U.S. Review

Well, That De-Escalated Quickly

- The week began amid rising tensions carrying over from the U.S. killing of Iranian General Qasem Soleimani last Friday. Iran responded with non-lethal airstrikes on U.S. facilities, but President Trump has said the U.S. has no plans to escalate further, and the Iranians appear to have concluded their response for now.

- Compared to just prior to the drone strike, U.S. stocks are higher as is the dollar and the price for a barrel of oil (after spiking briefly) is now about $2.00 lower.

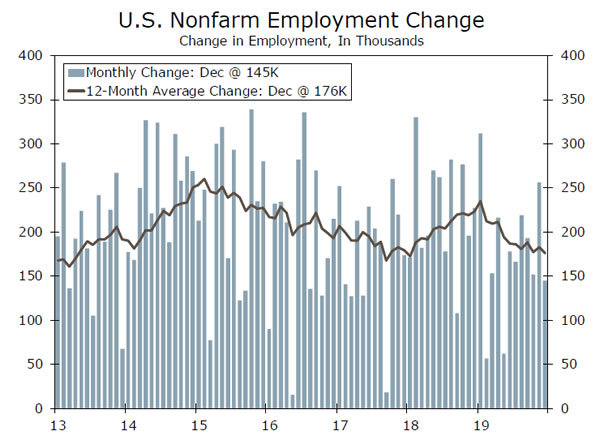

- he job market continued to expand adding another 145K jobs although wages rose the least since mid-2018.

Tale of Two Cities: Manufacturing vs. Service Sector

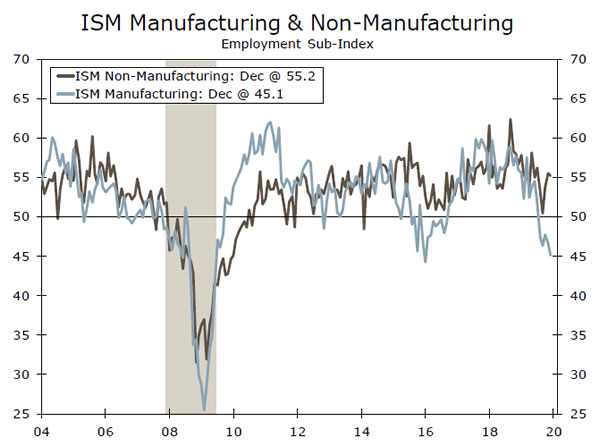

The first major economic indicator to hit the wire in 2020 was the ISM manufacturing report last week, which showed the fastest pace of contraction since the height of the 2008 recession. So when the ISM non-manufacturing report was published earlier this week, financial markets were relieved to see that barometer of the service sector rise to 55.0. That is the fastest pace of expansion in four months.

The shortened holiday shopping season due to a late Thanksgiving this year was referred to a number of times in the report. That gels with our thinking around Holiday Sales. We have been saying that despite a weaker-than-expected retail sales report in November, we still expect a year-over-year Holiday Sales increase of 5.0% as December will effectively get a boost. Even Cyber-Monday (the Monday after Thanksgiving) got pushed into December.

A Slowing in Labor Market Growth

The employment component of the services ISM remained in expansion but slipped a bit from the prior month heralding the slightly lower-than-expected employment report on Friday which showed the U.S. economy added another 145K jobs with the unemployment rate staying put at 3.5%.

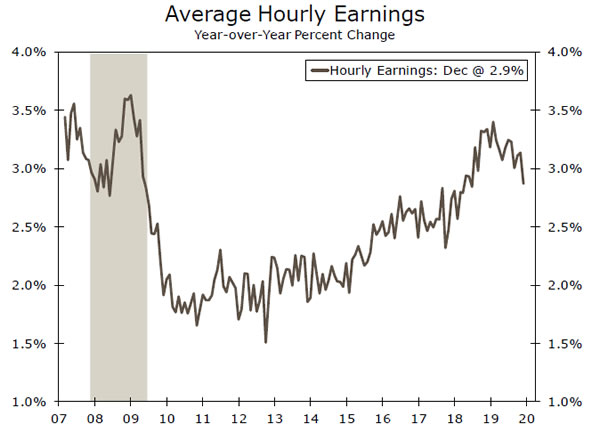

It has been a remarkably good run for the labor market, but this latest report offered some indications of softening even amidst the lowest jobless rate in a half-century. Average hourly earnings edged up just 0.1% in December, after rising 0.3% in each of the prior two months. On a year-over-year basis, average hourly earnings rose by the smallest amount since July 2018.

