Here are the latest developments in global markets:

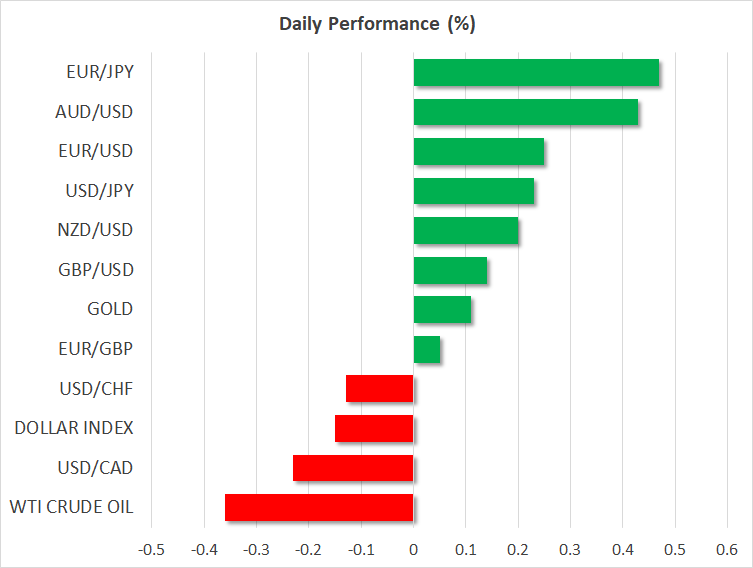

FOREX: The dollar index dropped significantly on Thursday and is a little lower on Friday too (-0.15%). The world’s reserve currency likely suffered as investors locked in profits on their prior dollar-long bets, ahead of the all-important US employment data today. Meanwhile, the British pound skyrocketed, gaining around 2% against the dollar, amid growing optimism that a Brexit deal is inching closer. The antipodeans aussie and kiwi also soared, probably as some of the massive short bets on both currencies were flushed out.

STOCKS: Wall Street climbed for a third session, buoyed by hopes that the US and China may restart trade talks. Both the S&P 500 and the Dow Jones gained 1.06%, while the Nasdaq Composite rose by 1.75%. The positive sentiment lingered, as futures tracking the S&P, Dow, and Nasdaq 100 are all pointing to a much higher open today. Asia was a sea of green on Friday too, with the Hang Seng in Hong Kong surging by an astonishing 4.05%, while South Korea’s Kospi 200 soared by 3.65%. In Europe, all the major indices were set to open notably higher , according to futures markets.

COMMODITIES: Oil plunged despite the recovery in risk sentiment. The drop was fueled by news the US government granted eight countries waivers from its sanctions on Iran. Meanwhile, signs the US is releasing some of its Strategic Petroleum Reserves ahead of the midterm elections, coupled with data indicating higher output from OPEC lately, amplified the losses. WTI touched a seven-month low of $63.45 per barrel, and Brent a two-month trough of $72.80 a barrel. In precious metals, gold took advantage of the sizeable correction lower in the dollar yesterday to recover some of the ground it lost recently, currently trading at $1,234 an ounce.

Major movers: Pound bulls go into overdrive; dollar crumbles amid massive profit-taking

Sterling skyrocketed on Thursday, as speculation that the Brexit talks are set to progress was reinvigorated, following new reports the EU is considering a compromise that would give the UK guarantees no customs border will be needed along the Irish sea. The currency barely reacted to the BoE rate decision, given the absence of fresh policy signals and the little-changed economic forecasts. Brexit headlines will likely remain the dominant force in driving the pound until a deal is clinched, at which point the focus will turn to whether the UK Parliament will actually approve it. The ball is now in the UK’s court, sort of speak, as markets will be awaiting to see how PM May will react to this new proposal.

