other gauges of core inflation.

Turning to retail sales, Friday’s other important release, they’re anticipated to expand by 0.3% m/m in August, the same as in the previously reported month. Meanwhile, core retail sales that exclude automobiles, are predicted to grow by 0.2% m/m, much lower than July’s 0.9% pace.

Canadian OIS put the probability for an October 24 quarter percentage point rate rise by the BoC close to 90%, in other words it is roughly seen as a done deal. The upcoming data, however significant, are unlikely to shift the central bank’s thinking away from a rate rise next week, especially in light of other releases pointing to a relatively strong economy and uncertainty over a new North American trade deal being lifted. What they may achieve though, is affect rate expectations moving forward. Particularly, markets see another interest rate increase (beyond next week’s) in March 2019. Encouraging prints may push the timing for that closer in time, and vice versa. It is worth noting that Monday’s quarterly business outlook survey by Canada’s central bank was on the optimistic side of the spectrum.

For the record, the BoC has delivered four 25bps rate increases since July 2017, with the Fed delivering twice as such moves since it began its own normalization cycle in late 2015.

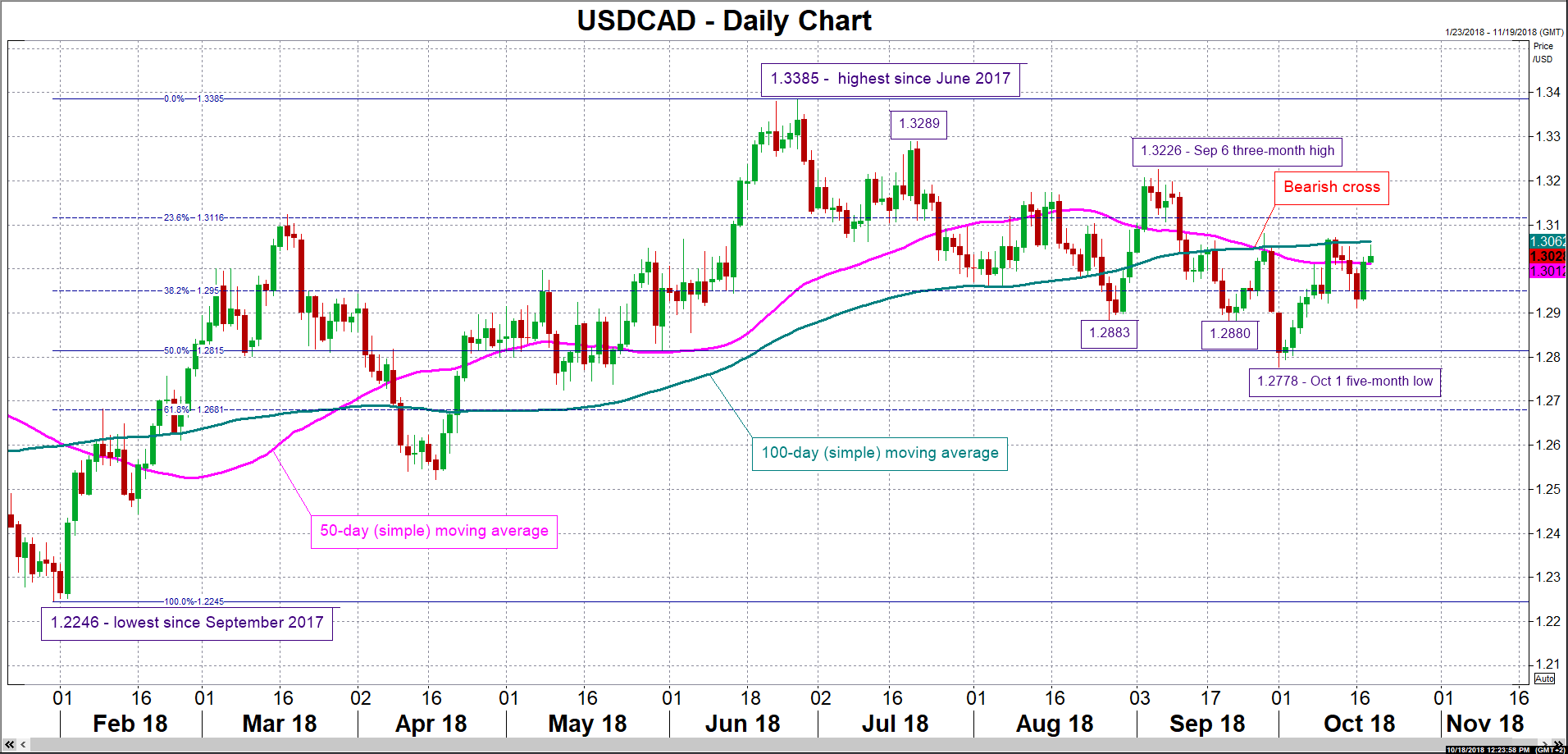

In FX markets, upbeat Canadian prints are expected to lift the loonie. At the moment, immediate support to a declining USDCAD seems to be occurring around 1.3012, the current level of the 50-day moving average line. Further below, support could come from the area around 1.2950, which is the 38.2% Fibonacci retracement level of the upleg from 1.2246 to 1.3385. Lower still, the zone around 1.2880 that captures a couple of bottoms from the recent past and which was congested earlier in the year would come into scope, with steeper losses shifting the attention to the 50% Fibonacci mark at 1.2815. Conversely, disappointing figures are likely to be met with long USDCAD positions. A first line of resistance could take place around the 100-day MA at 1.3062. Not far above lies the 23.6% Fibonacci point at 1.3116, with an upside violation turning the focus to early September’s three-month high of 1.3226.

Lastly, despite oil prices and the loonie being far from perfectly correlated, on occasion their positive relationship comes to the fore; Canada is a major oil exporting power. In this sense, it is worth paying attention to crude prices as yet another factor that may determine the short-term direction in USDCAD. Inventory data, US sanctions on Iranian oil exports kicking in in early November and the US-Saudi discord over missing journalist Khashoggi are some of the themes at play in energy markets.