Here are the latest developments in global markets:

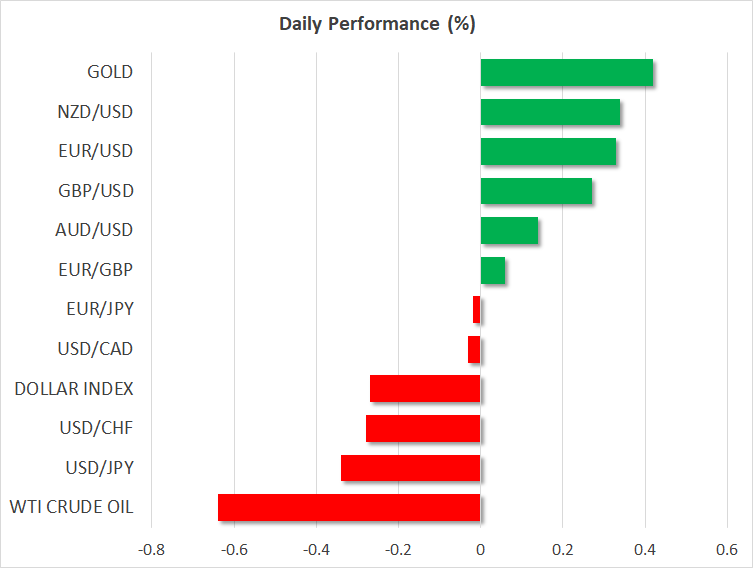

FOREX: The dollar is lower by 0.28% against a basket of six major currencies on Wednesday, weighed down by the results of the US midterm elections, which produced a split Congress – dampening the prospect for any further tax cuts. Meanwhile, the pound continued its Brexit-induced march higher, while the kiwi dollar soared overnight, after a surprisingly strong employment report out of New Zealand.

STOCKS: Wall Street closed in the green on Tuesday as US citizens went to the polls to elect their 116th Congress, with the Dow Jones (+0.68%), S&P 500 (+0.63%), and Nasdaq Composite (+0.64%) all posting decent gains. Even though the outcome was a divided Congress, equity investors seemingly focused more on uncertainty fading rather than the incoming political gridlock, evident by futures tracking the Dow, S&P, and Nasdaq 100 all pointing to a higher open today. Meanwhile, Asia was mostly in the red on Wednesday, with Japan’s Nikkei 225 (-0.28%) and Topix (-0.42%) ticking lower, alongside the Hang Seng in Hong Kong (-0.16%). In Europe, all the major indices were set to open much higher today, according to futures.

COMMODITIES: Oil continued its downtrend, with WTI touching an eight-month low and Brent its own three-month trough, pressured by worrisome signs on the supply front, in light of the US granting sanctions waivers to some of Iran’s biggest clients. Oversupply is slowly returning as a market theme, and it will be crucial to see if the weekly EIA data confirm as much today. In precious metals, gold is up by 0.41% at $1,232 per ounce, hovering near its recent highs. The near-term outlook seems to have shifted back to neutral, with prices now fluctuating between $1,212 and $1,238.

Major movers: Dollar softens on divided Congress; kiwi soars after jobs data

As was widely telegraphed by opinion polls, the US midterm elections produced a split Congress, with the Democratic party taking back control of the House of Representatives, and the Republicans keeping control of the Senate. The result sets the stage for gridlock in Washington DC, rendering President Trump unable to implement most of his domestic agenda – such as tax cuts 2.0 – as the Democrats would likely veto any relevant legislation. Outside of the economic arena, while the Democrats could start an impeachment process, for a US President to actually be impeached it requires a 67/100 supermajority in the Senate, implying Trump is not going anywhere for now.

The market reaction was mostly subdued, possibly due to how widely this outcome was anticipated. The US dollar is modestly lower, as Democrats taking the House likely put to bed any surviving speculation for more deficit-funded tax cuts – evident by a pullback in US Treasury yields. That said, the fact that the Democrats can’t roll back any of Trump’s already-enacted policies probably limited the downside. Meanwhile, stocks appear to have escaped unscathed, as futures tracking the US indices are pointing to a green open today, amplifying the narrative that US equities tend to outperform after the midterms as uncertainty fades, irrespective of which party won.