Still, for the year as a whole, the U.S. economy added 2.1 million jobs with an average monthly gain of 176K jobs. Those are solid numbers, but short of the 223K monthly average in 2018.

For the Fed, the message from the jobs report is that the labor market remains tight, but still not tight enough to put upward pressure on earnings so not much of a threat for inflation. In other words, there was nothing in this report to nudge policymakers from a course of holding rates steady.

Service Sector Resilience

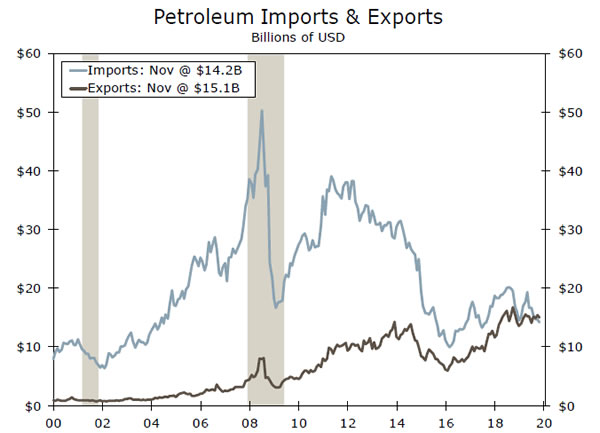

In what is probably the most consequential development for GDP growth this week, the trade deficit narrowed to $43.1 billion in November which, barring an unexpected widening in December, means that trade will be a big boost to fourth quarter GDP.

The boost is welcome but if, as we expect, the recent decline in imports is due to importers pulling forward demand to get ahead of consumer-focused tariffs, it may be set to reverse and be a drag on GDP in coming quarters. Those consumer-focused tariffs were taken off the table with the Phase I trade deal set to be finalized at a formal signing next week in Washington.

An interesting development is that U.S. petroleum exports exceeded imports in November for the third straight month, another reason perhaps why financial markets have (for now at least) shrugged off the crisis in Iran.

U.S. Outlook

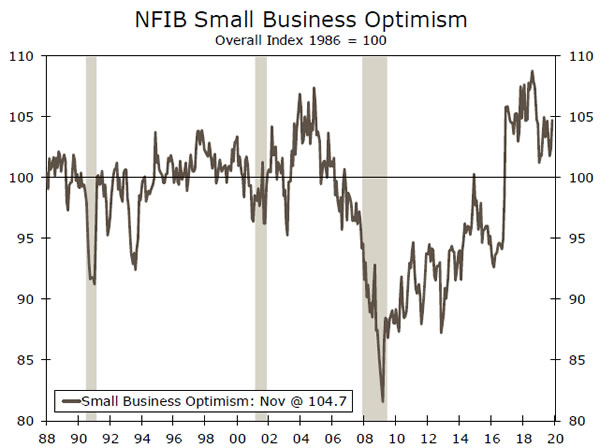

NFIB • Tuesday

Small business optimism may get a boost from the Phase I trade deal with China, which was formally announced by the Office of the U.S. Trade Representative on December 13. Equity markets sure celebrated the deal, although small companies generally have less exposure to foreign economies and international trade. On the other hand, small businesses owners lean disproportionately Republican, so the impeachment of President Trump—which was approved in the House on December 18 but was building for weeks prior—may be giving them some pause (optimism skyrocketed upon his election).

Regardless, optimism remains extremely high on a historical basis, supporting our view that Main Street and the consumer remain healthy. Underneath the headline, we are closely watching small business hiring intentions and selling prices, as these often lead overall nonfarm payrolls and inflation. When the economy turns, it typically does so at small firms first.

