Following the unexpectedly strong Q1 GDP data out of Japan this week, the focus now turns to April trade numbers on Wednesday (Tuesday, 23:50 GMT) and inflation figures on Friday (Thursday, 23:30 GMT). Despite the impressive growth figures, worries remain about the outlook for Japan’s economy as the October sales tax hike nears and trade tensions escalate. Investors will therefore be watching carefully how the economy evolves over the next few months for signs the Bank of Japan would need to step in again to kick start growth.

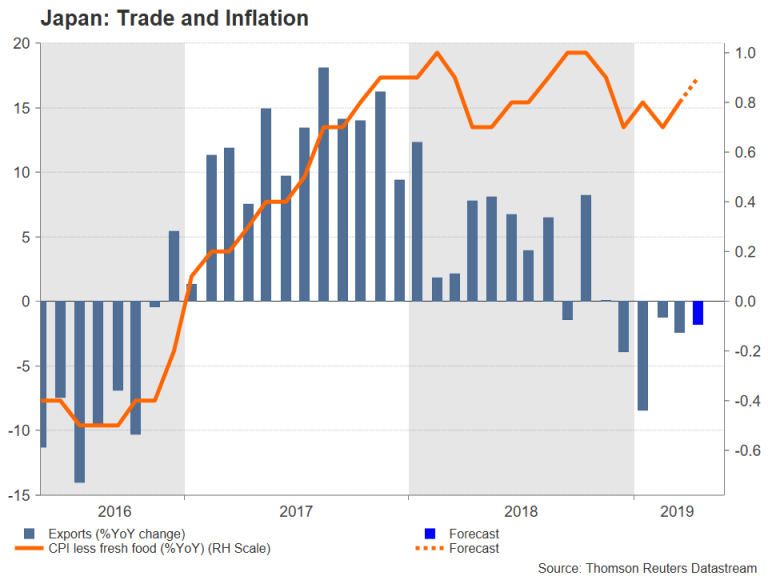

Japan’s first quarter GDP growth may have beaten even the top estimates, coming in at 0.5% quarter-on-quarter, but under the surface, there was less to cheer about. Both private and business spending fell over the quarter, while exports tumbled by 2.4%. The only ‘bright spot’ was that imports plunged by even more than exports to produce a positive contribution from net trade of 0.4% to GDP growth. This puts the focus on Wednesday’s trade data to see whether the exports picture improved at all in April.

Slide in exports probably continued in April

But that’s unlikely to have been the case as exports are forecast to have declined by 1.8% year-on-year in April, easing only marginally from the prior 2.4% drop. There could be some good news from imports, however, as they are expected to have increased by 4.8% over the year versus 1.2% in the previous month, possibly signalling strengthening domestic demand.

Turning to Friday’s inflation release, core CPI is forecast to rise from 0.8% to 0.9% y/y in April, which would make it the highest since November 2018. The core CPI rate excludes fresh food prices and is what the Bank of Japan targets for its 2% inflation goal. But the measure has been moving sideways after peaking at 1.0% in February 2018. The BoJ has repeatedly said it would consider additional easing if inflation lost momentum in rising towards the target. Should core CPI continue to edge higher in the coming months, the BoJ is more than likely to stay on the sidelines.

Intensifying trade war poses a major risk

However, with the growth outlook becoming gloomy again as US-China trade tensions intensify, the risks to the Japanese economy are tilted to the downside. China is Japan’s largest export destination, followed by the United States, so weakening demand in either of those economies, as well as a disruption to the global supply chain from the trade war could have a significant negative impact on Japan.

Another risk for growth is the planned sales tax hike in October. If the darkening clouds from trade tensions haven’t cleared by then and the government presses ahead with its tax increase, the BoJ may be forced to ramp up its stimulus.

