- Fed meets on Wednesday as US inflation stays elevated

- Will Friday’s jobs report bring relief or more angst for the markets?

- Eurozone flash GDP and CPI numbers in focus for the euro

- Chinese PMIs and New Zealand employment to be watched too

Will the Fed put rate cut hopes in more peril?

The upcoming week looks sure to be an action-packed one for the US dollar, as besides an FOMC meeting and the April jobs report, there’s a flurry of other data on the US agenda that will give traders little time to rest.

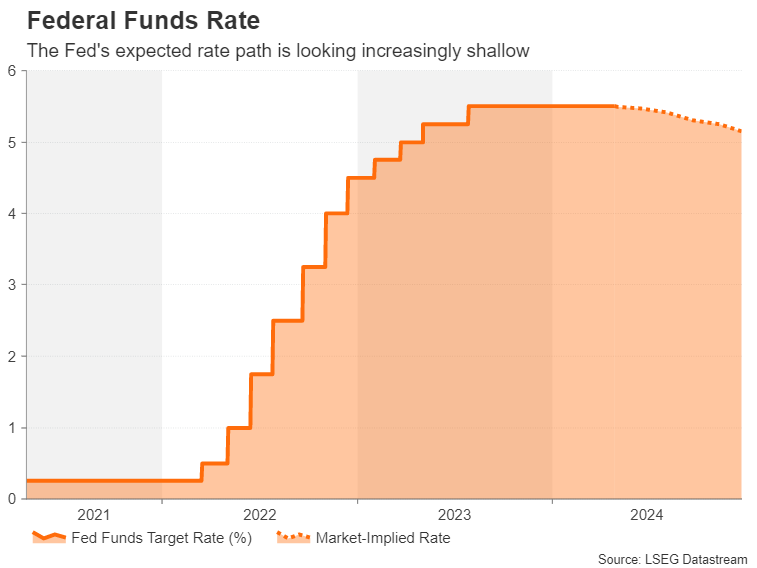

The main focal point during the first half of the week will be the Federal Reserve’s policy decision on Wednesday. It wasn’t that long ago that the May meeting was seen as the one where policymakers would set in stone the path to a June rate cut. However, following the string of hotter-than-expected inflation and employment data, the timing has moved further out into the future, with a cut seen unlikely before September.

With no updated FOMC projections to accompany the May decision, investors will be hanging on every word to come out of Chair Powell in his press briefing for any clues as to how soon the Fed will begin easing policy. Those clinging on to hopes that a summer rate cut is still possible will probably be disappointed.

The most recent commentary from Fed officials suggests committee members are more than comfortable staying on pause for a while longer, although the majority continue to foresee some amount of easing later in the year. Powell will likely reiterate the need for patience but still hint that rate cuts remain on the cards.

What investors will be trying to gauge, however, is how confident Powell is on inflation coming down substantially over the coming months that would allow policymakers to loosen their restrictive stance. If Powell strikes a somewhat more hawkish tone than his usual more balanced approach, the US dollar could resume its uptrend.

A labour market that won’t cool

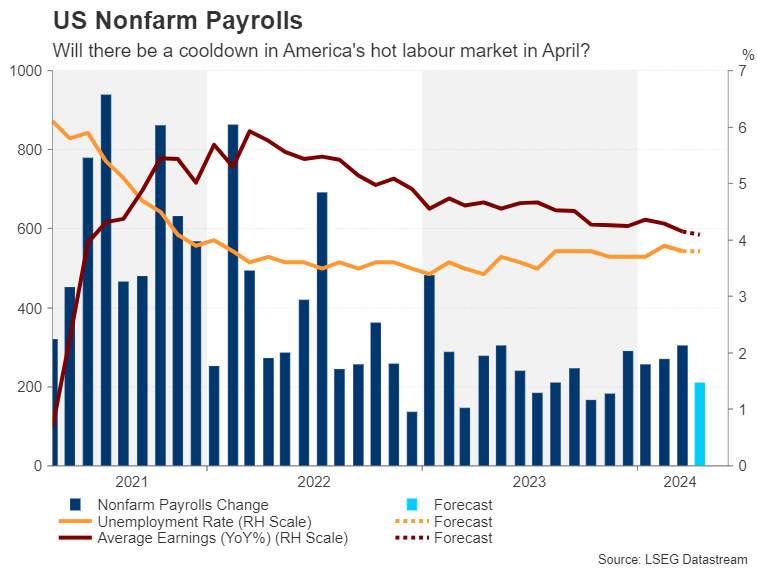

In the event there’s an absence of any fresh signals from the Fed, investors will turn their attention to Friday’s nonfarm payrolls report. Far from slowing, the US economy added an astonishing 303k jobs in March. Analysts expect a figure closer to 210k in April, while the jobless rate is forecast to have stayed at 3.8%.

The crucial factor here is whether wage increases will remain moderate and continue growing at slightly more than 4.0%. Any acceleration in average hourly earnings could spark a bigger panic about fading rate cut bets than an upside surprise in the headline payrolls print.

Also on investors’ radar next week are the ISM manufacturing and non-manufacturing PMIs for April, due on Wednesday and Friday, respectively. Following the softer-than-expected services PMI by S&P Global, a similarly weak ISM services PMI could offset the effects from potentially stronger jobs data and a hawkish tilt by the Fed.

