Here are the latest developments in global markets:

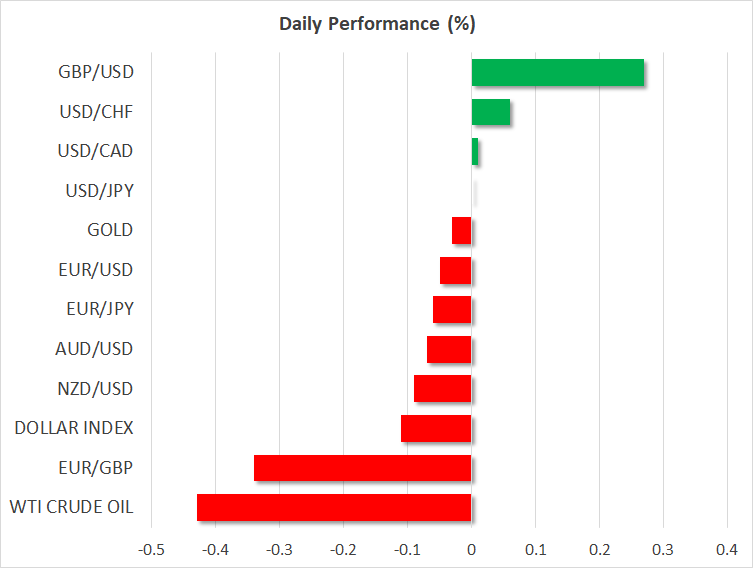

FOREX: The dollar was down by 0.1% versus a basket of currencies on Monday after rising on Friday, when the US saw the release of a robust October jobs report. Sterling outperformed even though it gave up on part of earlier gains, being helped by positive Brexit news.

STOCKS: Wall Street finished lower on Friday, with the Dow Jones (-0.43%), the S&P 500 (-0.63%) and the Nasdaq Composite (-1.04%) all unable to extend Thursday’s gains. Trade uncertainty remains in the background despite recent optimism for a de-escalation in Sino-US tensions, while Treasury yields jumped in the aftermath of the US jobs report that saw annual wage growth rising by the most in nearly ten years. Asian markets took their cue from Friday’s US equity market close, with the Japanese Nikkei 225 and Topix indices losing 1.55% and 1.1% respectively on Monday. Hong Kong’s Hang Seng was down by 2.05%. At 0759 GMT, futures markets were pointing to a mostly lower open for major European benchmarks, though they weren’t projecting steep losses. Contracts on the Dow, S&P and Nasdaq 100 were also in the red; similar to Europe, they weren’t projecting sharp declines.

COMMODITIES: WTI traded lower by 0.4% at $62.86 per barrel. The US proceeded with the re-imposition of sanctions on Iran on Monday – a positive for prices –, though it granted waivers, allowing major buyers to continue purchasing Iranian oil and this has weighed on the precious liquid. Brent crude was down by 0.2%, at $72.67/barrel. In precious metals, gold was roughly flat at around $1,235.50/ounce.

Major movers: Sterling gains on Brexit hopes; dollar modestly down

The dollar’s index against a basket of six major currencies was last down, though by a moderate 0.1%. The greenback gained on Friday as October’s nonfarm payrolls report delivered a notable beat on the number of positions added to the economy, while annual wage growth rose by its fastest since April 2009.

Consequently, markets continue to expect the Fed will remain on track as regards its policy normalization plans. Specifically, Fed funds futures assign an 81% probability for a December 25bps hike, which would constitute the fourth such more during the year. More hints on the US central bank’s thinking are expected during Thursday’s meeting, the penultimate for the year.

Sterling outperformed out of major currencies, with GBPUSD touching a two-week high of 1.3062. News of further progress in Brexit negotiations acted as the catalyst for the move up. In particular, the Times reported PM May has secured concessions from her EU counterparts that will allow all of Britain to remain in a customs union with the EU and avoid a hard border in Northern Ireland.

However, the British currency later reversed part of its gains, as investors appear wary in the absence of anything concrete. PM May will be discussing the latest Brexit proposals with her cabinet on Tuesday. The pound was also up versus the euro, with EURGBP trading lower by 0.35%.

EURUSD was marginally down, not far below the 1.14 handle, while USDJPY was flat at 113.17 even as Bank of Japan Governor Kuroda hinted on Monday that he wants to normalize monetary policy once the central bank edges closer to its inflation target. Perhaps market participants are becoming immune to such comments, waiting for a meaningful pickup in price pressures before taking long positions on the yen.

