Here are the latest developments in global markets:

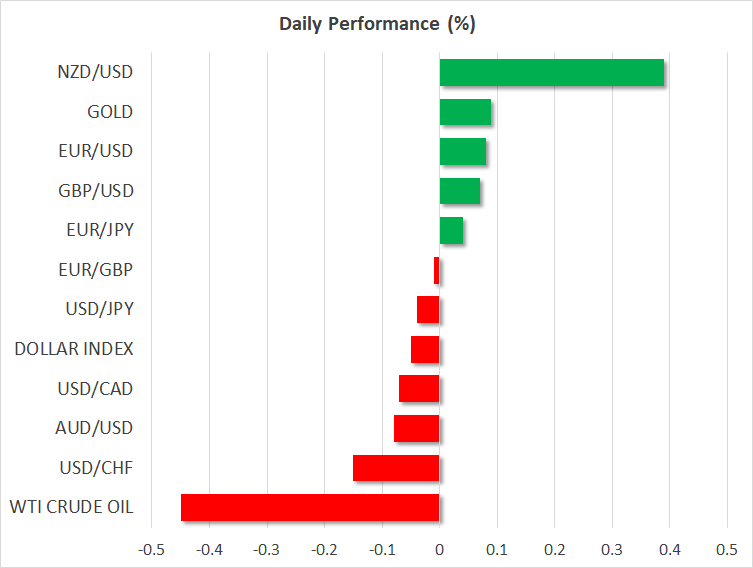

FOREX:The dollar index is marginally lower on Tuesday (-0.08%), extending the losses it posted in the previous session as US bond yields declined and a disappointing NAHB index fueled speculation the US economy may have peaked. The Swiss franc was the best performer, attracting inflows amid risk aversion in markets, while the euro followed closely in its tracks. The pound was little changed amid no fresh Brexit news, though investors may turn their attention to a testimony by BoE policymakers today.

STOCKS: Wall Street closed firmly in the red, with the weakness being led by the technology sector and specifically by FAANG stocks (see below). Accordingly, the tech-heavy Nasdaq Composite (-3.03%) was the worst performer, while the S&P 500 (-1.66%) and Dow Jones (-1.56%) also felt the heat of the tech rout, given the heavy weighting firms like Apple (-3.96%) have in these indices. Asian markets were also a sea of red on Tuesday, with indices in Hong Kong and China leading the drop. Europe didn’t escape unscathed either, with futures tracking all the major benchmarks pointing to a lower open today.

COMMODITIES: Oil ticked higher on Monday on the back of speculation for OPEC supply cuts, and amid news the EU is set to sanction some Iranian nationals. However, the recovery proved short-lived and crude retreated again, weighed by the risk averse market environment. WTI is currently trading at $56.90 a barrel, and Brent at $66.31 per barrel. In precious metals, gold continues to take advantage of the pullback in the dollar, moving further above its 100-day moving average to currently trade at $1,225 per ounce – looking set to challenge the downtrend line drawn from the peaks of May soon.

Major movers: Dollar drops alongside Treasury yields as risk appetite sours

The dollar underperformed most of its peers on Monday, falling in tandem with US bond yields, which were hammered somewhat lower as investors increased their exposure to defensive assets amid a sharp selloff in US equity markets. A disappointing National Association of Home Builders (NAHB) index likely exacerbated the greenback’s troubles, via amplifying the latest narrative that the Fed is set to pause its hiking cycle next year. Recall that housing data are considered a forward-looking gauge of broader economic activity and hence, the loss of momentum recently is an ominous sign for future growth prospects. Against this backdrop, figures on building permits and housing starts today may attract special attention.

The Swiss franc and the euro were the main beneficiaries of the pullback in the dollar, outshining even the defensive Japanese yen despite the broader weakness in risk sentiment. In the UK, the pound continued to trade in a choppy manner, gaining against the dollar but losing versus the euro, in the absence of any major Brexit updates. Attention may (briefly) turn away from UK politics today, as several BoE policymakers including Governor Carney and Chief Economist Haldane will testify before Parliament. Market pricing derived from the UK overnight index swaps suggests investors no longer expect a rate hike by the BoE in 2019 amid heightened Brexit uncertainties, and if Carney & Co. appear comfortable with that, the pound could come under renewed selling interest.

