The UK will see the release of its latest inflation and retail sales data on Wednesday and Thursday respectively, both at 0930 GMT. While a strong set of prints could support the pound somewhat, the dominant force dictating the currency’s broader movements will likely be the Brexit saga, where both sides are reportedly working round the clock to reach a deal this month. Whether such a deal will pass through the UK Parliament, though, is a different story.

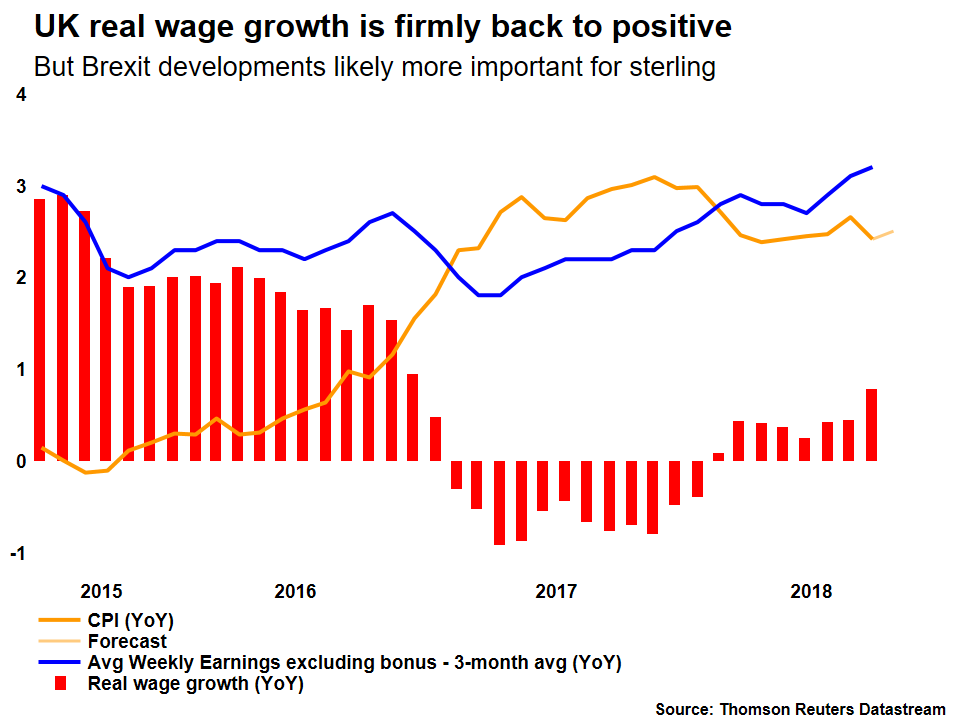

UK inflation is expected to have picked up steam in October, with the headline CPI rate forecast to tick up to 2.5% in yearly terms, from 2.4% previously. The core rate, which excludes the effects of volatile items such as food and energy, is also expected to inch higher to 2.0%, from 1.9% in September. The forecasts are supported by the Markit services PMI for the month, which noted the fastest rise in prices charged by services firms since June. Recall that the services sector accounts for 80% of UK GDP.

Turning to retail sales, both the headline and the core figure – that disregards volatile fuel items – are projected to have risen by 0.2% in monthly terms, a rebound after both fell by 0.8% in September. In yearly terms, the headline rate is expected unchanged at 3.0%, while the core is anticipated to rise marginally to 3.3%, from 3.2% previously.

While a strong set of figures may support the pound on the news, economic data will probably be overshadowed by political developments in driving the currency overall in the coming weeks. To explain – investors currently don’t expect a rate hike by the Bank of England until September 2019, a pricing so gloomy relative to the shape of the UK economy that it probably incorporates worries of a disorderly Brexit. Hence, markets believe policymakers will stay sidelined until there is some political clarity, which implies that economic data could have less of an impact in shaping expectations around future policy changes, for now.

As for the latest Brexit developments, negotiators on both sides are reportedly working round the clock to reach a deal by tomorrow, which would allow time to call a special EU summit by the end of the month to finalize the accord. If that doesn’t work, a deal can still happen, but the focus would shift to the next scheduled EU summit in mid-December. That said, the longer this process drags on, the greater the uncertainty for UK businesses and the less time Parliament would have to debate and ratify any deal, implying that the clock may be working against sterling on this matter.

Even if an accord is reached and approved by the UK Cabinet, pushing it through Parliament may be a herculean task, given how many lawmakers have threatened to vote it down. The opposition Labour party, the DUP, and even several of Theresa May’s own Conservatives – whether Brexiteers or pro-EU moderates – have all indicated as much. Thus, price action in sterling may stay directionless and choppy for a while longer, considering that several twists and turns probably linger before the Brexit fog lifts even partially.

