{kind=link}

The Bank of Canada is widely expected today (10:00 am EDT) to raise its benchmark policy rate for the first time in seven years. It would be a strong signal from policy makers that the Canadian economy is on the path to recovery after years of tepid growth following the global slump in commodities.

The majority who expect a rate hike of +25 bps to +0.75% cite the bullish shift in central bank communications about the outlook and data signalling Canadian output is expanding at its fastest pace in nearly three years.

However, inflation is not pressing, but most G7 economies indicate that they can live with interest rates a tad higher than they are at present and still generate solid growth.

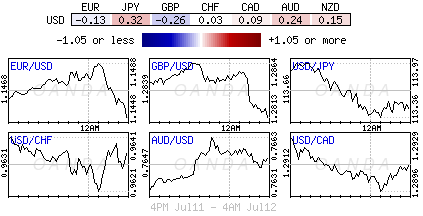

Not all agree that a rate rise is warranted today, if the BoC fails to deliver, given weak inflation and wage gains, and uncertainty that remains over the Trump administration’s trade policy, watch how quickly the loonie (C$1.2921) gets sold off.

Nevertheless, if Poloz fails to hike would be irresponsible, given the recent rhetoric, and definitely lead to more market confusion about the effectiveness of BoC’s communication policies.

Fed Chair Janet Yellen will also begin two days of testimony before Congress, with traders focusing on her assessment of financial conditions.

Note: The only major central banks expected to have moved to +1% base rate over the next year are the Fed and BoC.

1. Global Stocks encounter thin trading

In Japan, the Nikkei shed -0.5% while the broader Topix dropped -0.4% in thin trade before Fed’s Janet Yellen’s comments later today. A stronger yen (¥113.40) in the wake of a fresh controversy for U.S President Trump’s administration hit exporters.

In Hong Kong, the Hang Seng rallied +0.6% for the third straight day to a two-year closing high, boosted by China fund flows and investors’ bargain hunting.

In China, stocks ended lower overnight as investors paused for breath ahead of Ms. Yellen’s address to Congress. The blue-chip CSI300 index fell -0.3%, while the Shanghai Composite Index shed -0.2%. The “Nifty 50” hit a 23-month high before edging -0.2% lower.

In Europe, stocks have opened higher and are maintaining momentum. On the FTSE 100 energy stocks are being supported by an increase in oil prices.

U.S stocks are set to open little changed (+0.03%).

Indices: Stoxx50 +0.6% at 3,484, FTSE +0.8% at 7,387, DAX +0.4% at 7,384, CAC-40 +0.8% at 5,180, IBEX-35 +0.4% at 10,495, FTSE MIB +0.8% at 21,280, SMI +0.7% at 8,935, S&P futures +0.03%.

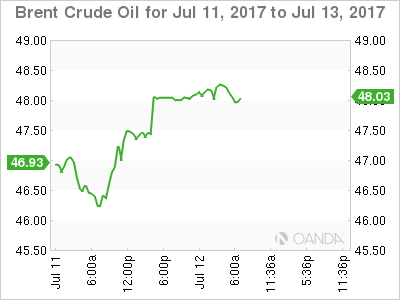

2. Oil gets a lift from inventory levels

Oil prices are better bid ahead of the U.S open in response to a fall in U.S fuel inventories and a cut in the U.S government’s forecast for crude output next year which raised hopes that a supply glut is easing.

Note: API data yesterday indicated that U.S crude inventories fell by -8.1m barrels. Official inventory data from the EIA is due at 10:30 am EDT.

Also supporting prices, the EIA said yesterday it expected U.S. crude oil production to rise by less than previously forecast next year due to a lower price outlook.

Brent crude is up +86c, at +$48.38 a barrel, while U.S light crude (WTI) has gained +93c to +$45.97.

Crude ‘bears’ believe that despite further upside could be expected in the short term amid the speculations of a cut in U.S production, theses gains may be limited by the firm oversupply dynamics of the markets.

Note: Brent prices are -17% below their 2017 opening despite a deal OPEC to cut production from January. U.S oil production has risen over +10% since mid-2016 to +9.34m bpd.

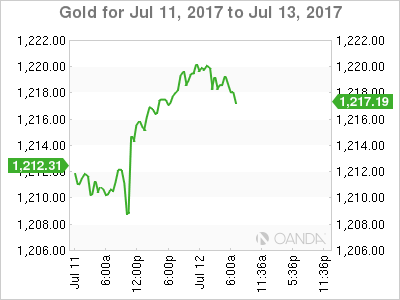

Yesterday, Gold registered its biggest intraday percentage gain since June 23 and silver registered its biggest intraday percentage rise in over a month. Currently, the yellow metal is little changed at +$1,217.97 an ounce and silver is +0.4% higher at +$15.80.

3. Yields curves look for further guidance

Fed Chair Janet Yellen is likely to reinforce the message of her June meeting’s press conference, guiding the market toward an announcement of balance sheet normalization and a rate-rise by end-2017.

Comments from Fed’s Mester (hawkish, non-voter) overnight noted reversing QE sooner rather than later is preferable, while the Fed’s Brainard (voter) indicated it was appropriate to reduce balance sheet soon if economic data holds up and that policy makers should move cautiously on further rate increases to help boost inflation back to +2% target.

Ahead of the open, U.S 10-year note yields have dropped -1 bps to +2.36%. The yield on Aussie 10-year bonds have fallen -3 bps to +2.72%, halting five days of gains. In Japan, the BoJ again raised outright purchases of 3 and 5-year government notes to contain the recent increase in medium-term yields.

In Germany, this morning’s 10-year Bund auction (4B, 2027) posted the highest funding cost since an auction in January 2016. The average yield was +0.59% with a bid-to-cover ratio of +1.4.

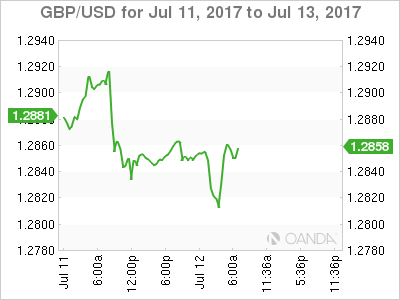

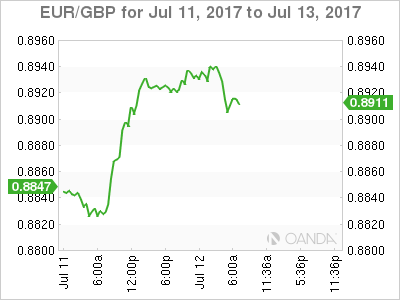

4. Sterling’s whippy price action

The pound came under pressure; printed new week lows (£1.2812), when the Bank of England Deputy Governor Ben Broadbent said he was not yet ready to vote for a rise in the key interest rate, citing the many uncertainties surrounded the outlook for the economy.

However, the it has since recouped its losses and then some (£1.2862, €0.8911) after U.K data showed that three-month wage growth came in above expectations and higher than in the previous quarter.

Average earnings ex-bonuses rose +2% in the three-months to May, more than the +1.8% expected.

The better-than-expected data is supportive for BoE ‘hawks’ that have suggested interest rates should rise this year.

5. Eurozone Industrial Output Picks Up Speed

Data this morning showed that Eurozone’s factories, mines and utilities output rose at the fastest annual pace in more than five years in May (+1.3% m/m and +4% y/y). The market was expecting a rise of +0.8% m/m, and +3.6% y/y – It’s further proof that the regions recovery has picked up Q2.

Note: The Eurozone economy grew at the fastest rate in two years during Q1, outpacing the U.S, the U.K. and Japan.