In equity markets, reports Apple is cutting its orders for iPhone components re-awakened the tech bears, with FAANG stocks (Facebook, Amazon, Apple, Netflix, and Alphabet’s Google) posting severe losses. While the trigger may have been hints of weaker demand for Apple products, the rout was likely aggravated by money managers liquidating prior long-equity positions to protect their year-to-date profitability, as the end of the year is now in sight. The implication is that equity investors should be especially careful heading into year-end; any further weakness could “feed on itself” much easier than usual, as several funds attempt to protect their profitability by locking in profits in the face of a declining market, thereby exacerbating the sell-off.

Day ahead: US housing starts due; Carney appears before Parliament; Brexit, EU-Italy budget standoff, Sino-US trade dispute at play

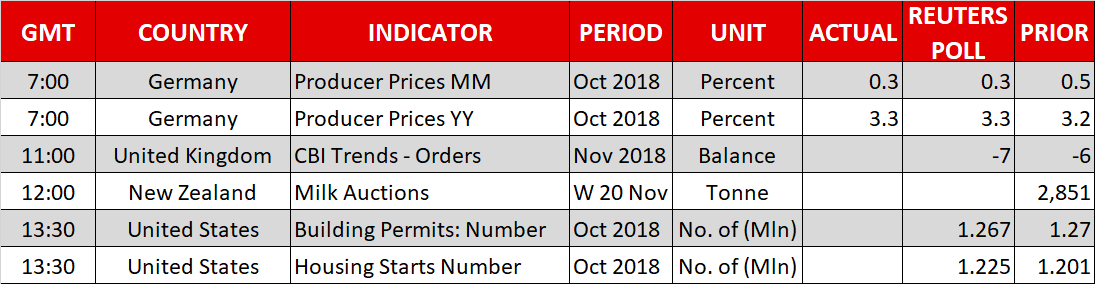

Bank of England Governor Carney’s parliamentary appearance will be attracting interest on Tuesday. Elsewhere, some housing data out of the US are on the agenda, while beyond releases, the themes of Brexit, the EU-Italy budget standoff and the Sino-US trade dispute remain at play, with any headlines having the potential to drive positioning in the markets.

Numbers on factory orders are due out of the Confederation of British Industry (CBI) at 1100 GMT, though these look secondary compared to any news on Brexit which have the capacity to lead to wild swings in sterling pairs.

Also pound-related and before the CBI figures, BoE Governor Carney, Deputy Governor Cunliffe, Chief Economist Haldane and external MPC member Saunders will be appearing before parliament to answer questions about the Bank’s November Inflation Report at 1000 GMT. They’re also likely to be on the receiving end of questions as regards the Bank’s plans in the event of a no-deal Brexit, with any comments on this front probably proving sterling-sensitive.

At 1330 GMT, October data on US housing starts and building permits will be made public. These don’t tend to be market-moving for FX markets though they’re attracting more interest as of late given that the rising rate environment is acting as a drag on the real estate market. Moreover, Monday’s figures that showed US homebuilders’ sentiment posting its sharpest monthly decline in more than four-and-a-half years, is giving an additional element of importance to the numbers.

Also at 1330 GMT, the Philly Fed will be issuing its November non-manufacturing business outlook survey.

In relation to the EU-Italy disagreement over the latter’s spending plans, the European Commission will release its report on all eurozone draft budgets tomorrow; Italy will likely be identified as violating the relevant rules.

The kiwi dollar may get some short-term direction from today’s bi-weekly milk auction, given that dairy products are New Zealand’s largest goods export earner. Thus, higher prices are seen as positive for the local dollar. Some calendars mark the release at 1200 GMT, though it is tentative in nature, hence the relevant numbers may well be made public at some other point in time.

The Bank of Canada’s Wilkins will be giving a speech at 1800 GMT.

In energy markets, weekly API data on US crude stocks are due at 2130 GMT.

In equity markets, it will be interesting to see whether the tech selloff, which according to some is coming on the back of worries over the Sino-US trade spat, has more room to run.

