The euro area is on the brink of yet another crisis, with Germany likely to enter a technical recession soon, as the export-heavy economy feels the burn of the US-China trade war and of Brexit worries. Although the ECB is preparing another dose of easing, monetary policy is already exhausted, and fiscal policy needs to step up. Sadly, any German stimulus is unlikely to be large and may take long to arrive, so any sustained rebound in the euro seems far away still.

Perfect storm

Dark clouds are gathering over the European economy once again, but this time may be worse, since the weakness is not just a phenomenon seen in periphery nations – it’s widespread. Germany is at the center of this slowdown, having contracted in the second quarter, and is on track to shrink again in the third as the nation’s central bank recently warned. If so, that would constitute a technical recession, defined as two consecutive quarters of negative growth.

The Eurozone’s largest economy is being battered from all sides: its massive car industry is in turmoil following the emissions scandal, the escalating US-China trade war is hitting exports, and deepening fears of a no-deal Brexit are sapping business sentiment. These are especially worrisome for an economy that is reliant on foreign demand for its products, and true enough, forward-looking surveys like the ZEW economic sentiment index are pointing to further deterioration in the German outlook.

The rest of the ‘big four’ – France, Italy, and Spain – are not doing particularly well either. The story is very similar, with trade tensions hurting the manufacturing sector of these economies, which in turn is starting to infect the far bigger service sector. Of course, Italy is facing a political crisis too, and seems headed for flat growth this year.

Stimulus time

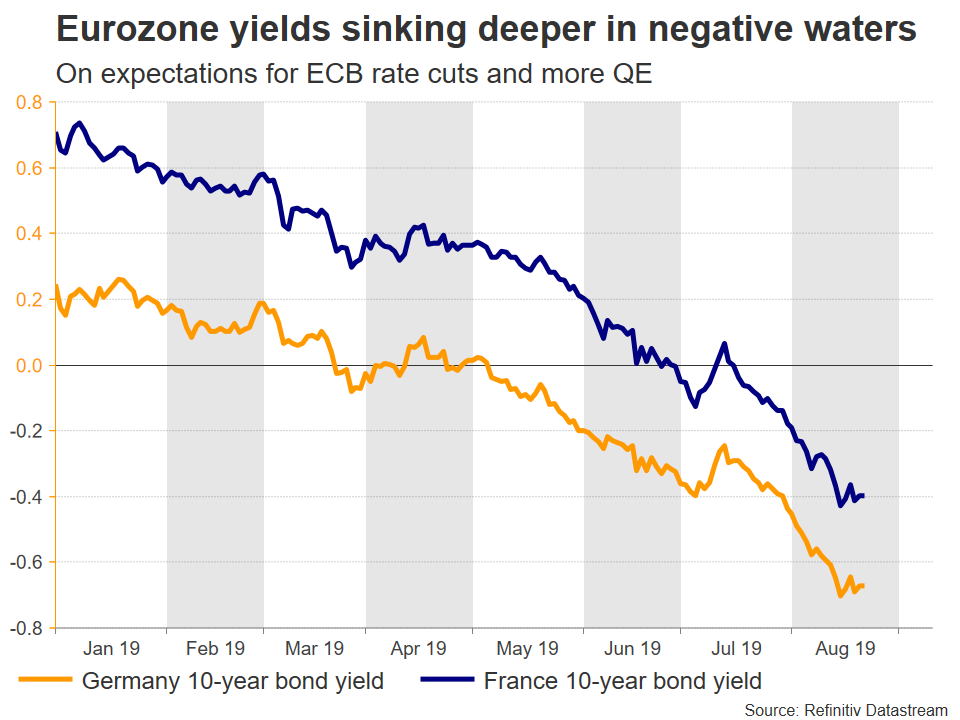

Naturally, the reaction by the European Central Bank (ECB) has been powerful, with policymakers quickly abandoning their rate-hike plans and signaling their readiness to add more monetary stimulus as soon as next month to support the ailing economy. While the size and dimensions of any stimulus bundle are still uncertain, it will probably involve interest rates being cut deeper into negative territory and a resumption of the Quantitative Easing (QE) program.