Elsewhere, the British pound continued its climb higher, touching a five-month high against the euro as optimism surrounding an imminent resolution to the Brexit talks continued to ride high. The latest headlines suggest the UK is drawing up another proposal, which may be presented to Brussels later this month, adding credence to speculation the Brexit “endgame” is gradually drawing closer.

In New Zealand, the local dollar soared after the nation’s employment report for Q3 blew past forecasts, with the unemployment rate unexpectedly slipping to a 10-year low even as the labor force participation rate rose. The strong prints likely enhanced speculation for a more optimistic tone by the RBNZ tonight, which will announce its policy decision at 2000 GMT.

Day ahead: RBNZ rate decision due

On Wednesday, investors will likely assess the economic implications of a split Congress in the US and position themselves accordingly. Beyond that, the Reserve Bank of New Zealand’s (RBNZ) policy decision is an event that has potential to prove market-moving for FX markets, particularly for kiwi pairs.

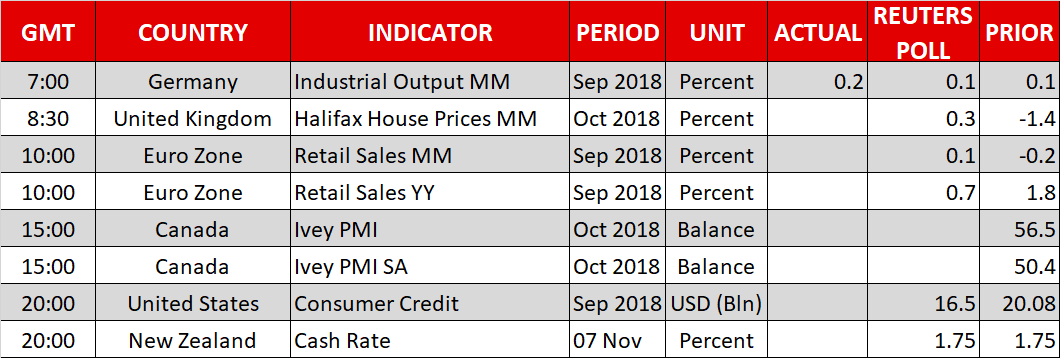

October data on housing prices due out of the UK at 0830 GMT are unlikely to prove market-sensitive, at least not for FX markets where all eyes for positioning on sterling remain on Brexit developments.

Eurozone retail sales for September will be hitting the markets at 1000 GMT. Month-on-month, sales are anticipated to grow by 0.1%, after contracting by 0.2% in August. This would put the annual pace of growth at 0.7% (vs 1.8% previously). Also of interest for euro pairs are any updates having to do with Italy’s budget.

Out of North America, Canada’s Ivey PMI for October will be made public at 1500 GMT, while September consumer credit data out of the US are due at 2000 GMT.

In focus will be the RBNZ’s rate decision at 2000 GMT. The Bank is widely expected to maintain its benchmark rate at the historic low of 1.75%. In light of no change in rates being expected, the RBNZ’s communication – how optimistic it is on the economy’s prospects – will likely act as the driving force for movements in the kiwi.

Earlier in the year, the central bank adopted a dovish stance by not ruling out a rate cut. Jobs data released during today’s Asian session which showed the unemployment rate falling to a decade low, in combination with the recent upside surprise in Q3 GDP growth, may tilt the Bank towards adopting a more upbeat tone, diminishing the chances for a rate cut and thus helping the local dollar. The press conference by the Bank’s Governor at 2100 GMT will also be eyed; his commentary has the capacity to move the kiwi.

In energy markets, EIA numbers on US crude stocks due at 1530 GMT are projected to show an inventory buildup of around 2.4 million barrels during the week ending November 2, following a rise by roughly 3.2m in the previously tracked week.

