Here are the latest developments in global markets:

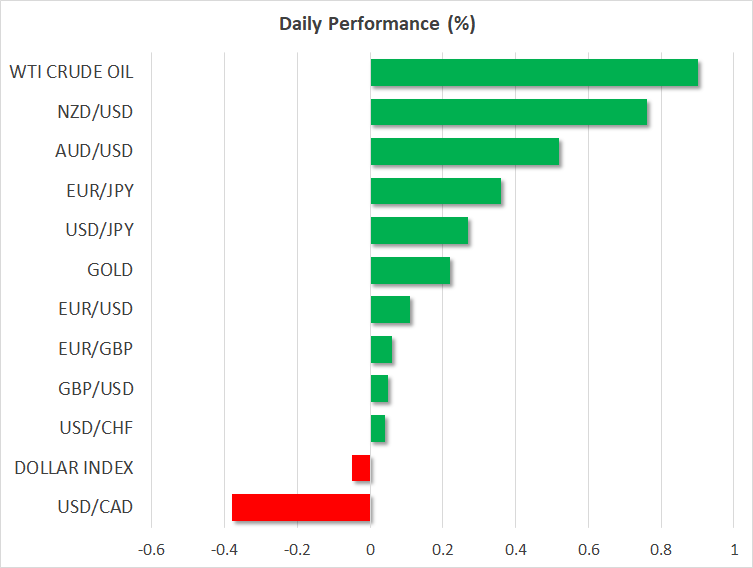

- FOREX: The euro reached a new 10-day low at 1.1431 against the US dollar earlier on Friday after the European Commission sent a cautionary letter to Italy over the submitted draft of their budget plan. However, euro/dollar managed to pare its losses, rising by 0.10% to 1.1462 later in the day, while euro/yen improved as well, jumping by 0.23% on the day. Pound/dollar moved slightly higher by 0.09% earlier today after European Union negotiator Michel Barnier said that a Brexit deal is very close even if the EU summit failed to provide any significant progress, but oppositions over the Brexit plan in the UK kept gains limited. Pound/yen was in a better position, adding more than 0.20% to its performance. Dollar/yen jumped by 0.28%, holding above the 112.00 handle. The antipodeans currencies were in bullish mode after two consecutive red days despite disappointing GDP growth figures out of China. Aussie/dollar traded up by 0.56% at 0.7118, while kiwi/dollar edged higher by 0.66% to 0.6586. Meanwhile, dollar/loonie was down by 0.37% at 1.3037 ahead of Canadian inflation and retail sales data later today.

- STOCKS: European stocks were mostly on the downside on Friday amid rising fears that the Italian budget could fail to get an approval from the EU, while discouraging earnings results from Michelin and Bouygues weighed on construction and auto equities. The benchmark European STOXX 600 tumbled by 0.46% for the third day in a row, whereas the blue-chip Euro STOXX 50 was up by 0.11% on the back of consumer non-cyclicals and utilities. The German DAX 30 dropped by 0.33%, the French CAC 40 dived by 0.89% and the Spanish IBEX 35 slipped by 0.81%. The British FTSE 100 increased by 0.16%. In Asia, Japan’s Nikkei 225 and Topix closed lower. In the US, even though the S&P, Dow Jones and the Nasdaq all plunged yesterday, futures tracking these indices are currently in the green, pointing to a higher open today.

- COMMODITIES: Oil prices recovered from one-month lows after China’s GDP growth slowed down more than analysts expected in the third quarter, raising fears that oil demand from the world’s largest oil importer might stall. In other news ,sources with knowledge shared that OPEC/non-OPEC compliance with the supply pact stood at 111% in September, above the 129% mark in August. Yet crude markets were set to finish lower for the second straight week. WTI and Brent crude were on the upside at $69.16 and $80.10 per barrel respectively. In precious metals, gold climbed by 0.19% to trade around $1,227 per ounce.

Day Ahead: Canada reports on inflation and retail sales; Italy’s budget to weigh on sentiment

Canada is expected to deliver key data releases later on Friday as the central bank prepares to raise interest rates next week for the third time this year. The conflict between Italy and the European Union will continue to feed risk-off sentiment in the eurozone, while political conditions in the UK will be closely monitored as some Conservative and Labour lawmakers look unhappy with May’s Brexit plans.