Alas, monetary policy in the euro area is already exhausted after years of heavy money printing, and the benefits of policies like QE are likely to face diminishing returns this time around. Hence, at some point the central bank could experiment with even more unconventional tools, like adding European stocks to its asset purchases instead of just buying bonds.

Still, monetary policy is unlikely to be effective on its own even if such policies are implemented, and fiscal policy will probably need to play a much greater role for the euro area to regain its footing.

Fiscal conservatism

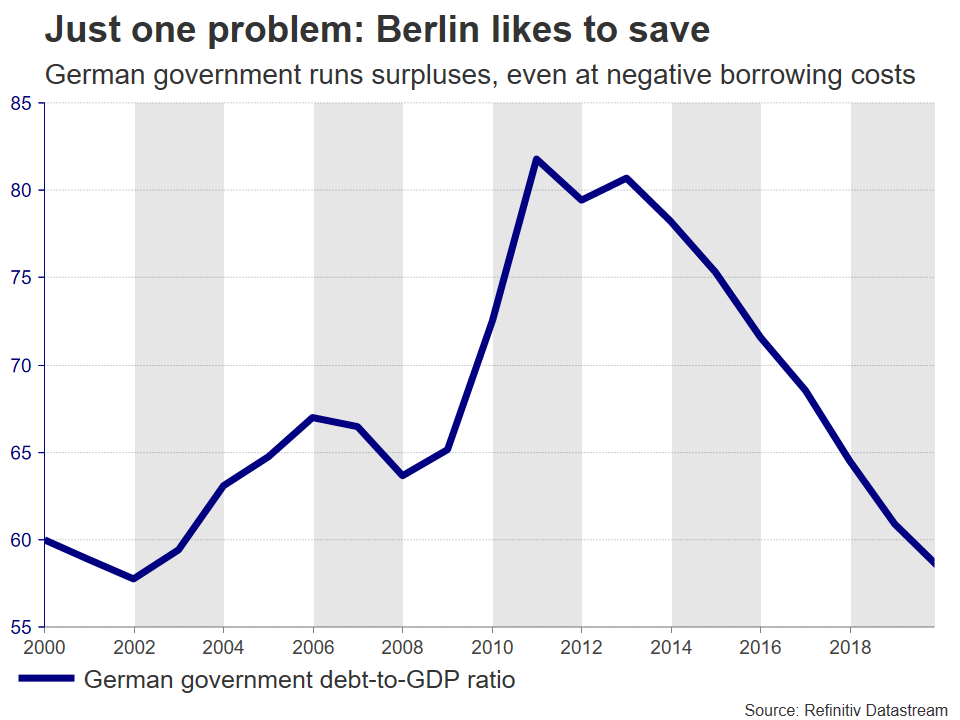

There’s just one problem. The only large European economy that has a low debt-to-GDP ratio and therefore has ample space for fiscal stimulus is Germany – and Berlin doesn’t like deficits. Not only does Germany balance its budgets, it also runs giant surpluses, which means the government is saving money.

This is bizarre because with German 10-year bonds now yielding -0.66%, markets are effectively willing to pay the government money for it to borrow, and it is still not spending. Even for a country as fiscally conservative as Germany, that makes no sense – you can literally borrow today and still see your debt levels decline over time, especially in a positive inflation environment.

Too little, too late?

On the bright side, Germany’s finance minister recently floated the idea of a €50 billion stimulus package to boost growth if the nation slips into a recession. While this shows that Europe’s powerhouse is at least open to the idea of spending more, his plan is also worrisome for two key reasons.

First, waiting for a recession to hit before you act is generally a bad strategy – you want to avoid the negative impact on business sentiment and the consumer as much as possible. As Fed Chairman Jay Powell put it recently: “an ounce of prevention is worth a pound of cure”. Second, the size of the proposed €50bn package is tiny for an economy of €3.4 trillion, as it only amounts to 1.5% of GDP.