The pound’s gains came mostly at the expense of the US dollar, which probably fell victim to some massive profit-taking after a very strong run higher recently, and ahead of the US employment report today. Additionally, tweets by President Trump that he “had a long and very good conversation” with Chinese President Xi Jinping may have led investors to unwind some of their haven bets on the greenback, amid signs that trade talks may restart soon. A disappointing ISM manufacturing PMI for October probably didn’t help either.

Meanwhile, the antipodeans aussie and kiwi rallied, with several potential catalysts behind the moves. First and foremost is that a short-squeeze likely took place, considering the massive net-short speculative positioning on both currencies, according to CFTC data. Then, there was the risk-on environment, amid positive signals on the trade front. An alternative explanation is that the strong trade surplus Australia reported recently sparked speculation China is buying more goods from the antipodeans, after the US imposed tariffs. Paradoxically, it follows that if Australia and New Zealand are the sellers China starts purchasing even more goods from, then those economies could even benefit somewhat from the US-China trade row.

Day ahead: US and Canada on the receiving end of employment figures; Sino-US trade developments eyed

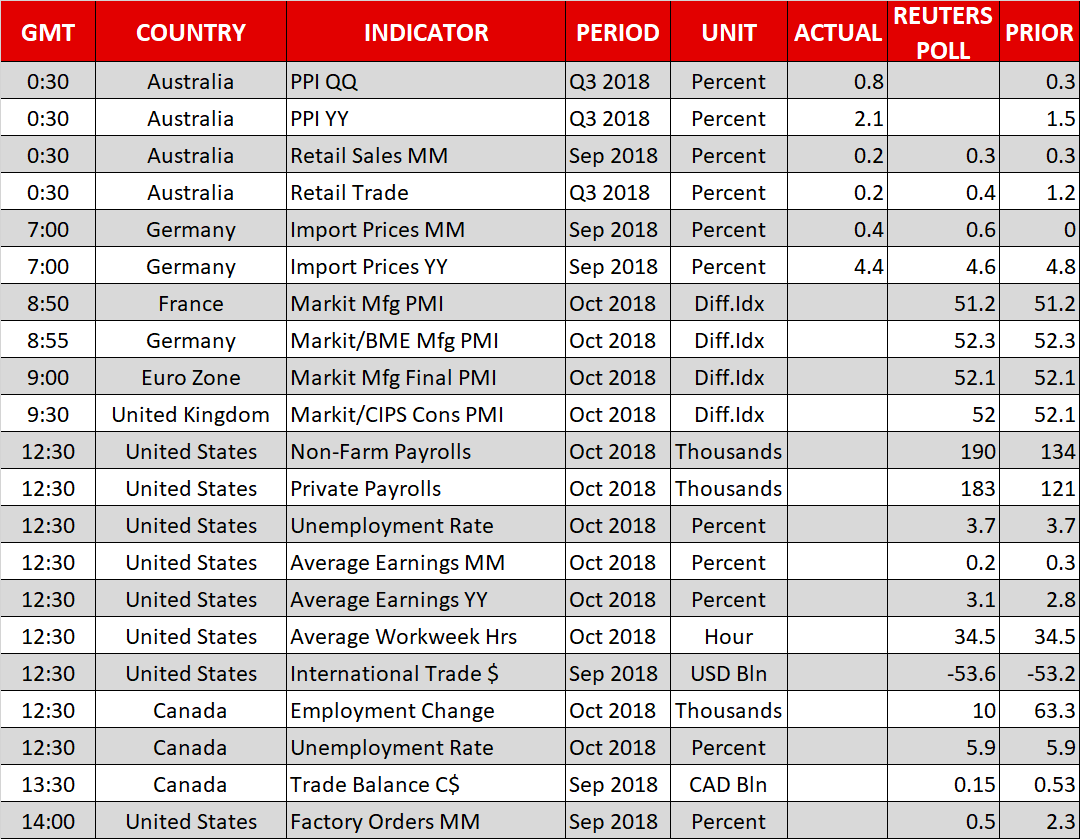

Undoubtedly the most important release on Friday’s calendar is the US employment report for October. Elsewhere, trade developments will be in focus as well, especially on the back of news that raised hopes for a de-escalation in tensions between the US and China.

