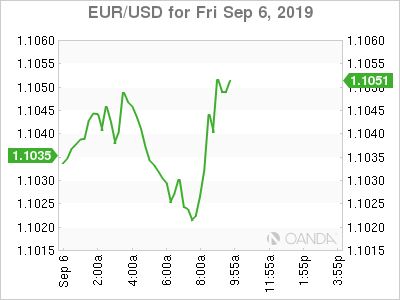

The US jobs report confirms slowdown fears, but by no means is pointing to a recession anytime soon. The US economy saw employment rise by 130,000 jobs in August, with private payrolls posting a soft 96,000 gain, as 25,000 temporary government workers were hired for the 2020 Census count.

The employment report pretty much cements only a 25-basis point rate cut for the Fed at the September 18th meeting. The global growth outlook remains soft and it is unlikely we get a landmark moment in the trade war this month that will ease businesses’ concerns that is making them hesitate with capex and investments. With aggregate weekly payrolls continuing a strong trend and better than expected wages, stagflation concerns may make the Fed a little hesitant in following through with as many rate cuts the market is pricing in over the next six months.

The dollar took a hit across the board and US stocks extended pre-market gains as the punchbowl seems set to overflow with future actions from both the Fed and PBOC.

PBOC

China’s RRR cut was widely expected after the State Council on Wednesday signaled a cut was coming soon on Wednesday. The PBOC’s reserve requirement ratio cut of 50 basis points will take effect on September 16th, with additional cuts taking place for some commercial banks occurring in two steps on October 15th and November 15th.

Chinese futures popped higher but we didn’t see a broader rally as the move was telegraphed and we didn’t see a deeper cut. This round of easing provides modest stimulus to the economy as China will wait to see what happens with the next round of trade talks. The PBOC will unleash a significant wave of stimulus if we see trade talks fall apart again in the coming weeks. Today’s RRR cut is just the beginning and regardless how the trade war unfolds, we will see the further efforts from the PBOC.

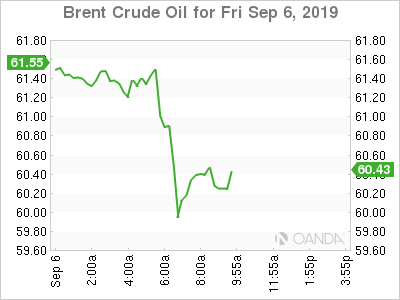

Oil

Oil’s price action is still focused on global demand concerns and was little fazed to the labor market report. The topline numbers were disappointing, but with wages rising fast this year, the mixed report shows signs the US consumer is still strong and demand for crude in America will remain intact.

Another key story for oil is the continued progress Iran is having with the EU in possibly salvaging the 2015 nuclear deal. If we start to see Iran get some relief and tensions ease in the Persian Gulf, we could see that be an unexpected headwind for higher oil prices.

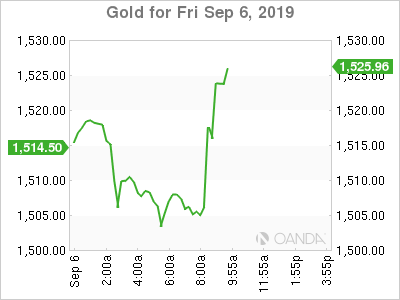

Gold

Gold rallied after job growth struggled in August, but the overall report was not as negative to completely support the doves. Gold’s bullish rally is still facing some exhaustion and this employment report is doing little to fully reinvigorate longer-term bullish bets just yet. Strong support remains at the $1,470 to $1,500 range, but it seems gold will settle comfortably above $1,500 for the week. Until we get to the ECB rate decision, we may see gold trade rangebound.

{kind=link}