US stocks declined sharply yesterday after doubts emerged about world trade. These problems started on Monday, when Donald Trump tweeted that he would add tariffs on Argentina and Brazil for devaluing their currencies. He argued that these actions hurt American farmers by making South American farm products cheaper. Ironically, Trump’s tweet led to more weakness of Argentinian and Brazilian currencies. Later on, Trump said that he would add fresh tariffs on French goods worth more than $2.4 billion. France said that the EU would retaliate. Yesterday, he said that he was comfortable waiting for a China deal until after the 2020 election. This statement lowered the chances of the first phase of the trade deal. The Dow declined by 300 points while the S&P500 declined by 21 points. The price of gold rose by 1% and reached a high of $1480.

The US dollar declined as the trade war rhetoric increased. Today, focus will remain on the currency, which is the reserve currency of the world. The focus will be on ADP, which will release the private nonfarm payrolls for the month of November. The market expects the data to show that the economy created more than 140k jobs. This will be more than October’s 125k. This data usually comes two days before the official government data that is released by the Bureau of Labour Statistics. The market will also be watching out for the ISM non-manufacturing PMI data. The market expects the number to show a decline from 54.7 to 54.5. Meanwhile, the Canadian central bank will conclude its monetary policy meeting and announce its decision. The market expects the bank to leave rates unchanged at 1.75%.

The Australian dollar declined after the bureau of statistics released the final reading of Q3 GDP data. The numbers show that the economy contracted from 0.5% in the second quarter to 0.4%. The economy rose from 1.4% to 1.7% on a YoY basis. The capital expenditure improved from -1.7% to -0.2% while the chain price index declined from 1.2% to 0.7%. Final consumption declined from 1.0% to 0.3%. This data came a day after the RBA left interest rates unchanged at 0.75% and sounded optimistic about the economy. Meanwhile, in Japan, services PMI improved from 49.7 to 50.3 while in China, they improved from 51.1 to 53.5.

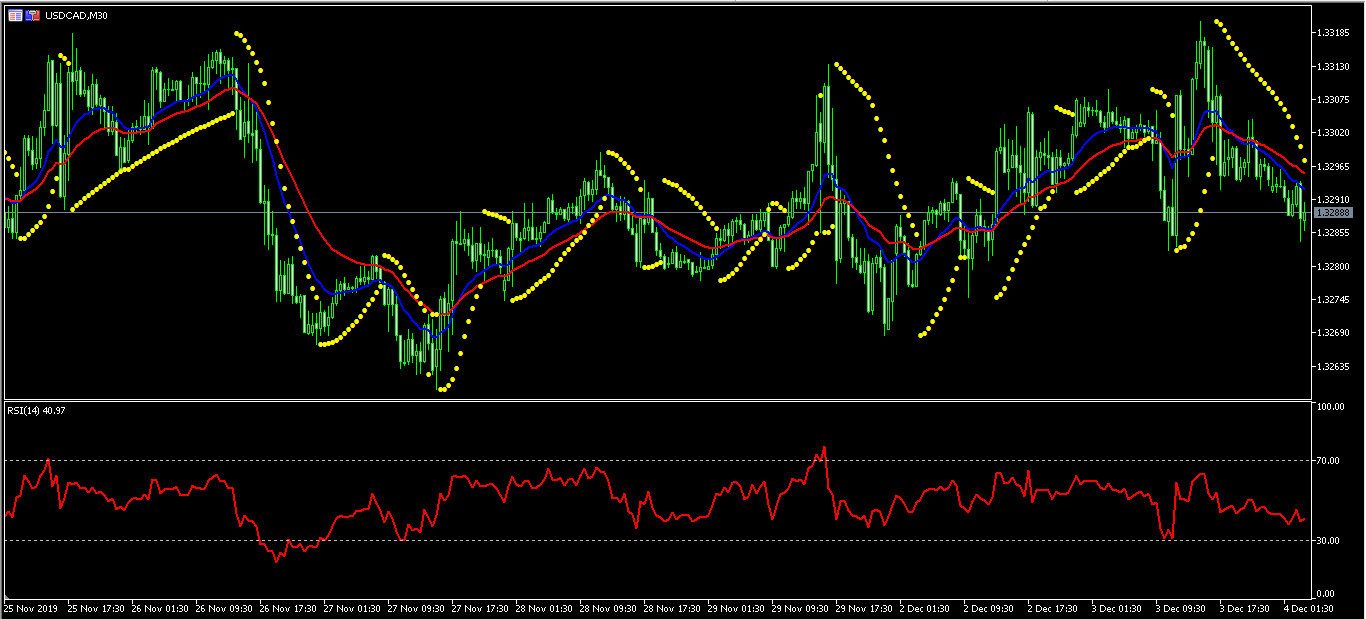

USD/CAD

The USD/CAD pair declined to a low of 1.3285. This was lower than the weekly high of 1.3320. The price is below the 14-day and 28-day moving averages while the RSI has moved slightly lower to 40, on the 30-minute chart. The Parabolic SAR dots are above the price, which is a sign that the price may continue moving lower. Still, this may change depending on the BOC statement.

AUD/USD

The AUD/USD pair rose sharply yesterday after the optimistic RBA statement. The pair rose to a high of 0.6860, which was the highest level it has been since November 11. The pair is now trading at 0.6835, and is forming a head and shoulders pattern. The 14-day and 28-day moving averages appear to be making a bearish crossover. The RSI too is declining. This is a signal that the pair may continue moving lower.

EUR/USD

The EUR/USD pair declined slightly from a high of 1.1092 to the current level of 1.1080. The price is along the 14-day moving averages and slightly above the 28-day moving averages. The price is between the channel that has been forming this week. The RSI has started to decline. The pair may decline today to test the important low of 1.1065.