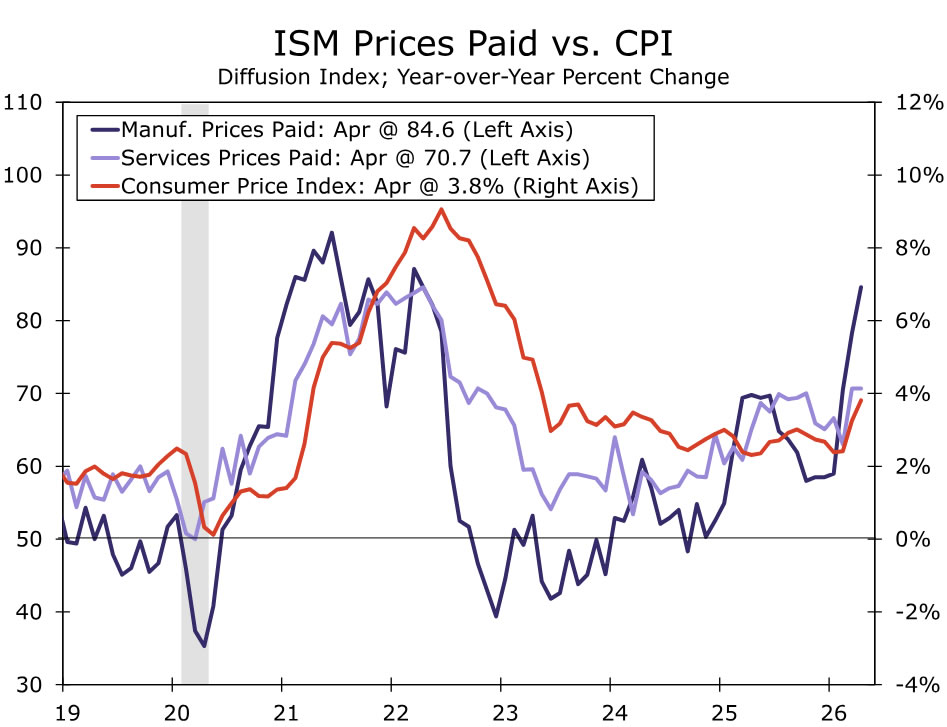

The focus next week is Friday’s U.S. employment report, where we look for May nonfarm payrolls to rise by 105K and the unemployment rate to edge up to 4.4%. Taken together, the report should leave the broader message unchanged: the labor market is no longer deteriorating but still is not meaningfully improving, either. Earlier in the week, the U.S. ISM surveys should point to expansion, with manufacturing holding near April’s level at 52.5 and services easing to 53.4 from 53.6, though the prices paid components will matter most as a signal of broader inflationary pressure.