Previous: 104.7 Consensus: 104.8

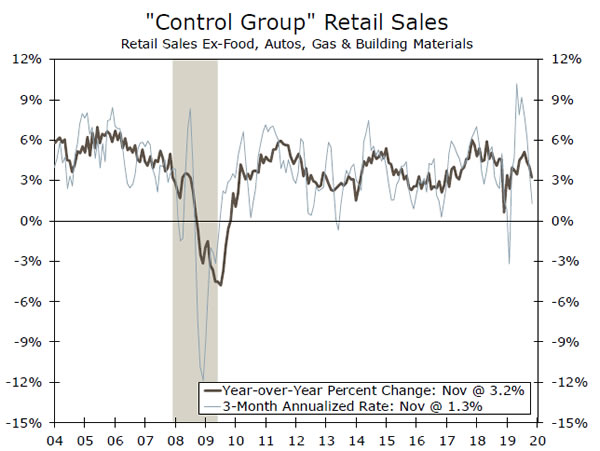

Retail Sales • Thursday

December retail sales could surprise to the upside. Sales in November came in low, rising just 0.2%. Yet there were some notable calendar and data quirks we are monitoring. For one, Thanksgiving was the latest possible day in November this year, meaning that the period between Thanksgiving and Christmas was the shortest possible. With many holding off purchases until Black Friday, we suspect this could have pushed more of the usual spending deluge into December.

Second, Black Friday is not as important as it used to be, and Cyber Monday fell on December 2. Moreover, the seasonal adjustments may be having some difficulty accounting for the paradigm shift towards online shopping. In other words, do not be surprised by a surprise. December aside, we have an optimistic view of the consumer. Spending growth is moderating, to be clear, but it should remain healthy enough to sustain the expansion.

Previous: 0.2% Wells Fargo: 0.3% Consensus: 0.3% (Month-over-Month)

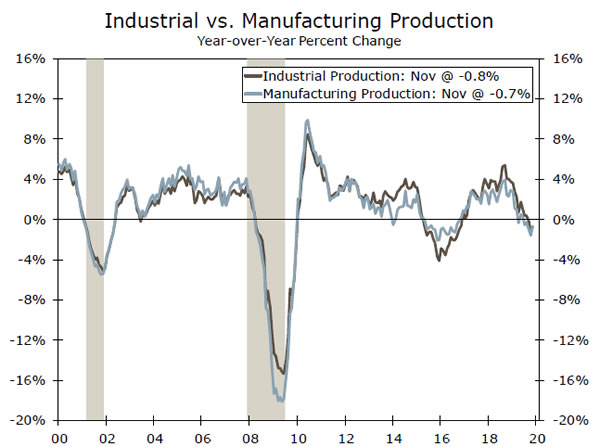

Industrial Production • December

The industrial production (IP) figures have been especially volatile of late due to the strike at GM and Boeing’s ongoing 737 MAX issues. GM’s assembly lines came back on-line in November, resulting in a double-digit surge in autos production, which flattered the overall 1.1% IP increase. This will not repeat in December, which is also when the ISM manufacturing index fell to a ten-year low of 47.2. The stage is therefore set for a weak manufacturing print to end 2019, and the outlook does not improve with the calendar turn, as Boeing suspended 737 MAX production on January 1.

Looking further out, the drop in the ISM may be overstating the weakness in the factory sector, and we would not be surprised to see a gradual rebound after the Phase I trade deal and improvements in global PMIs. Tensions with Iran may impact mining output in coming months, but that is impossible to predict at the moment. We expect industrial production fell -0.3% in December.

Previous: 1.1% Wells Fargo: -0.3% Consensus: 0.0% (Month-over-Month)

Global Review

A (Mostly) Happy New Year

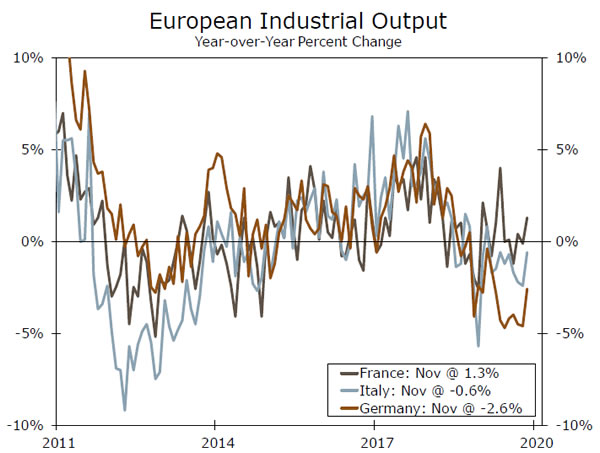

- It was a relatively busy week for international data and events. In the Eurozone, inflation increased in December at the fastest pace since April, an encouraging sign for the ECB, while European industrial data were sturdy.