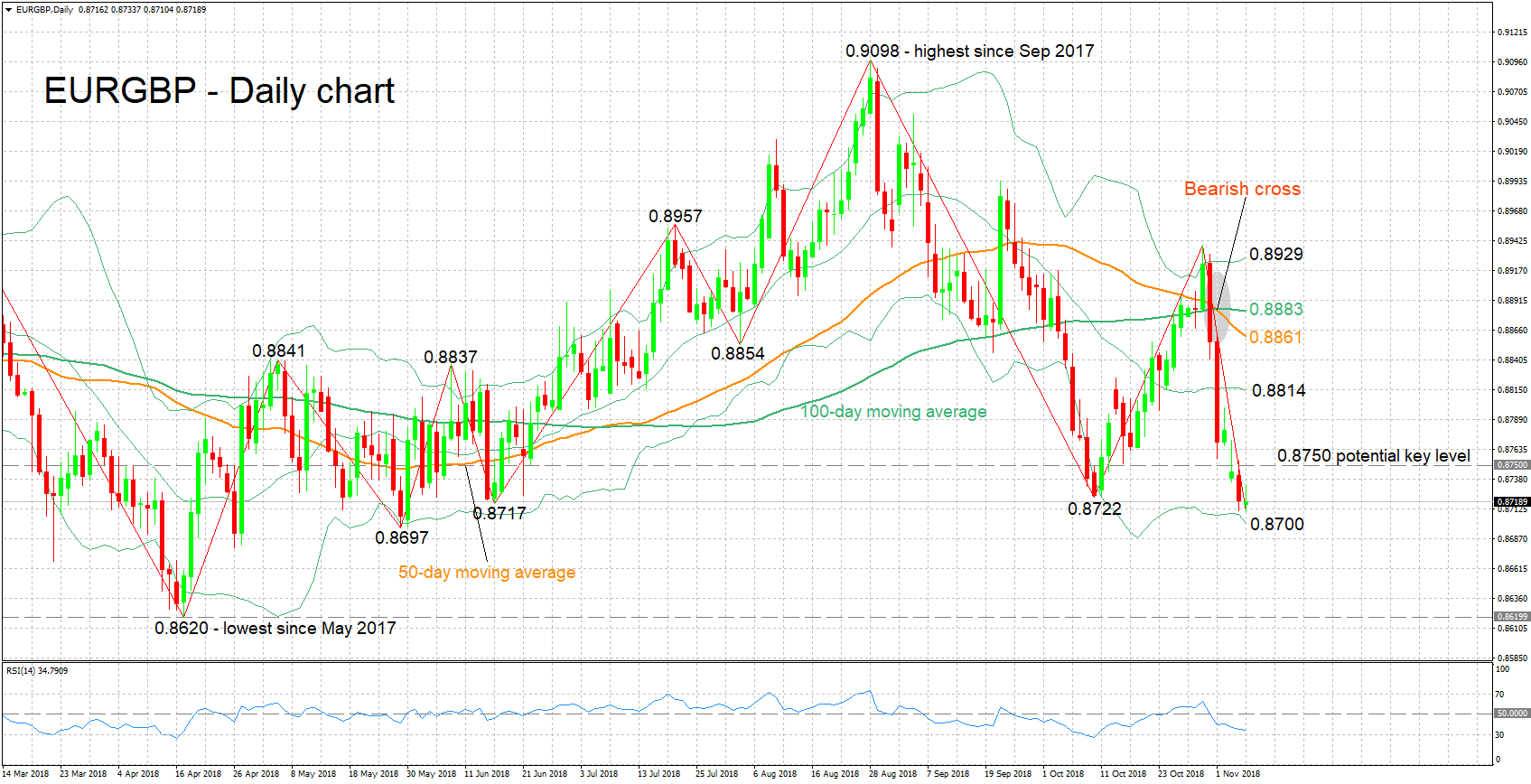

Technical Analysis: EURGBP short-term bearish at 5-month low

EURGBP extended its losses to touch a five-month low of 0.8710 earlier on Wednesday. The RSI is declining in support of a bearish picture in the short-term; notice that at 35, the indicator is relatively close to the 30 oversold level.

Concrete signs that Britain and the EU are edging closer to a Brexit deal are likely to push the pair lower. Immediate support to losses may come around the lower Bollinger band at 0.87; the area around this captures the earlier hit low of 0.8710, as well as numerous other bottoms from previous months. A downside violation would bring 0.8620, the pair’s lowest since May 2017, within scope.

On the upside and in the event of a no-deal Brexit scenario again coming to the fore, support could come around 0.8750; the zone around this was congested between late April to late June. Further above, the region around the middle Bollinger band – a 20-day moving average line – at 0.8814 would be eyed. Higher still, the attention would turn to the current levels of the 50- and 100-day MAs at 0.8861 and 0.8883 respectively.

Italian budget updates can also move the pair.

{kind=link}