- Fed – Markets are still processing Fed decision

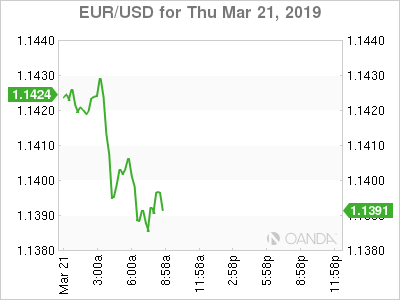

- EUR – Euro falls as German bunds target zero

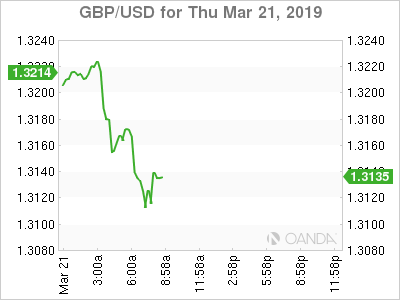

- BOE – Unchanged on Interest Rate (vote 9-0)

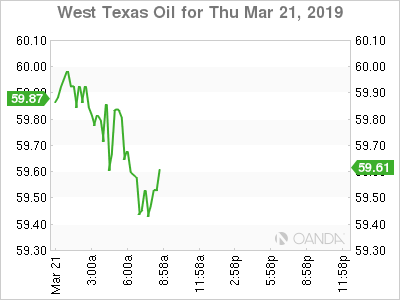

- Oil – Softer on profit-taking

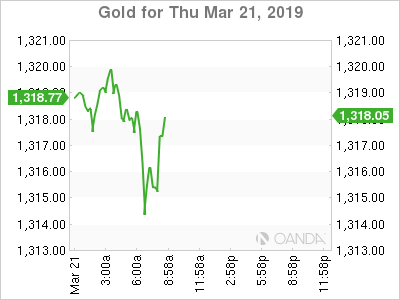

- Gold – Support from dovish Fed, Brexit and Trade risks

Fed

Financial markets are still processing the Fed’s decision to remove all rate hike expectations for 2019. Government yields across the board are all sharply lower, while the dollar traded mixed and stocks retraced some of yesterday’s gains.

Economists will now debate over the coming months whether this dovish commitment is a policy mistake. The Fed’s concern for the economy likely suggests they will be overly cautious reversing course back to a tightening bias even if we see a strong second quarter of data.

US data this morning was strong and will like fuel the fire that is questioning the Fed’s dovish commitment. Jobless claims came in better than expected and the Philadelphia Fed business outlook rebounded sharply

EUR

The euro is softer as the dollar mustered up a rebound following yesterday’s FOMC dovish commitment that sent the dollar flailing. The low interest rate environment that was supported by yesterday’s Fed decision will also drive Bund yields down and possibly back to zero. The 10-year Bund yields fell 4.5 basis points to 0.035%, the lowest level since Autumn of 2016.

Key manufacturing data will be released tomorrow, and expectations are for both Germany and the euro zone to rebound. Improving economic data is what will be needed to help take the euro out of its stubborn 1.12 to 1.16 range.

BOE

The Bank of England rate decision went as planned with a unanimous vote on maintaining the Bank Rate at 0.75%, Corporate Bond Target at £10 billion and the Asset Purchase Target at £435 billion. The BOE is pretty much on hold until we get Brexit clarity. They signaled that monetary policy is dependant on whatever form Brexit takes. The British pound slightly came off the session lows following the decision.

Financial markets are no longer as optimistic as they were that the next move will be a rate rise from the BOE. Dwindling expectations on a BOE rate rise are stemming from a global low interest rate environment.

Oil

Yesterday’s rise with crude prices was supported by the falling dollar and the biggest plunge in weekly crude inventory data since July. Today’s pullback with oil prices is more of a profit-taking move than anything else. The tentative rise above $60 a barrel signals that we many longer be in an oversupplied market. Oil may have room for one last major push higher, but with US production poised to keep taking production to fresh record levels, we could see prices play ping-pong over the coming months.

Gold

The precious metal is rising for a fifth consecutive day and is benefiting from the very dovish Fed statement delivered yesterday. Gold may continue to have a positive backdrop as two major headwinds to the global economy appear to have substantial updates next week. The Brexit date is just over a week away and it is expected next week will be pivotal and that could be uncertainty should persist to the very end. Trade talks between China and the US enter a high gear next week when Mnuchin and Lighthizer go to Beijing, so it would be unexpected to see a breakthrough before then.