In other releases, quarterly employment costs will be watched on Tuesday along with the Chicago PMI and the consumer confidence index. On Wednesday, there will be more labour market indicators consisting of the JOLTS job openings and ADP employment survey.

Euro sets sights on GDP and CPI update as June cut nears

Barring surprisingly strong wage figures awaited by the ECB at the end of May, a June rate cut seems to be a done deal. What is less certain is the rate path thereafter. Market pricing for the year end has fallen below 75 basis points (~3 rate cuts) in recent weeks and Germany’s influential Bundesbank head Joachim Nagel has warned that a June cut does not necessarily have to be followed by a series of further reductions.

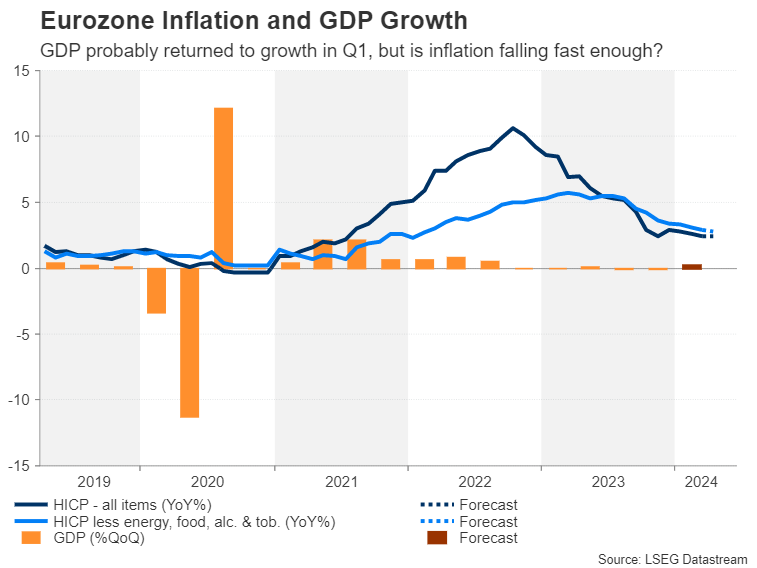

Preliminary readings on first quarter GDP and April CPI due on Tuesday will likely further shape expectations about the rest of 2024, though the probability for June is unlikely to budge much unless there’s a big deviation from the forecasts.

The euro area economy likely expanded by 0.2% quarter-on-quarter in the first three months of the year after flat growth in Q4. An improving economic outlook would lessen the urgency for the European Central Bank to cut rates aggressively so policymakers would have to see further declines in inflation to maintain a dovish stance. Headline inflation is projected to have stayed unchanged at 2.4% in March.

The euro is currently trying to establish a foothold above the $1.07 handle; whether it succeeds will depend on which way the incoming data turns.

Chinese PMIs and New Zealand jobs on the way

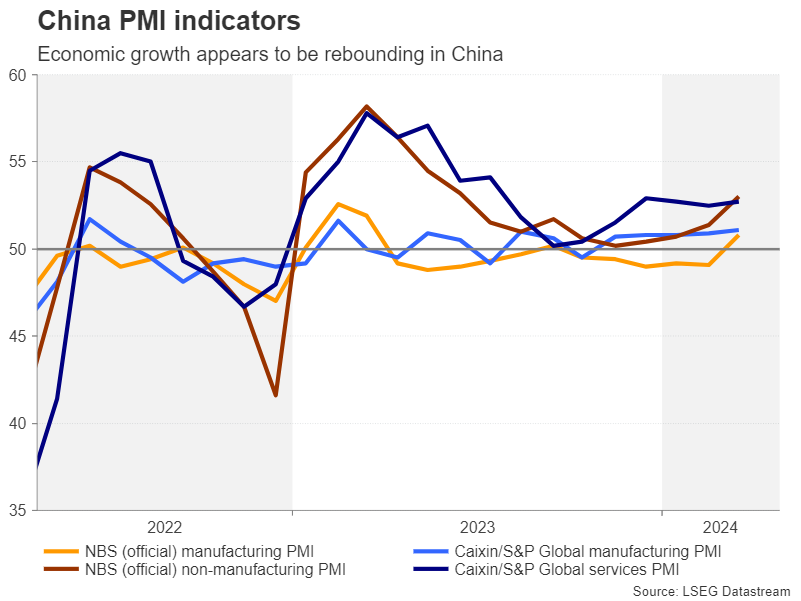

Another region enjoying a bounce back in economic activity is China. The official composite PMI climbed to the highest since May 2023 in March, although much of it was driven by the services sector and the recovery in manufacturing remains tepid.

The latest PMI readings from both the government and Caixin/S&P Global are out on Tuesday.

If the economy gathers further momentum in April, that would bode well for risk-sensitive assets like stocks and oil, and commodity-linked currencies such as the Australian and New Zealand dollars.

In New Zealand, the local dollar will also be keeping an eye on domestic employment numbers scheduled for Wednesday. First quarter data on jobs growth, the unemployment rate and wages might offer clues as to how soon the RBNZ is likely to cut rates after the central bank recently gave its strongest indication yet that the next move will be down.

The kiwi could come under pressure if the labour market appears to be slowing.

Elsewhere, Canada publishes monthly GDP estimates on Tuesday and preliminary industrial production numbers for March are due out of Japan on the same day. Switzerland will release April CPI figures on Thursday and on Friday, Norway’s central bank announces its decision on interest rates.

{kind=link}