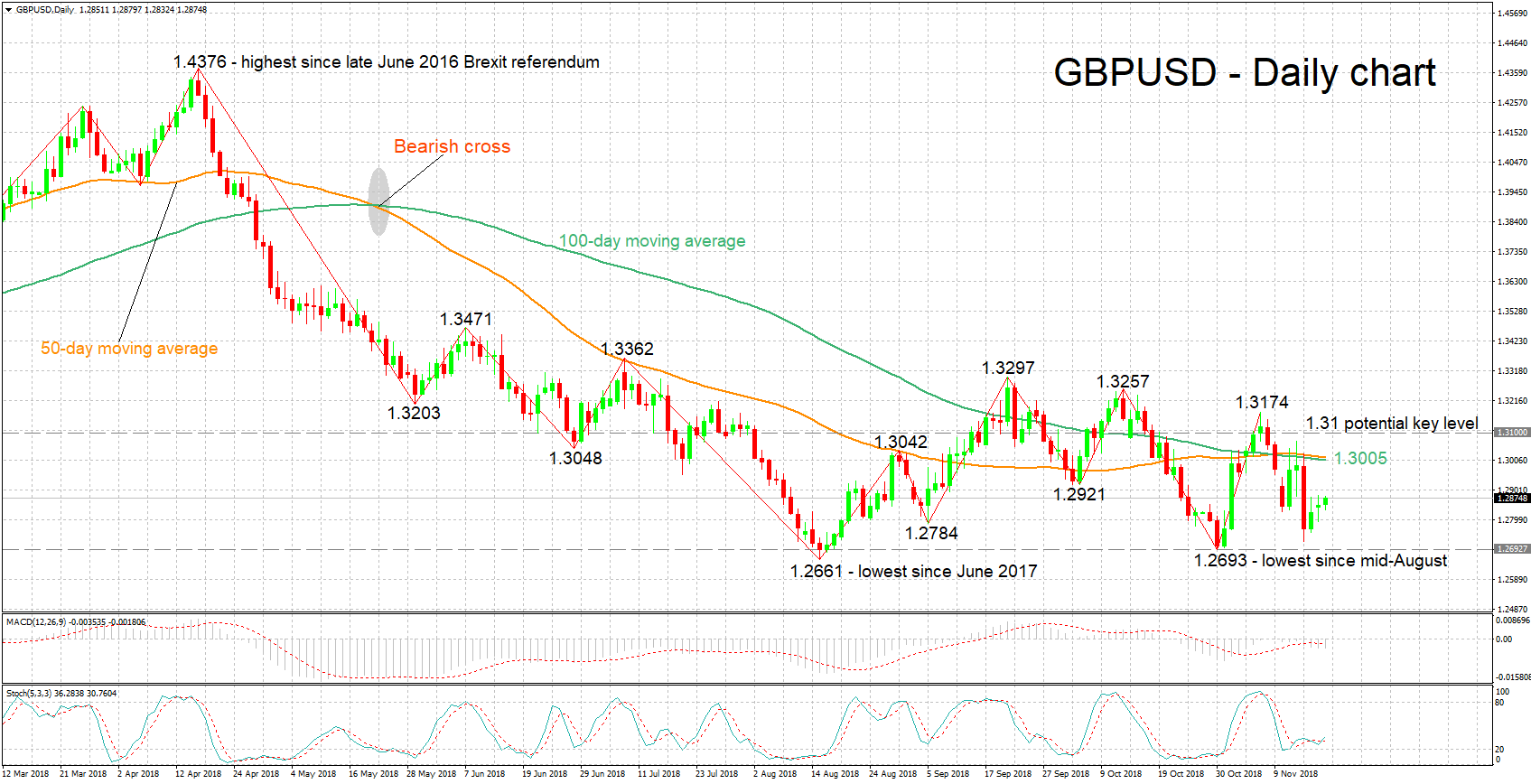

Technical Analysis: GBPUSD negative short-term bias still at play

GBPUSD has recovered somewhat after coming close to its lowest since mid-August of 1.2693 last week. The MACD being below its trigger line suggests that the short-term bias is still negative. However, the stochastics may be giving an early sign for gains in the very short term, as the %K line has just moved above the slow %D one.

Upbeat remarks by Carney or positive Brexit news are likely to boost the pair. Resistance to gains may take place around a previous low at 1.2921. Further above, the area around the current level of the 100-day moving average line at 1.3005 would be eyed; the 50-day MA has roughly converged with the 100-day one, while not far above lie a top (1.3042) and a bottom (1.3048) from previous months. Steeper gains would eye the region around the 1.31 handle which was relatively congested in the past.

Losses on the back of a dovish Carney or additional Brexit complications could meet support around 1.2784, this being a previous bottom. Further below, the zone around 1.2693, the pair’s lowest since mid-August, would come within scope; notice that 1.2661, a more than one-year nadir lies not far below.