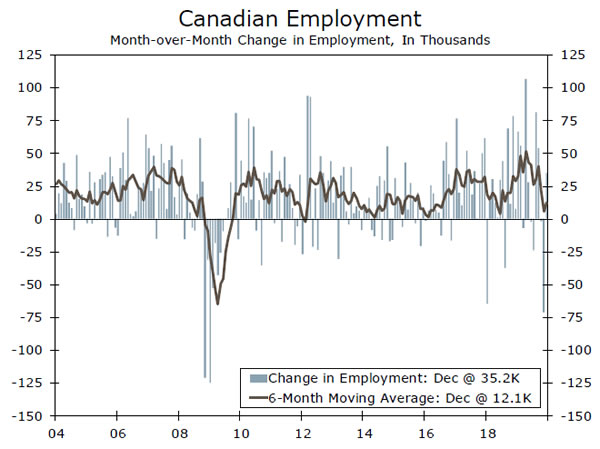

- Canadian employment rebounded in December after two straight months of declines, lessening concerns about a slowdown in job growth.

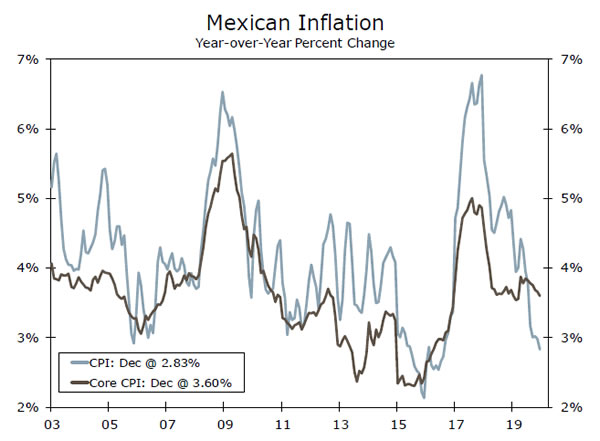

- In Mexico, the data was not as promising, however. Mexico’s consumer prices eased further in December and industrial production disappointed in November, supporting the case for additional monetary policy easing from the central bank.

Solid Data Out of the Eurozone

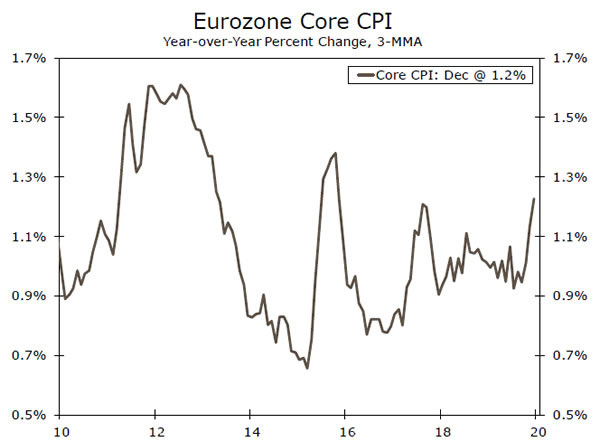

The Eurozone’s headline inflation rose at the fastest pace since April 2019, rising 1.3% year-over-year in December from 1.0% the previous month. The figure was mostly driven by a jump in oil prices in December as the energy sector rebounded, rising 0.2% year-over-year. The core inflation rate—which strips out volatile components such as energy—held steady at 1.3% and the three-month average of core Eurozone inflation edged higher to 1.2%, the strongest pace since 2015. Separately, retail sales rose more than expected in November, up 1% over the month and October’s figure was revised higher. The stronger retail sales data appears to be driven in part by Germany, as its retail sales figure also jumped more than anticipated in November. The recent solid data provides an encouraging sign ahead of the European Central Bank’s policy meeting this month.