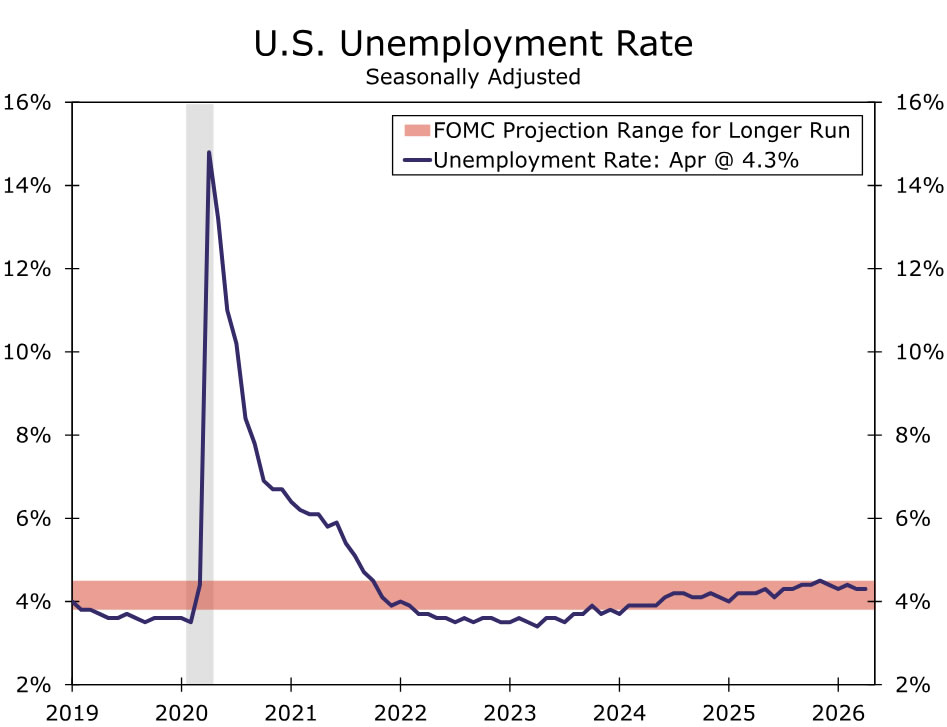

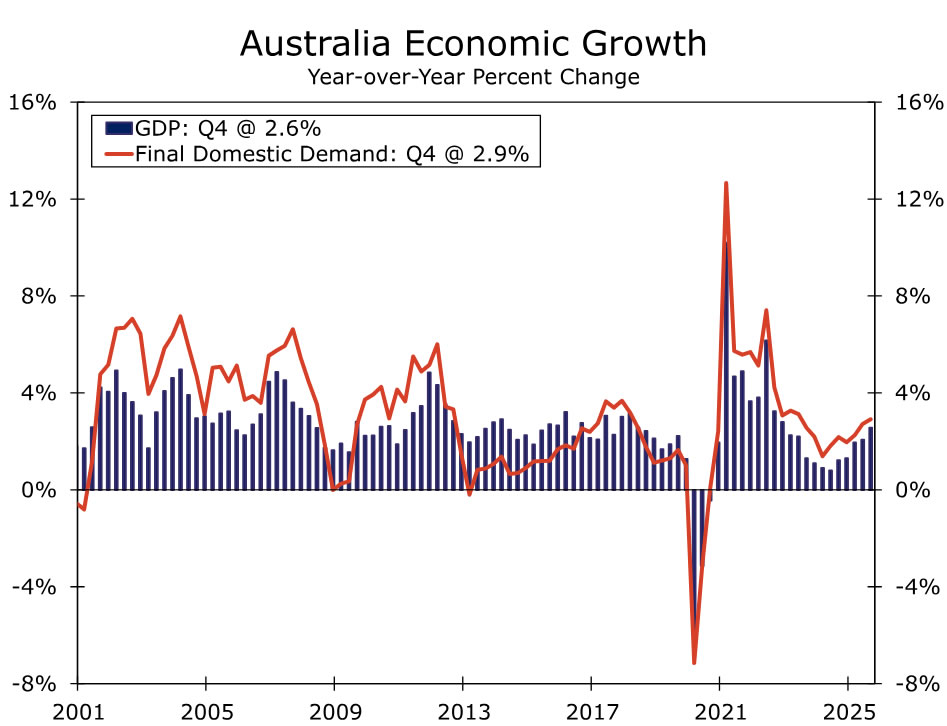

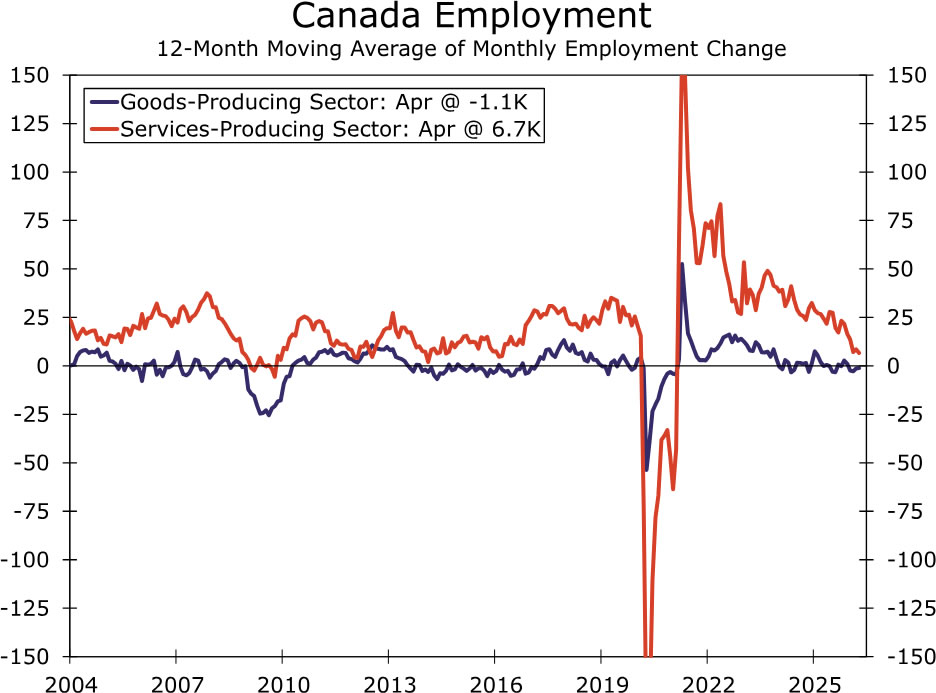

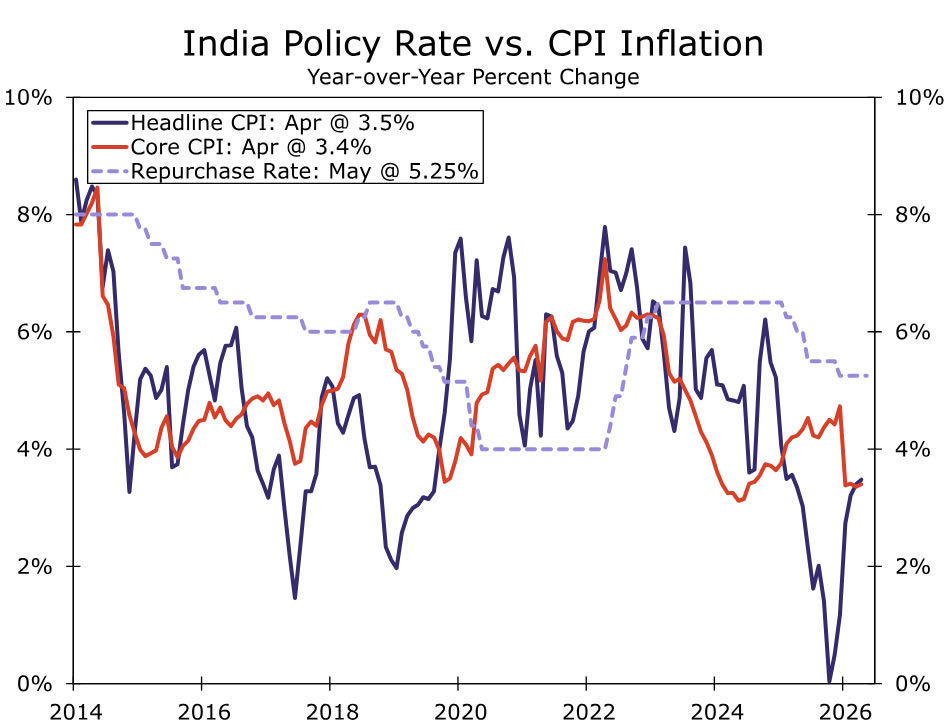

Outside the U.S., we expect Eurozone CPI to rise to 3.3% year-over-year in May from 3.0% last month and core CPI to increase to 2.5% from 2.2%, keeping pressure on the ECB ahead of its June meeting. In Australia, Q1 GDP is likely to remain at a more moderate 2.6% year-over-year rate, and in Canada, we expect employment to rise 15K and the unemployment rate to dip to 6.8%. In emerging markets, the Reserve Bank of India is likely to leave the repurchase rate unchanged at 5.25% next week, though we continue to expect two rate hikes this year.