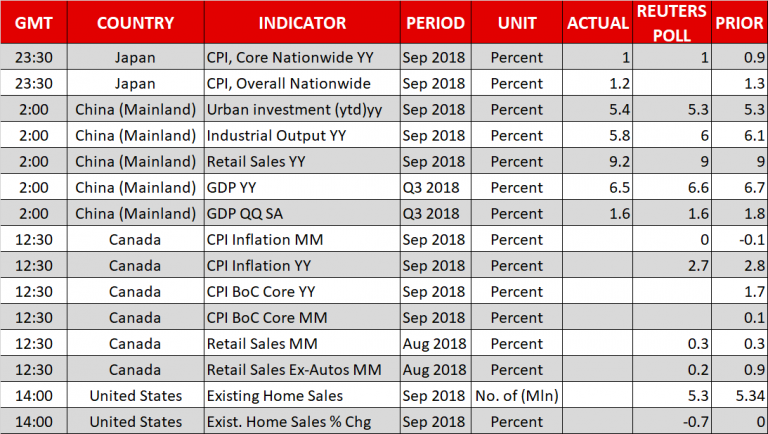

At 1230 GMT, Statistics Canada is projected to show that year-on-year the Consumer Price Index retreated to 2.7% in September, down from 2.8% in August and lower than the 3.0% peak in July. The modest slowdown however might not be much of worry to policymakers as long as the measure holds above Bank of Canada’s 2.0% midpoint target, while core measures fluctuate near that threshold. Note that the Bank of Canada anticipates the headline CPI to return towards 2.0% in early 2019 as the effect from higher oil prices is projected to fade.

Separately, Canadian retail sales growth for the month of August is said to have steadied at 0.3% m/m. Yet in the absence of automobile items, the core equivalent is seen easing by 0.7 percentage points to 0.2% m/m.

In the aftermath, an upside surprise in the data is highly likely to boost odds for a rate hike next Wednesday, with the loonie probably jumping on the news as well. Overnight indexed swaps are currently giving a 98.5% probability for a 0.25 bps rate rise by the BoC next week. Yet loonie traders will be also be monitoring crude prices as any potential fluctuations in the oil market may affect the currency’s performance. Note that Baker Hughes is due to report on US oil rig counts at 1700 GMT.

In the US, September’s existing homes sales will come into light at 1400 GMT, with analysts estimating a decline of 0.7% versus 0.0% in August. Still investors could shrug off the data and turn focus to trade after Chinese GDP growth figures proved that expansion in the world’s second biggest economy weakened for the third consecutive quarter to levels not seen since the first quarter of 2009. An evidence that US trade tariffs might have started to affect the country’s economic performance at a time when the government is focusing its efforts on deleveraging the economy. Industrial production figures also appeared discouraging, though Chinese stocks managed to rebound from earlier losses to close in the positive territory instead.

Meanwhile in Turkey, investigations around the disappearance of the Saudi Washington Post journalist continue, with the US President saying that consequences to Saudi Arabia could be “very severe” if the nation is found to have ordered the death of the journalist. The remarks followed the return of the Secretary of State Mike Pompeo from Ankara and Riyadh.

Elsewhere, the climate surrounding Italy’s fiscal demands turned more toxic after the European Commission sent Rome a notice, warning that the government’s spending plans seem to be in “particularly serious non-compliance” with EU regulations as they “unprecedently” deviate from targets. Italy which continued to back its fiscal plans today despite the EU’s objections, has to respond by Monday.

In terms of public appearances, Bank of England Governor Carney will be speaking at the Economic Club of New York at 1530 GMT. Later at 1445 GMT, Dallas Fed President Robert Kaplan, a non-voting FOMC member in 2018, will be talking on the state of monetary and fiscal policy in New York. On Saturday at 1500 GMT Atlanta Fed President Raphael Bostic will be participating in armchair discussion on the economic outlook, in Macon.