Financial markets are still clinging to belief central banks will come to rescue as President Trump tries to prevent his multi-front trade war from crushing the American economy. With the ECB joining the likes of the RBNZ, RBA, and Fed in signaling dovishness, it appears the punch bowl is back, and global equities could resume the longer-term bullish trend if we start seeing some progress with some trade wars. The dollar remains on soft footing as the 10-year Treasury yield continues to slide, down 3.6 basis points to 2.098%. The VIX continues to decline now trading below the $16 level.

A wrath of US data saw limited reaction. US weekly jobless claims came in unchanged at 218,000, still relatively close to the recent cycle lows, also providing a supporting view that the labor market remains strong. US first quarter productivity posted a 3.4%, a miss of the 3.5% estimate analysts provided and down from the 3.6% prior. The US trade deficit for the month of April also narrowed modestly to $50.8 billion. The big takeaway is that US good shipments to China dropped 20% year-to-date to $8.5 billion. US economic data is only get worse as the effects of the multi-front trade wars will start to hit the May data. Fed rate cut expectations by the end of the week could see the June meeting be a live one. Current expectations are only for 21.3% chance for a rate cut at the Fed’s June 19th meeting.

- EUR – No surprises from ECB; sees rates at present levels at least through H1 2020

- MXN – Peso falls as talks gets extended and Fitch cuts rating to BBB

- Oil – Bear Market Bounce

- Gold – Bullish Sentiment in place; rising along stocks

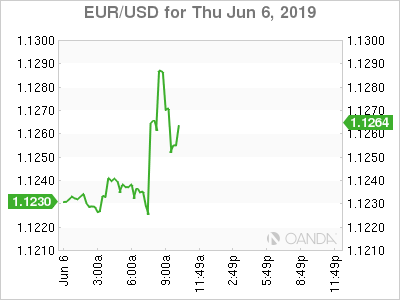

EUR

The European Central Bank (ECB) statement went as expected, with the biggest change being the change in forward guidance which now calls for rates to stay at present levels at least through H1 2020. They announced the new long-term loan rate can be as low as Depo Rate plus 0.1 percentage points.

The market reaction to the ECB saw the Italian 10-year yield rising 2.5 basis points to 2.491%. The euro also whipsawed, initially to session lows than turning positive and up 0.3% to 1.1250. The statement was not as dovish as many thought it could have been. Markets are still pricing in the next move to a rate cut, with the January meeting being a coin flip.

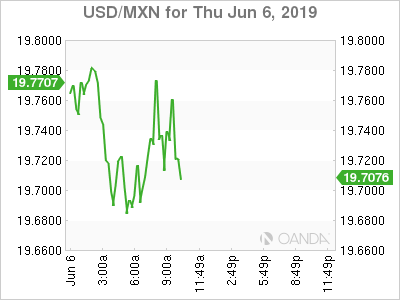

MXN

The Mexican peso remains on soft footing after US and Mexico trade officials failed to reach a deal on immigration and tariffs at yesterday’s meeting. President Trump noted that progress was made but that it was not enough. Trump said talks will resume on Thursday, but that tariffs will take effect on Monday. Expectations are growing for Mexico to get hit with tariffs. Mexico consistently remains optimistic but markets are starting to doubt a deal will get done before the June 10th deadline.

The peso was also weighed down by the news rating agencies were lowering their stances on Mexico. Fitch cut their sovereign rating one notch to BBB, which is just two notches above junk status and Moody’s revised their outlook to negative while affirming their A3 rating.

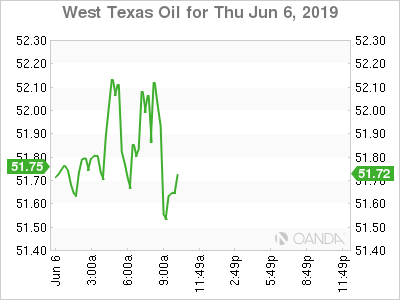

Oil

Crude prices are positive this morning following the move into bear market territory that stemmed from the surge in US stockpiles. The rebound is mostly profit taking and some bets that the we will see some constructive outcomes in trade talks potentially alleviating global demand concerns.

Oil prices could see some further gains if we continue to a risk-on tone with US equities combined with a softer dollar. Geopolitical risks have done little to support crude here, but we should start seeing that become a focal point as we enter a long pause until the June 28-29th G20 summit for a meaningful update on the US-China trade war. We could see resistance start to form around the $55 a barrel level for West Texas Intermediate crude.

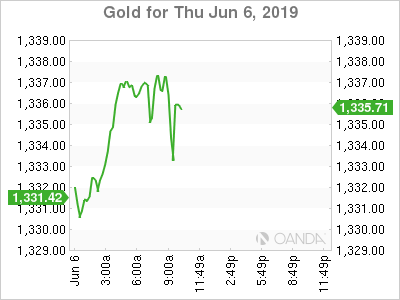

Gold

Gold prices are still rallying higher, but are finding formidable resistance from the February 20th high of $1,349.80. The yellow metal still remains bullish, especially as it is still able to rise on days when equities are climbing higher. The safe-haven is also benefitting on softer dollar flows. If we continue to see deterioration in US data, especially with tomorrow’s non-farm payroll report, we could see that be the catalysts for gold to break above $1,350. If the labor market which has been the backbone to the US expansion is starting to weaken, the Fed’s potential rate cuts will likely become a certainty, with possibly two cuts happening before the end of summer.

{kind=link}