Unfortunately, any attempt to unleash a stimulus package without the economy being in real trouble, or to significantly increase its size, would probably face fierce political opposition domestically.

The bottom line

Therefore, the European economy is faltering, and while the central bank seems ready to act with force, any meaningful fiscal stimulus probably won’t be delivered any time soon. Meanwhile, the external risks are not going away either, and may in fact intensify further. The US-China conflict is heating up and judging by recent comments, Trump could also hit Europe with tariffs before long. Likewise, a chaotic Brexit in October would leave deep scars on the euro area as well, not just Britain.

What does all this mean for the FX market?

All in all, these paint a dark picture for the euro, particularly against safe-haven currencies with ultra-low interest rates, like the Japanese yen and Swiss franc. Both could soar if Europe deteriorates, though any gains in the yen may be larger, as the Swiss National Bank (SNB) still intervenes in the FX market to weaken the franc. Similarly, since neither the Bank of Japan nor the SNB can ease much further, while the ECB will do so, there is also a monetary policy convergence story that may benefit these haven currencies.

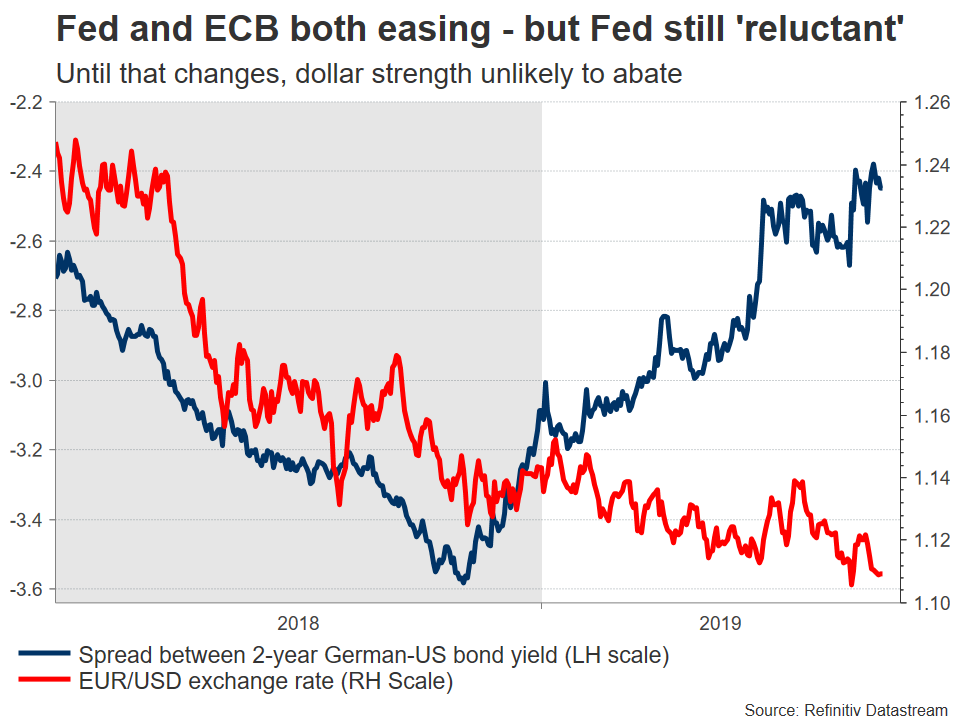

Against the dollar, the picture is more complicated. Both the Fed and the ECB are about to ease, and even though the Fed seems reluctant to get the ‘bazookas’ out for now, it has far greater firepower to ease with overall. As such, there is still a case for the dollar to weaken, but only once the Fed starts slashing rates more aggressively or hints at QE of its own, which is unlikely in the foreseeable future. For now, dollar strength seems unlikely to abate, not least because the US economy is in better shape than the rest of the developed world.

From a technical perspective, the big test for euro/dollar will be whether the $1.10 psychological handle holds. A bearish break could signal a resumption of the broader downtrend.

{kind=link}