Mexico’s Slowing Trend Continues

Over the past two years, Mexico’s consumer prices have eased from its recent peak of 5%. On a year-ago basis in December, headline CPI slowed further to 2.8%, the slowest pace since 2016, while core inflation eased to 3.6%. Meanwhile, November industrial output declined 2.1% year-over-year, but suggested that the pace of the contraction may have slowed. The overall economy has been relatively sluggish and GDP data indicated that the economy fell into a technical recession in the beginning of 2019. Although Mexico was able to exit the technical recession in Q3-2019, GDP rose only a modest 0.01% quarter-over-quarter. With core inflation falling for the sixth consecutive month and growth expectations still subdued, we expect the central bank to continue its easing cycle into the new year. The Mexican peso has been relatively strong over the past several months, which also supports the case for more monetary policy easing from Mexico’s central bank.

Keeping a Close Eye on Canada’s Labor Market

Canada’s economy softened a bit in late 2019, including a slowdown in GDP growth as well as a downshift in the pace of job creation. In that regard, a Bank of Canada governor gave a “fireside chat” this week, offering some recent observations on the economy. Governor Poloz said that damage from the global trade conflict was likely to be permanent and the central bank was watching to see if the impact of the trade disputes spillover to other sectors. He also said that while the trend in the Canadian labor market has been healthy over the past year, the central bank is also watching to see if the recent labor market moderation persists.

There was some better news on the jobs front this week. There was some recovery in December hiring with a job gain of 35,200, after a large November employment fall of 71,200. Moreover, that increase reflected a rise of 38,400 in full-time jobs, and a decline of 3,200 in part-time jobs. The unemployment rate dipped to 5.6% in December, while the pace of wage growth remained healthy. After a couple of disappointing months the December employment report was a hopeful sign, and should keep Bank of Canada monetary policy on hold in the coming months.

Global Outlook

U.K. Inflation • Wednesday

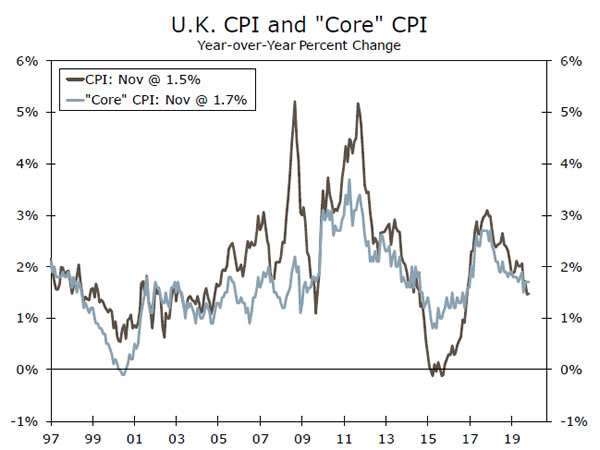

U.K. inflation held steady at 1.5% year-over-year in November, the lowest rate in three years, while core inflation remained at 1.7%. At its December policy meeting, the Bank of England noted that it expects headline inflation to slow further to around 1.25% by spring 2020, but then rise to slightly above the central bank’s 2% target towards the end of the forecast period. Next week’s inflation figures could be slightly restrained by the spike in the pound over the month, however the large run-up in oil prices in December could act as an offset. The market currently expects U.K. headline inflation to rise 1.5% year-over-year and 1.7% for core, in December.

December retail sales is also on next week’s schedule, and could have some market impact. Following a surprise fall in November, retail sales is expected to rise 0.8% month-over-month.

