Political risk in the euro area is not dead and is currently weighing on the EUR along with Draghi’s ‘dovish’ message yesterday that emphasised that the eurozone still requires substantial stimulus – if so, its suggests that there is little likelihood of an imminent QE tapering announcement at next weeks ECB meeting.

The probability of Italian snap elections has risen substantially, despite the baseline scenario is still for general elections to be held next-year. The momentum for early elections has grown in recent sessions and if they were to be held under the new voting system that has been reportedly agreed across parties, the odds are rising that the anti-establishment parties could win the government.

Under the above scenario, investors should expect volatility in Italian and periphery assets to increase in the coming weeks.

Euro zone finance ministers failed to agree with the IMF on Greek debt relief or to release new loans to Athens last week, but did come close enough to aim to do both at their June meeting. What’s Greece to do?

Markets focus will be on today’s PCE release (08:30 am EST), the Fed’s preferred measure of inflation.

1. Global stocks finding little or no traction

With China, Hong Kong and Taiwan markets again closed for holiday’s overnight led to thin trading conditions.

In Japan, the Nikkei share average inched down -0.02% overnight as the market felt the weight of a stronger yen (¥110.89) on risk aversion, while the broader Topix rallied +0.2% after erasing an earlier decline of -0.5%.

In South Korea, the Kospi dropped -0.4%, falling for a second day from record highs as investors booked profits.

In Singapore, the Straits Times Index slid -0.4%.

In Europe, indices trade lower across the board with notable under performance from the French CAC, and German DAX with dovish Draghi comments on the Eurozone economy weighing on sentiment. On the FTSE 100 airline stocks trade lower.

In the U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.5% at 3563, FTSE -0.3% at 7524, DAX flat at 12624, CAC-40 -0.7% at 5298, IBEX-35 -0.2% at 10858, FTSE MIB -0.3% at 20731, SMI -0.4% at 8993, S&P 500 Futures -0.1%.

2. Oil slips on oversupply worries despite OPEC deal, gold shines

Oil prices remain on the back foot, pressured by market concerns that production cuts by OPEC and some non-OPEC members may not be enough to drain a global glut that has depressed the market for the past three-years.

Ahead of the U.S open, benchmark Brent crude is down -40c a barrel at +$51.89 after having gained +14c yesterday. U.S light crude has fallen -20c to +$49.60

OPEC and other oil producers, including Russia, agreed last week to keep a tight rein on supply until the end of Q1, nine-months longer than originally planned back in November 2016.

The collective output by OPEC and other producers will be held around -1.8m bpd below its level at the end of 2016.

Technically, the market is still trying to decide if OPEC has done enough to balance supply and demand. Nevertheless, the problem for OPEC is oil supply in the U.S, where shale production continues to boom.

Market price action since the May 25 decision would suggest that the market was expecting much deeper cuts and a longer deal. Despite the ongoing cuts, oil prices have not been able to rally much beyond +$50 per barrel.

Data last week showed that U.S. drillers have added rigs for 19-consecutive weeks to reach 722, the highest in two years.

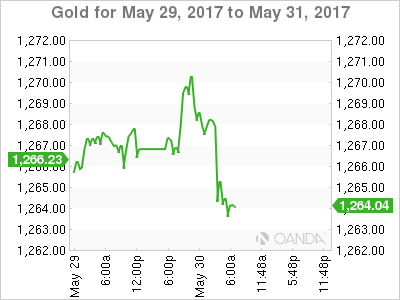

Gold has edged up to touch a one-month high overnight, with investors turning to the safe-haven asset as geopolitical tensions sap their appetite for risk. Spot gold has rallied +0.1% to +$1,267.30 per.

3. Euro periphery yields rally

Geopolitical risks in Europe have periphery yields backing up. Italian 10-year government yields have backed up +13 bps to + 2.20% on reports that Italy’s main parties are close to an agreement on a new voting law and that former PM Renzi said he favored an election in autumn. The threat of an anti-Euro party governing Italy is expected to have Italian assets underperforming in the short to medium term.

In the U.S, the Fed has strongly signalled that it will raise interest rates next month, but officials have promised to keep a close watch on inflation, and their preferred gauge – personal-consumption expenditures price index or PCE – will be in the spotlight this morning at 08:30 am EST. The yield on 10-year Treasuries declined less than one basis point to +2.24%.

Down-under, Aussie 10-year yields fell -2bps to +2.39%.

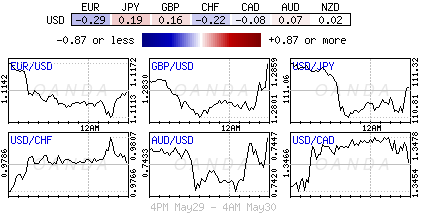

4. Dollar steady

Modest risk-off is playing out in FX space going into today’s key PCE inflation data and China manufacturing PMI’s this week.

Note: Both reports have shown underwhelming prints over the past two-months.

A new round of political worries over Greece, Italy and Britain has the respected regional currencies under pressure.

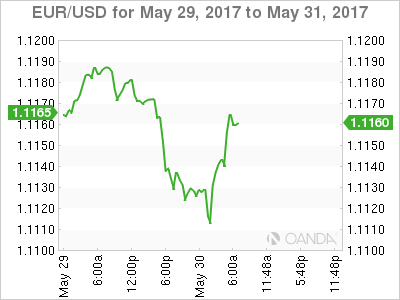

The EUR/USD (€1.1162) has drifted from its recent seven-month highs made last week as a plethora of May inflation data backs the ECB’s view that extraordinary monetary accommodation will remain in place for the foreseeable future.

Sterling (£1.2854) is beginning to find resistance to the topside as more polls show the gap between PM May’s Conservatives and Labour narrowing. The pound is currently trading in ‘no-man’s land’ after probing above £1.3000 last week.

Note: Conservative Party’s lead continues to erode (Opinium Poll: Con: +45% (-1); Labour +35% (+2); ComRes Poll: Con: +46% (-2); Labour +34% (+4); ORB/Telegraph Poll: Con: +44% (-2); Labour +38% (+4).

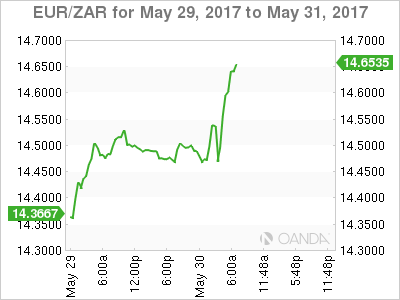

The ZAR ($13.0700) continues to exhibit volatility. The rand weakened yesterday after South Africa President Zuma survived another confidence motion from within his ruling party. However, the currency recovered after reports circulated that the DA office would file charges against the President.

5. Japan near full employment, but no inflation, German inflation falls

Japan has a labor shortage, but the labor structure is not allowing wage inflation.

Data overnight shows that Japan’s jobless rate remains at its 23-year low of +2.8%, while household spending again remains relatively soft.

Japan’s April overall household spending y/y is -1.4% vs. -0.9%e – a 14th consecutive month of declines.

Data released by six German states this morning suggest that German consumer price inflation fell a little more than expected in May, to about +1.5% from +2.0% in April. The market consensus was looking for a +1.6% reading.

Regional releases hint at a pick-up of food inflation this month, but energy inflation dipped, in line with expectations, given the fall in oil prices.