In emerging markets, the dollar was 0.3% higher against the offshore yuan (USDCNH) after losing ground the previous week, recording its first weekly losses after gaining in the preceding five weeks. Of note, White House economic advisor Larry Kudlow downplayed the chances for a quick trade deal with China, something which also likely aided the move down for Asian stock markets on Monday.

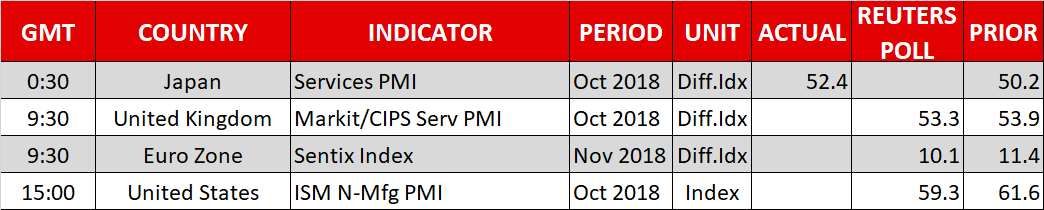

Day ahead: UK services PMI, eurozone Sentix index and US ISM non-manufacturing PMI on the agenda

Monday’s a relatively light data day, with the UK services PMI and the eurozone’s Sentix index, as well as the ISM’s non-manufacturing PMI out of the US being the only notable releases on the agenda.

At 0930 GMT, the UK services PMI for October will be hitting the markets. The index is anticipated to ease to 53.3 from 53.9, which would constitute its lowest since April. Despite the services sector prominence within the UK economy – it accounts for roughly 80% of the economic pie –, sterling is yet again expected to prove most sensitive to Brexit developments rather than on economic releases. Brexit optimism last week and earlier on Monday allowed GBPUSD to touch a two-week high of 1.3062; early last week the pair traded as low as 1.2693. Still, the figures on services PMI may offer some near-term direction to pound pairs.

The eurozone’s Sentix index for November is also slated for release at 0930 GMT. Further weakness is forecast for the gauge of investor morale, which at 10.1 is predicted to touch its lowest since June. Uncertainty around trade and politics – Italian budget angst and a relatively fragile government coalition in Germany – are some of the factors at play that may weigh on sentiment; the automobile industry’s compliance with emissions rules has also been morale-negative recently.

Out of the US, the ISM’s non-manufacturing PMI is due at 1500 GMT. The measure is projected to fall from September’s 61.6, the highest since the index’s creation in 2008, to 59.3, which would also be a robust number. Last week’s manufacturing PMI out of the ISM disappointed, coming in at its weakest since April; still, at 57.7, it remained comfortably in expansion territory. Politics are also taking center stage in the US, with the midterm elections concluding on Tuesday.

Beyond data, trade developments which have boosted sentiment, allowing equity markets and risk-on currencies such as the Aussie to rally towards the latter part of the previous week will be closely watched. Any indication that China and the US are indeed edging closer to a trade deal is likely to be met with a continuation of the rally. Conversely, a correction is likely in store should the confrontational rhetoric make a comeback.

Bank of Canada Governor Poloz will be giving a speech at the Canada-UK Chamber of Commerce at 1210 GMT. ECB Vice President de Guindos and the Bank’s Chief Economist Praet will be speaking in Brussels, where eurozone finance ministers will also be meeting to discuss euro area integration.