Previous: 1.5% Consensus: 1.5% (Year-over-Year)

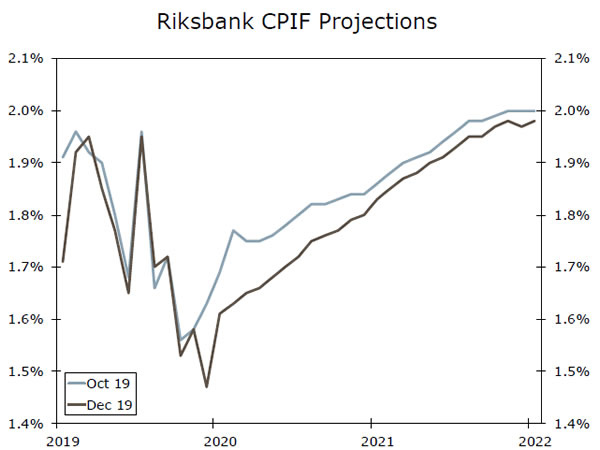

Sweden Inflation • Wednesday

Swedish inflation figures topped estimates in November as CPIF inflation firmed to 1.7% year-over-year and CPIF inflation excluding energy quickened to 1.8%. Sweden’s economic signals, for the most part, have held up better than expected in November, and with inflation close to the central bank’s 2% target, the Riksbank had some room to hike interest rates at its December policy meeting.

At that meeting, the Riksbank slightly decreased its forecast for inflation for 2020-2021 (chart to the left) due to the krona’s effects on inflation wearing off, while lower energy prices also had a marginally weakening effect. Looking ahead to next week, inflation is expected to increase at just 1.7% year-over-year in December, while inflation ex-energy is forecast to rise 1.8%. In our view, a weaker-than-expected inflation print would likely keep the Riksbank on hold for an extended period of time.

Previous: 1.8% Consensus: 1.8% (Year-over-Year)

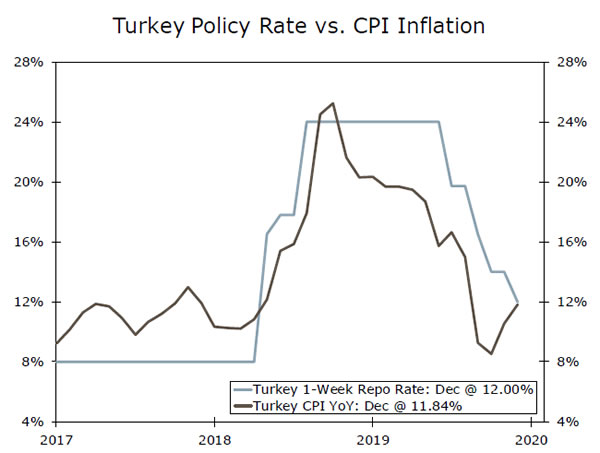

Turkey Policy Rate Decision • Thursday

Turkey’s central bank cut rates further at its December policy meeting, opting to reduce its one-week repo rate 200 bps to 12.00%. The decision to ease monetary policy amid increasing price pressures and underwhelming growth performance, reinforces our view of a lack of central bank independence in Turkey. In addition, President Erdogan announced that the monetary policy committee will meet 12 times this year (versus eight times in 2019) and suggested interest rates will reach single digits in 2020, indicating that political pressure on the central bank has not yet eased.

CPI inflation pushed higher to 11.84% year-over-year in December, the second straight monthly increase. The latest increase narrowed the real interest rate to 16 bps (chart to the right). Currently, market participants anticipate a 50 bps cut to 11.50% at the policy meeting next week.

Previous: 12.00% Consensus: 11.50%

Point of View

Interest Rate Watch

Repo Rates Tranquil at Year-End

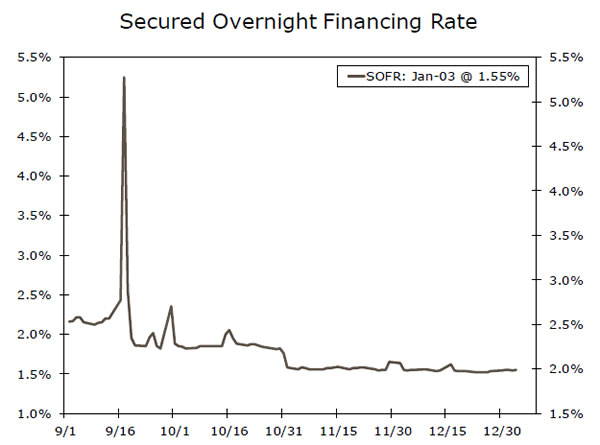

Heading into the end of 2019, there were fears that U.S. Treasury repo rates could be in for a tumultuous ride. Repo rates often rise at quarter/year end, and the previous year was no exception: the secured overnight financing rate (SOFR) spiked more than 50 bps on December 31, 2018, and then 15 more on January 2, 2019. Furthermore, repo rates skyrocketed even more dramatically in September 2019 (top chart), and although they had mostly been tame since, it remained unknown whether the Fed’s actions taken over the ensuing months would be enough to keep repo rates from spiking at year end.

