Risk sentiment subject to Brexit headlines…

Optimism was buoyed early in the European session on hopes that we might finally see a Brexit deal on October 19th, at the earliest. Headlines emerged that the EU and UK had found a “fair and balanced agreement” with Jean-Claude Juncker President of the EU Commission tweeting “when there is a will, there is a deal”. The news saw heavy risk-on moves take place across G10 FX with AUDUSD climbing +0.8%, building on its gains in the previous session led by a solid Aussie jobs report. NZDUSD caught some of the action too, trading 50pips higher. However, markets quickly checked the rally as it became clear the deal would still need to be ratified by both the EU and UK Parliaments. Party officials from the DUP – who are key to getting anything through UK Parliament – have announced they won’t support the Brexit deal in its current form. Risk-on/risk-off proxy USDJPY tested 108.9 but has since pulled back to 108.6.

…And initial US/Turkey understanding

A positive agreement between US and Turkey which allows Kurdish forces to withdraw from key areas in Northern Syria has helped steady risk through NY. The truce which Trump described would see “millions of lives saved” will now see Turkish Armed Forces control the “safe zone”. The US still appear to be moving forward with Turkey sanctions that would target top levels of government and the country’s economy, however, can be removed if found to be “not operating unilaterally in Syria”.

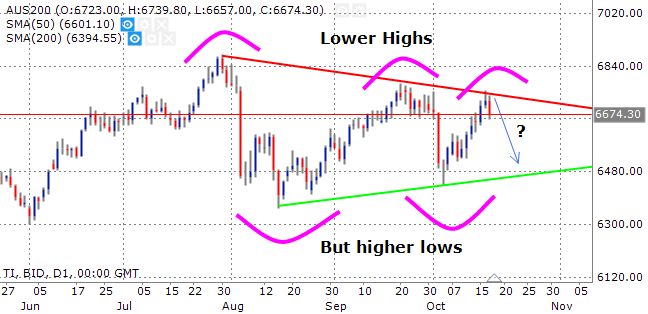

ASX Futures have softened overnight meaning we’re likely to see ASX Cash lower at the open 13pts.

RBA Gov Lowe talks in Washington

RBA Gov. Lowe spoke in Washington this morning at the International Monetary Fund’s “Governor Talk” event. He said it was “extraordinarily unlikely” that Australia would need negative interest rates to stimulate the economy and meet economic targets, but that, low rates alone might not necessarily get the job done. It comes at an interesting time when unconventional monetary policy has slowly crept into the spotlight given Australia’s official cash rate of 0.75% is only three rate cuts from what we think is an effective lower bound (0.00%). Even if Lowe rules out negative rates, there are other forms unconventional monetary policy can take: explicit forward guidance, quantitative easing, funding for credit lending, open market operations, in which we explain in our SPECIAL REPORT: AUD – Unconventional Monetary Policy Primer.

Important data for China complex

Markets are scheduled to catch the release of Q3 GDP and September activity data (Retail Sales, Industrial Output, Urban Investment) today with their official release by the National Bureau of Statistics of China due out at 1.00pm AEDT. The marked focus for traders will be how China’s Q3 GDP y/y reads given it’s expected to print at 6.1% which puts it in proximity to the critical lower bound of China’s target range, 6.0-6.5%. While expectations are for GDP to remain above 6.0%, a negative print would confirm sluggish views on China’s growth and feed into PBOC forward implications. We cover the print in more detail in our SPECIAL REPORT: How Low Can Q3 China GDP Go?.

Current USDCNH spot price: 7.080

Upside pivot level if we see a positive print for GDP (>6.1%) + September activity data: 7.066 (-14pips), 7.05 (-30pips), 7.03 (-50pips).

Downside pivot level if we see a negative print for GDP (<6.0%) + September activity data: 7.066 (-14pips), 7.05 (-30pips), 7.03 (-50pips).