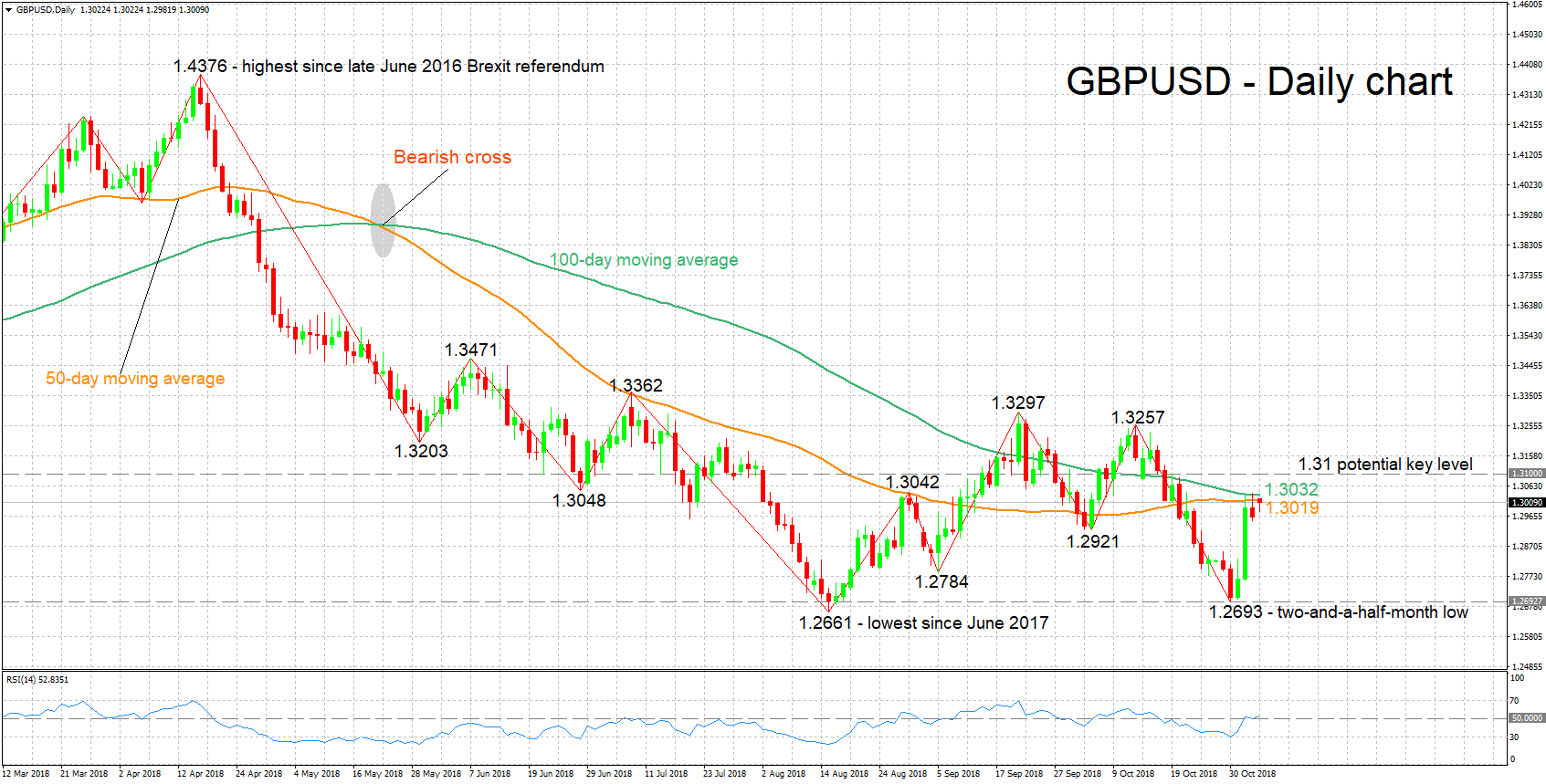

Technical Analysis: GBPUSD looks mostly neutral in the short-term

GBPUSD has eased a bit from an earlier hit two week-high but continues to trade above the 1.30 handle, having staged a recovery after falling to a two-and-a-half-month low of 1.2693 last Tuesday. The RSI has eased after climbing previously. It is currently hovering around the 50 neutral level, mostly pointing to the absence of short-term momentum in either direction, the upside or the downside.

A stronger-than-projected services PMI print out of the UK, or more importantly positive Brexit developments, are expected to boost the pair. Immediate resistance to gains seems to be taking place around the current levels of the 50- and 100-day moving average lines at 1.3019 and 1.3032 respectively. Further above, an additional barrier may occur around the 1.31 handle; the area around this point was relatively congested in the past. Higher still, the October 12 peak of 1.3257 would increasingly come within scope.

On the downside and in the event of weak UK data or a no-deal Brexit again picking up steam, support could come at 1.2921, a previous bottom. Another trough from the past at 1.2784 would come into focus in the event of steeper losses. Even lower, late October’s two-and-a-half-month low of 1.2693 would be eyed; the zone around this also captures the pair’s lowest since June 2017 of 1.2661.