In the end, money market rates were incredibly tame over year end. SOFR set at 1.55% on December 31, perfectly in line with the interest rate paid on excess reserves (IOER) and the effective fed funds rate. Thus, it appears the Federal Reserve’s multi-pronged approach to keeping a lid on repo rates was largely successful.

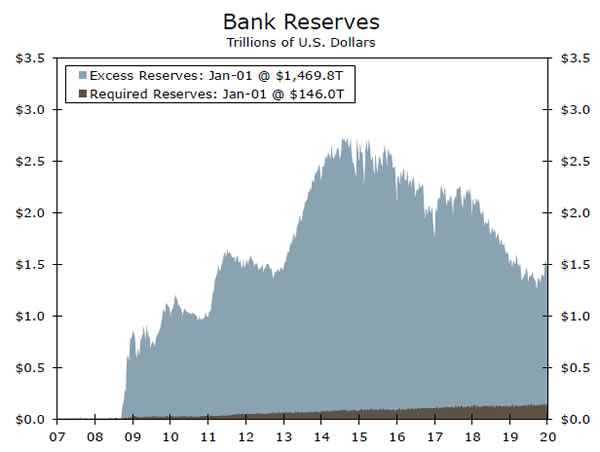

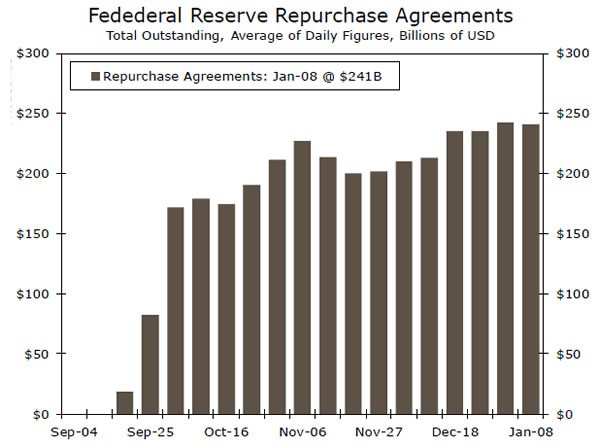

What were the tools that the Fed utilized? Since October, the Fed has been purchasing Treasury bills in order to increase bank reserves in the financial system, and as a result excess reserves have risen by about $200 billion from their September lows (middle chart). In addition, the Fed has become a large and active lender in the repo market. At the turn of the year, the Fed had about $242 billion of repurchase agreements on its balance sheet (bottom chart). Persistent downward tweaks to the rate paid on IOER and reverse repurchase operations also likely helped.

Although the recent tranquility in repo markets is a clear success for the Fed, questions remain. Now that year end is past, the Fed will likely begin to reduce some of the support it has offered repo markets. How fast it pulls back, and in what ways, remain open questions. Furthermore, the tools the Fed has used, such as the ad hoc repo operations it has conducted, are likely more operationally intense and inherently uncertain than the central bank would prefer. Thus, a longer-term solution, such as a standing repo facility or some regulatory changes, remain very much in the mix going forward.

Credit Market Insights

Revolving Credit Growth Rolling Over

Consumer credit grew slower than expected in November, as the outstanding level of consumer debt, excluding home loans, increased $12.5 billion. The deceleration from last month’s $19.0 billion gain comes entirely from a slowdown in revolving credit, which is comprised primarily of credit card debt and accounts for less than a third of overall consumer credit. Though it picked up briefly last summer, revolving credit growth has remained fairly subdued this cycle. The more recent moderation can be attributed partially to tougher lending standards. The Fed’s Senior Loan Officer Opinion Survey showed that banks were less likely to approve credit card applications in Q3 2019 than they were a year prior, particularly for borrowers at the lower end of the credit spectrum. While consumers have been relying less on their credit cards, non-revolving credit has continued to increase at a steady clip, rising 5.8% over the month and 5.0% over the year. This form of credit is comprised mostly of auto and student loans and continues to take up an increasing share of household debt.

