The Fed initially disappointed markets participants expecting a strong dovish message. The path for future rate cuts is likely as it will be needed to sustain the expansion and more importantly to help fight off disinflationary pressures. Today’s decision should have been unanimous, but Rosengren and George dissented, a sign the argument for more cuts will likely be difficult. The Fed will also the end balance-sheet runoff on August 1st, implying they will reinvest $83 billion of Treasuries over the next two months.

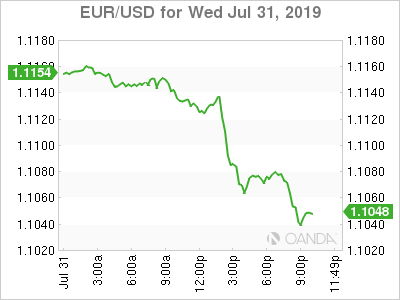

The dollar surged initially as financial markets focused on the hawkish aspects of the statement: they did not clearly signal a lower rate path schedule, ending the balance-sheet drawdown two-months early and that they could not get a unanimous vote.

Press Conf (mid-cycle comment)

Powell’s press conference did little support dovish bets after he stated today was a mid-cycle adjustment to policy. An easing cycle was expected by many as the longer-term inflationary trends show monetary policy has been ineffective over the last batch of hikes while the economy has been so strong. Powell’s further clarified that today’s rate cut is not he start of an easing cycle.

Powell is no stranger to policy mistakes and today’s press conference saw him try to correct an earlier slip. Stocks rebounded off their lows after he stated, “It’s not the beginning of a long series of rate cuts. I didn’t say it’s just one.”

USD/Stocks

The dollar could see further momentum here as today’s decision derailed many dovish bets. Key technical levels could be breached on the euro and Australian dollar. US stocks sold off during the presser and could see further pressure as we are still not far from the record high levels. The bullish case remains intact, as the US consumer remains strong and we could very well see the Fed eventually commit to an easing cycle with no progress with inflation and as global growth concerns rise.

Trump

President Trump is probably regretting not reappointing Janet Yellen. Traders should not surprised, if he resumes his harsh tone towards the Fed and possibly becomes more supportive in delivering rhetoric about dollar intervention.

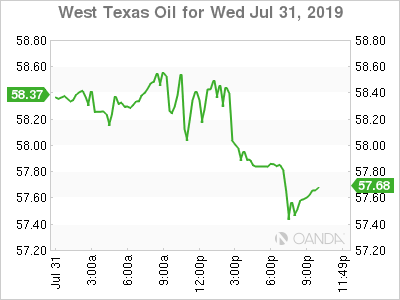

Oil

Energy prices whipsawed following Fed but remained higher on the day following another bullish stockpile report. Commodities should still see some support on easy money flowing throughout all the major central banks in the world. The Fed was not dovish as many hoped but they kept the door open for future cuts.

US stockpiles declined to the lowest levels since May and the overall larger than expected draw with crude inventories should provide a strong backdrop for higher prices. The trend for lower US oil inventories continues and with geopolitical risks still on the mind of energy traders, we could see oil continue to stabilize here.

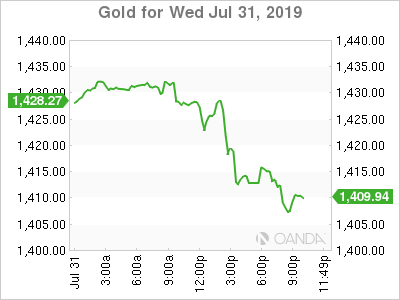

Gold

Muted inflation is likely the key here for gold prices and after recovering earlier losses from the initial Fed reaction, gold could continue to rally. All the major central banks, Fed, BOJ, ECB and PBOC are likely to deliver additional stimulus in the coming months and we should see gold be a favored spot as investors seek better returns than debt that has negative returns. The press conference saw prices sag again after the Fed noted today’s action as mid-cycle adjustment to policy and not clearly stating it was a start of an easing cycle.

{kind=link}