The final reading on eurozone’s manufacturing PMI for October is due at 0900 GMT. With markets positioning accordingly upon the release of the preliminary estimates, which tend to be reliable, this is not expected to be a market moving data point. For the record, the manufacturing PMI is forecast to be confirmed at 52.1, its lowest since July 2016.

October’s construction PMI out of the UK is scheduled for release at 0930 GMT. The reading follows yesterday’s disappointing print on manufacturing activity, with the all-important services PMI coming up on Monday.

But all eyes will be on US employment data due at 1230 GMT. The US economy is expected to have added 190k positions in October, above September’s 134k which was the lowest in a year, being impacted by Hurricane Florence. The unemployment rate is projected to remain at the 48-year low of 3.7%. On the wage growth front which is expected to attract most interest, average earnings are predicted to have grown by 3.1% on an annual basis, reaching a fresh cycle peak, specifically their highest since April 2009. Overall, the prints are projected to portray a relatively robust labor market.

Strong data are anticipated to help the greenback. The subtlety at play though is that a beat in wage growth figures that spurs a considerable jump in Treasury yields may end up hurting US stock markets. Hence, the resulting risk aversion from such an outcome will likely end up helping the safe-haven perceived yen, leading to a lower USDJPY.

The reading on September’s US trade balance will be made public at 1230 GMT as well. The relevant deficit is forecast to come in at $53.6 billion, its widest since February. Additional attention will be falling on the politically sensitive trade gap with China that touched an all-time high of $38.6bn in August. Also due out of the US will be factory orders data for September, scheduled to hit the markets at 1400 GMT.

On the Sino-US trade relationship, further evidence that the two sides are edging closer to a deal can be reasonably expected to divert funds into riskier assets, such as equities and risk-on currencies, for example the Aussie. This would come at the expense of haven assets such the yen. Presidents Trump and Xi will be meeting at the G20 summit in Argentina later in the month.

Returning to economic releases, Canada’s respective jobs report for October will be made public at the same time as the one for the US. An addition of 10.0k is predicted by analysts, significantly below September’s 63.3k. The headline number though may be misleading, given that it blends part-time and full-time positions; one has to delve into the actual numbers to draw concrete conclusions. The nation’s unemployment rate is anticipated to remain at the relatively low level of 5.9%. Again similar to the US, Canada will see September trade data as the day unfolds (1330 GMT).

In equities, Exxon Mobil and Chevron will be reporting quarterly results before Friday’s opening bell on Wall Street.

In energy markets, Baker Hughes data on active oil rigs in the US are due at 1700 GMT.