The bulk of household debt, however, is still made up of home loans. Though mortgage debt may feel less burdensome in 2020, given that many were able to refinance at a lower rate in 2019. The Mortgage Bankers Association’s refinancing index is currently up 113% over the year, after hitting a three year high in August. This refi boom also helped Americans cash out roughly $54 billion in home equity, according to Freddie Mac.

Topic of the Week

Potential Implications of Iranian Crisis

The week began amid rising tensions carrying over from the killing of Iranian General Soleimani last Friday. Iran responded this week with non-lethal airstrikes on U.S. facilities, but President Trump has said the U.S. has no plans to escalate further and the Iranians appear to have concluded their response for now.

Financial markets have more or less settled back to where they were prior to the start of recent hostilities a week ago. Oil prices spiked on the initial news, but quickly settled down and as of this writing the price for crude oil is actually lower than it was prior to the U.S. drone strike that killed the Iranian general. However, if tensions flare again, investors instinctively turn to oil prices as a risk barometer raising questions about potential knock-on effect for the economy.

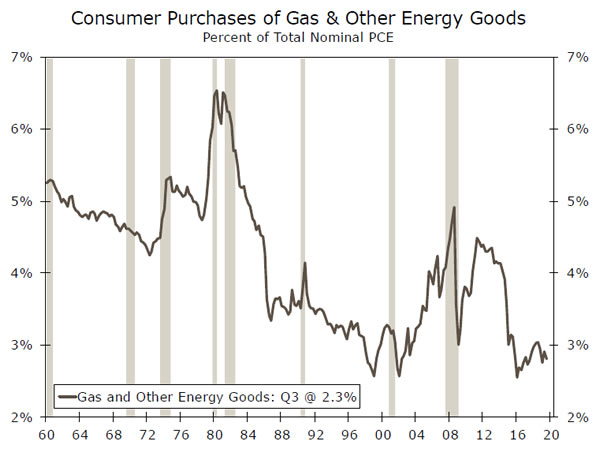

As shown in the top chart, consumer purchases of “gasoline and other energy goods” accounted for roughly 4% of total personal consumption expenditures (PCE) at the time of the oil price shocks in the 1970s. Today, those goods account for only 2% of PCE. So oil prices would need to shoot much higher from their current levels to have a meaningful effect on consumer purchases of other goods and services. (Oil prices more than doubled after the OPEC oil embargo in late 1973 and again following the Iranian revolution in early 1979.)

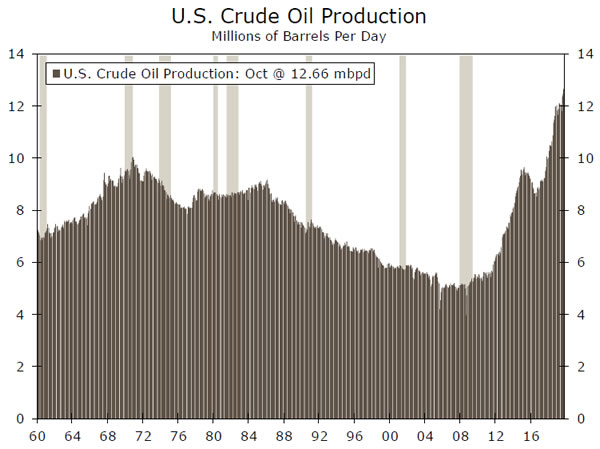

Additionally, the lower chart shows how American production of crude oil has increased over the past decade. This week we also learned that November marked the third consecutive month that U.S. petroleum exports exceeded imports suggesting less reliance on foreign sources. Higher oil prices would actually encourage more investment in the energy sector and what’s more, other industries are not as dependent on oil as an energy source as they were in the 1970s. So the direct effects of the Iranian crisis on the U.S. economy appear to be rather small.

However, the uncertainty that the crisis imparts could potentially be more meaningful. Consumer spending could potentially take a more meaningful hit if a marked cycle of violence were to take hold.

{kind=link}