Data not anticipated to move the yen

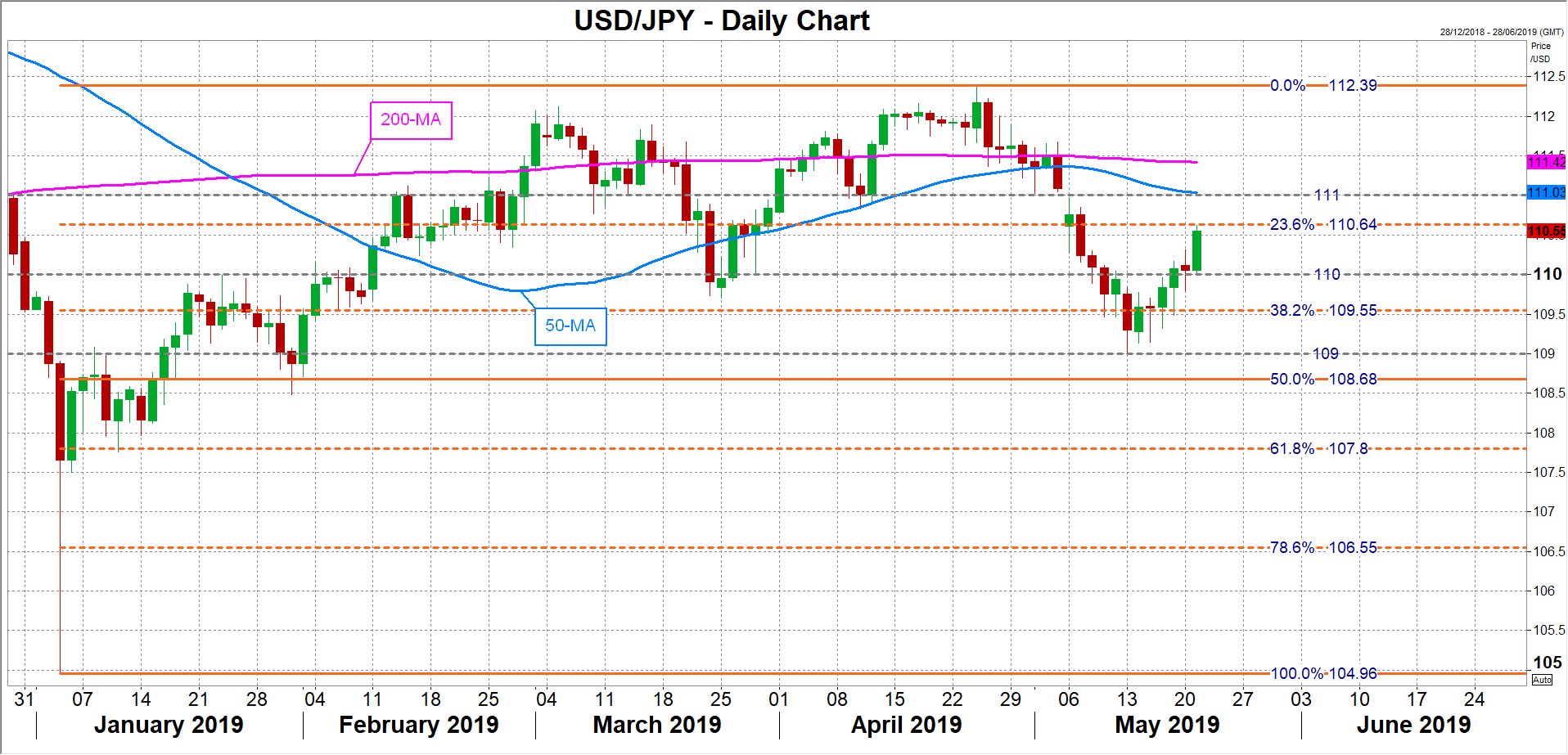

Until such a scenario starts to develop, however, the yen is unlikely to move much to domestic economic indicators, with any reaction to this week’s releases expected to be limited. Potential resistance for the yen to stronger-than-expected numbers could arrive initially at the 38.2% Fibonacci retracement of the upleg from 104.96 to 112.39 at 109.55 per dollar, followed by the 109 level. But weak figures could see the yen breaking below immediate support at the 23.6% Fibonacci at 110.64 per dollar and head towards the 50-day moving average near the key 111 level.

{kind=link}