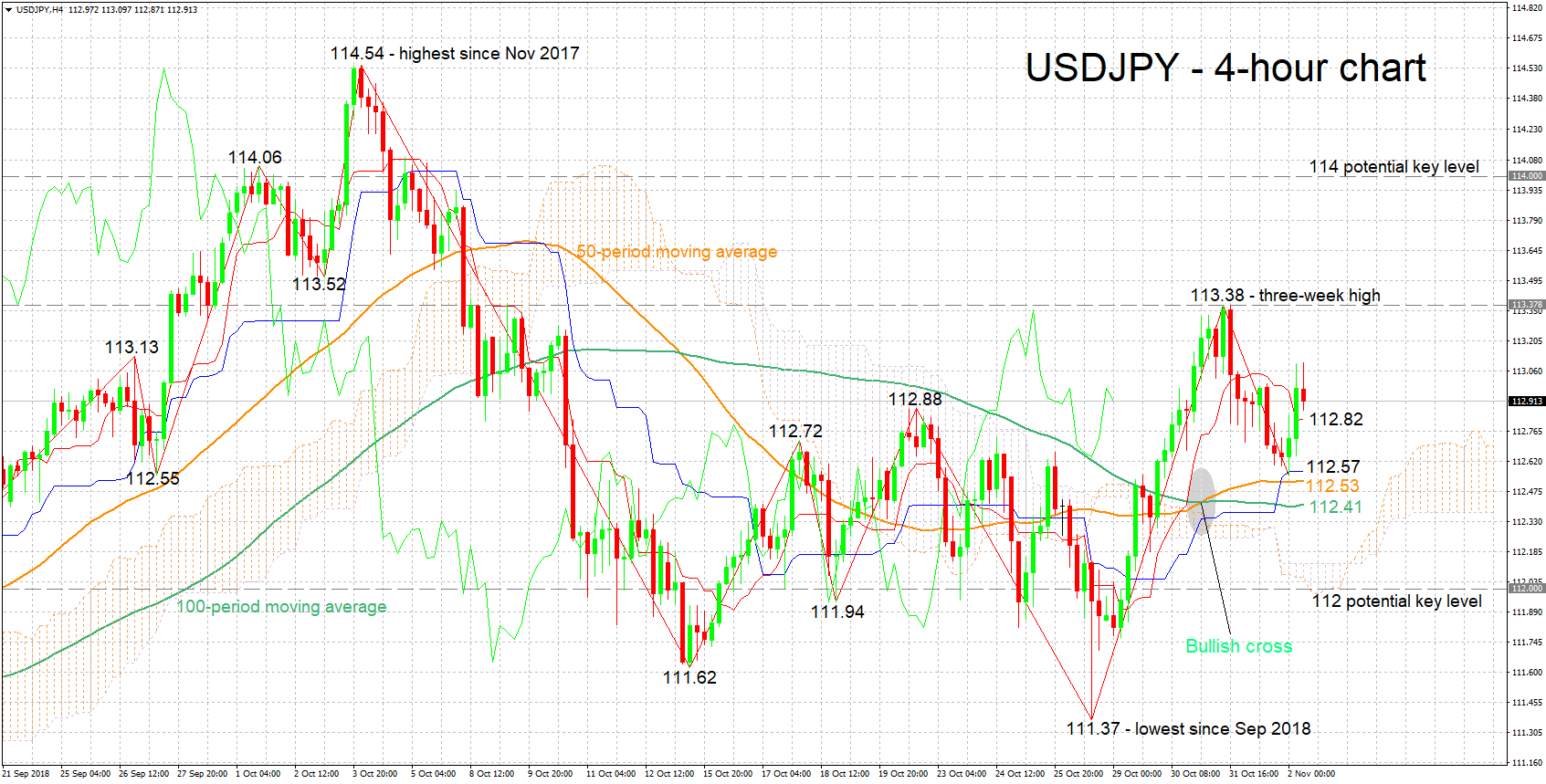

Technical Analysis: USDJPY looking bullish-to-neutral in the short term

USDJPY is trading around 50 pips below Wednesday’s three-week high of 113.38. The Tenkan- and Kijun-sen lines are positively aligned in support of a bullish bias. Notice though that the Kijun-sen has flatlined. On balance, the Ichimoku indicator seems to be projecting a bullish-to-neutral short-term picture.

Upbeat US jobs data that are not associated with a stock market selloff are expected to boost the pair. Resistance to gains may take place around the 113.38 high, with the zone around the 114 handle which captures a top from early October being eyed in case of an upside violation. Further up, the next target will be the 114.54 peak, the pair’s highest since November 2017.

On the downside and in case of disappointing figures or a steep decline in equities, support may occur around 112.53, the current level of the 50-period moving average line; the area around this includes the 100-period MA at 112.41 and the Kijun-sen at 112.57. This, given that the region around the Tenkan-sen at 112.82 is violated first. Further below, the zone around the 112 mark, which also encapsulates the Ichimoku cloud top (112.12) and bottom (11.98), as well as a bottom from the recent past (111.94), would come into scope. Lower still, 111.37, USDJPY’s lowest since September 2018 would increasingly come in focus.

Updates on Sino-US trade relations can also move the pair.