United States:

- ISM Surveys (Monday & Wednesday), Employment (Friday)

G10 Economies:

- Eurozone CPI (Tuesday), Australia GDP (Wednesday), Canada Labor Force Survey (Friday)

Emerging Markets:

- Reserve Bank of India Policy Rate (Friday)

U.S. Week Ahead

ISM Surveys • Monday & Wednesday

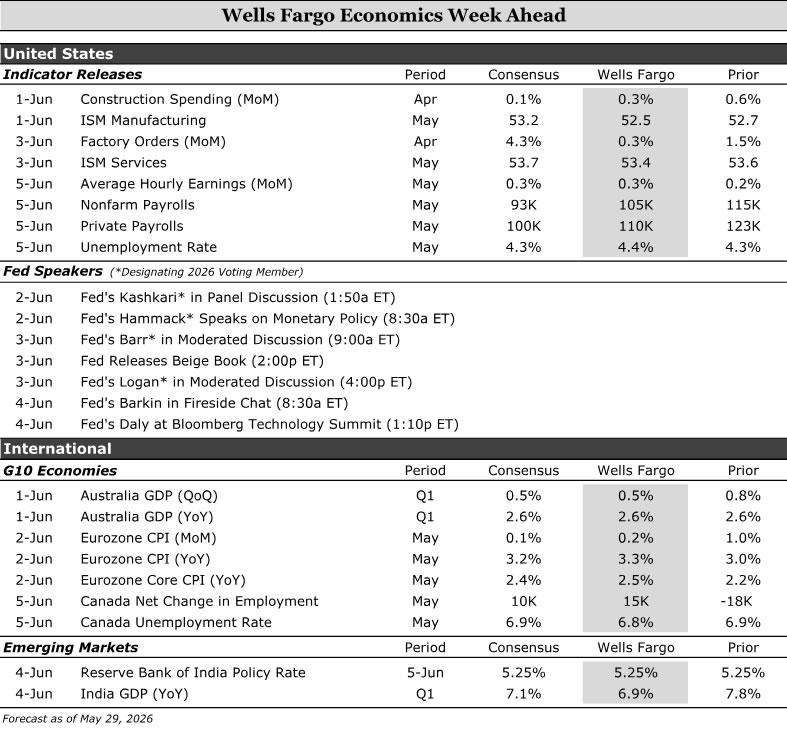

We expect the ISM surveys to indicate continued expansion in May. Regional Fed manufacturing surveys and the Markit PMI both point to little change in underlying conditions, and we look for the ISM manufacturing index to hold near April levels at 52.5.

The prices paid component will get the most attention given the market’s focus on assessing the inflationary spillovers from the ongoing conflict in Iran. Manufacturing input costs have moved sharply higher, but there is little evidence of a comparable pickup in services, where pricing pressures appear more contained.

Service-sector activity also looks resilient. We forecast the ISM services index edging down modestly to 53.4 from 53.6 in April. While uncertainty and cost pressures are building, the data continue to suggest demand is holding up rather than deteriorating materially.

Employment • Friday

The labor market remains stuck in a low fire, low hire equilibrium. Initial jobless claims remain low, and major layoff announcements have been largely limited to tech. Hiring, however, shows few signs of improvement. New job postings on Indeed and regional Fed employment PMIs have been moving sideways, while the Conference Board’s labor differential slipped in May. Together, these indicators suggest there has not been a re-acceleration in labor demand.

With demand little changed, we estimate nonfarm payrolls rose 105K in May. Hiring in cyclically sensitive industries has picked up a bit since late last year, but we expect to see some pockets of weakness following the bankruptcy of Spirit Airlines and additional layoffs hitting the information industry.

Tepid demand for new workers, including recent college grads, is likely to lead to the unemployment rate back up to 4.4%. While most of the drop-off in the participation rate over the past year can be attributed to demographics, the slide also reflects a swath of labor force exits. With the labor force participation rate falling every month this year, we would not be surprised to see a partial rebound in May that pushes the jobless rate higher. Even with an uptick though, the unemployment rate has been largely unchanged over the past year. The stability underscores a labor market that is no longer deteriorating, but also not improving.

G10 Week Ahead

Eurozone CPI • Tuesday

Euro area May CPI is likely to move up to 3.3% year-over-year change from 3.0% in April. On a monthly basis, we expect momentum to ease to 0.2% (from 1.0%) as energy prices stabilize after prior gains. The key question for markets and policymakers is whether price pressures are broadening, as inflation to date has remained concentrated in a narrow set of energy-intensive goods and services. PMI data point to renewed pressure on input costs, although this has yet to feed through to output prices. Focus will remain on services and non-energy industrial goods (NEIG) as indicators of broader pass-through. We look for core CPI to rise to 2.5% year-over-year from 2.2% in April.