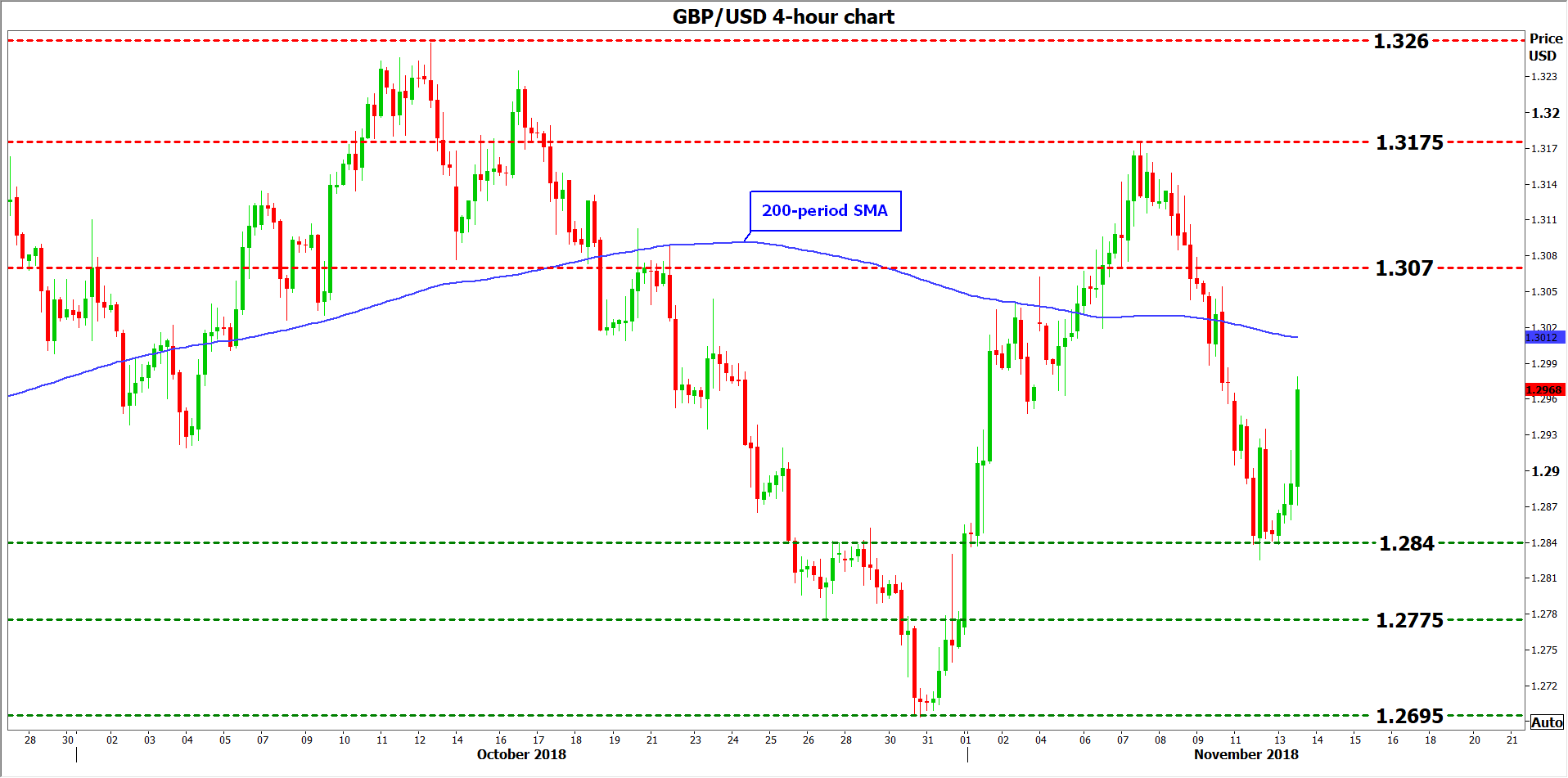

Technically, advances in sterling/dollar could encounter resistance near the 200-period simple moving average (SMA) on the 4-hour chart, at 1.3012. An upside break may open the way for the 1.3070 area, the inside swing of November 7, which also coincides with the 23.6% Fibonacci retracement of the April to August downleg, from 1.4375 to 1.2660. Even higher, the November 7 peak at 1.3175 would attract attention, ahead of the October 12 top at 1.3260.

On the flipside, a pullback in the pair could meet preliminary support around 1.2840, the area that capped the decline on November 12. If the bears pierce below it, the focus would shift to 1.2775, the low of October 26, with even steeper declines setting the stage for a test of 1.2695, the October 30 trough.

{kind=link}