Global equities continue to maintain a cautious tone ahead of key earnings results from the banks that will paint a clearer picture of how of the strength of the US consumer. So far Citigroup and JP Morgan noted that the US consumer is healthy. US futures are little changed as European stocks trade mix. Germany’s ZEW survey came in softer than expected and supports the argument that the ECB could act soon to mitigate the downward pressures to the eurozone’s largest economy. The ongoing trade dispute between the world’s largest economies continues to weigh on the expectations for the German export sector.

USD

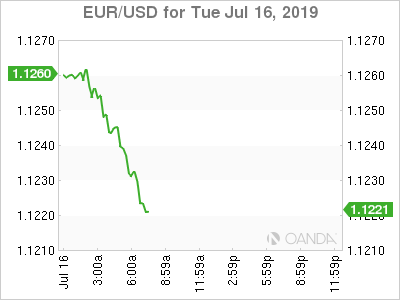

The dollar rallied against most of its trading partners, with the strongest gains against both the euro and pound. The dollar’s gains could be short-lived however if we see the morning release of US retail sales and factory data continue the recent string of further deterioration. While market pessimism is running high, traders should not be surprised if we a slightly better performance with the morning data since yesterday’s Empire manufacturing survey showed some signs of stabilization and Citigroup’s earnings highlighted a strong US consumer.

The dollar’s gains were strongest to the British pound as some analysts see the risks of a no-deal Brexit rising to a coin flip. Brexit negotiations seem to firmly be deadlocked and we will likely see tough banter until we see the next Prime Minister take office next week. The Irish backstop will once again be a key sticking point that the EU, that will likely see either candidate, Hunt or Johnson, argue it needs to go or we will see a hard Brexit. The UK economy is still surprising with decent data, labor came in mixed, while wages rose more than expected.

JP

JP Morgan shares initially fell despite an earnings beat as they joined other banks in cutting their Net Interest Income outlook. Just like Citigroup, equities trading took a hit for JP Morgan down 12% on annual basis, slightly worse than the analysts’ consensus. The results overall were not too and the key takeaway for the overall economy is that they see positive momentum with the US consumer and healthy confidence levels.

Oil

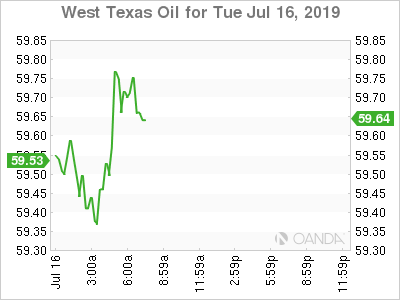

Crude prices are stabilizing after yesterday’s slide as Gulf of Mexico production begins to come back online as the first major test of Hurricane season eased. US stockpiles are expected to ease for a fifth consecutive weak, with stockpiles dropping nearly 3 million barrels last week. The situation between the Persian Gulf remains tense as Iran continue to take the next steps in enriching uranium beyond levels specified under the 2015 nuclear deal. Geopolitical risks and disruptions with US production could support crude prices in the short-term.

Gold

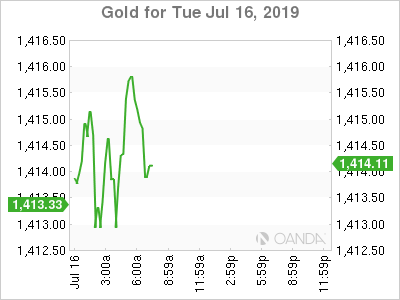

Gold prices continue a summer doldrum consolidation pattern as market participants await further clarity on how dep the Fed’s rate cut path will be. The four largest central banks are set to unleash fresh stimulus in the second half of the year and gold’s bullish outlook remains intact with short-term resistance resting at the $1,500 an ounce level.

Bitcoin

Treasury Secretary Mnuchin joined the crypto-skeptic club yesterday, reiterating the Trump’s administration concerns on privacy and security. The regulatory future for Bitcoin and other digital coins is going to be a bumpy road. Facebook’s Libra has a dartboard on its back and eventually, that could help Bitcoin.