Looking ahead to the ECB’s June meeting, the Governing Council will have the May inflation print alongside updated staff forecasts. We continue to see June as the likely starting point for rate hikes, with a follow-up move in Q3, most likely July. That said, a downside surprise in core or continued narrowness in price pressures could tilt the decision toward a hawkish hold in June, with a clear bias to move once broader pass-through becomes evident.

Australia GDP • Wednesday

Australia’s Q1 GDP release next week is likely to show a more moderate pace of growth after the stronger Q4 print. We expect GDP to rise 0.5% quarter-over-quarter and 2.6% year-over-year. While the previous quarter’s headline growth was strong, reaching its fastest annual pace in nearly three years, the underlying details were less convincing. Inventories played an outsized role, while net exports dragged as imports rose sharply.

Q1 indicators have been uneven. PMIs started the year on firmer footing, then softened through the quarter and ended in contraction. Monthly household spending also looked soft in January and February before rebounding sharply in March, though some of that strength may reflect front-loading linked to the Middle East conflict. Investment should provide some support after the stronger Q1 cape print (led by machinery and equipment, driven by a 196% quarter-over-quarter surge in information and telecommunications). However, that is unlikely to fully offset softer consumption and another likely drag from net exports (as shown in the surge of March’s import bill).

In terms of monetary policy implications for the Reserve Bank of Australia, a materially softer GDP print would reinforce the drag from higher rates on household spending and confidence. Still, while April headline inflation cooled, underlying price pressures rose to 3.4% year-over-year and underscored continued pass-through risks. Against this backdrop, we continue to see room for one more 25 bps hike in August, taking the Cash Rate to 4.60%.

Canada Labor Force Survey • Friday

We expect the stabilization narrative in the labor market to persist despite April’s unexpected softening. Employment growth is projected to rise by 15k in May, with the unemployment rate declining to 6.8%. The April increase in unemployment was driven by a surge in participation alongside weak hiring rather than layoffs.

Looking ahead, labor demand should be supported by firmer consumer spending, improved business sentiment, and ongoing fiscal support. Elevated energy and commodity prices represent an inflationary tailwind for Canada, likely skewing job gains toward resource-linked sectors. Structurally, labor supply constraints remain intact, with an aging workforce and weaker immigration flows continuing to weigh on participation and push the unemployment rate lower over time.

A weak May print would challenge the stabilization narrative and, coupled with soft Q1 GDP, could push back expectations for a BoC rate hike beyond July, which remains our baseline.

EM Week Ahead

Reserve Bank of India Policy Rate • Friday

Reserve Bank of India (RBI) policymakers will meet next week, and we expect them to leave the Repurchase Rate on hold at 5.25%. We see a hold as likely because inflation is still within the RBI’s 2%-6% target range, helped in part by government subsidies, which gives policymakers some room to assess pass-through before tightening policy. That said, the inflation outlook has become more challenging. Higher energy and food prices are likely to push headline inflation higher in the coming months, especially if the Middle East conflict keeps energy prices elevated or El Niño conditions weigh on the southwest monsoon.

Recent high-frequency indicators suggest that strong momentum in economic activity has continued, and next week’s Q1 GDP print should provide a clearer read on the economy’s underlying strength. Still, the growth outlook has become more vulnerable as higher energy prices, rising shipping and insurance costs, and supply disruptions risk pressuring margins and weighing on downstream production. The rupee has also come under pressure from higher oil prices, short-term capital outflows, and a stronger dollar.

At its April meeting, the MPC maintained a neutral stance, which preserved flexibility to respond to incoming data. With inflation risks moving higher, growth risks shifting to the downside, and currency pressures building, we continue to see policy risks skewed toward tightening. We maintain our view for two rate hikes this year, one in Q3 and one in Q4, which would bring the Repurchase Rate to 5.75%.

{kind=link}