Executive Summary

- Recent Japanese data have underperformed expectations, suggesting that the economy is taking longer than anticipated to recover from the consumption tax hike and typhoon in October. Underlying measures of output suggest the economy did not weaken quite as much as it did following the prior tax hike in April 2014, but it also did not enjoy the same firming in growth leading into the tax hike as it did in the prior episode.

- At this point, Japan is fairly constrained in terms of a possible policy response. The Bank of Japan seems to have limited appetite for further stimulus at this point given its policy appears to be at or near its limits, while the Japanese government already announced a substantial package of easing measures a few weeks ago, and additional stimulus would only further undo some of the fiscal consolidation achieved by the 2019 tax hike. Accordingly, we are downgrading our Japanese GDP outlook, and now expect real GDP to decline 0.1% in full-year 2020, although we see a rebound to 1.2% growth in 2021.

There’s So Many Sinking Now

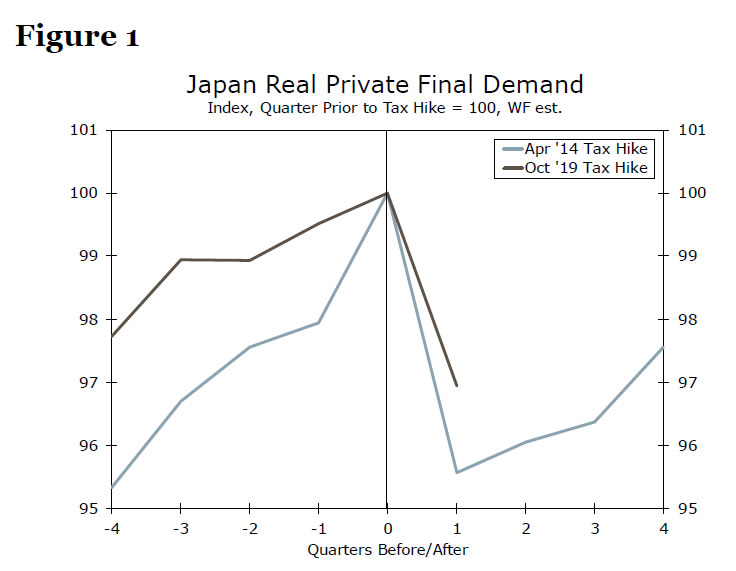

The recent economic data from Japan have been disappointing, to say the least, and suggest that the economy suffered much more than expected in the wake of a “double whammy” of a tax hike and typhoon in October. Recently released data showed that Japanese real GDP contracted at a 6.3% quarter-over-quarter annualized pace in Q4-2019, much worse than expected and the sharpest decline since the last tax hike in April 2014. Digging a little deeper, we look at real private final demand, a better underlying measure of growth that captures private sector consumption and investment adjusted for inventory changes. That measure of output fell at an even more alarming 11.7% quarter-over-quarter annualized pace, nearly double the decline in total GDP. While that decline is not as large as the drop in private final demand after the last tax hike in 2014, we also did not see the same firming of growth in the quarters leading into the 2019 tax hike (Figure 1).

We should add the important caveat that Japan was also affected by a devastating typhoon in October, which almost certainly added downward pressure to the economy in Q4. Still, December data showed another drop in overall Japanese consumption, a sign the economy may not have rebounded as much as expected toward the end of the quarter as the tax and typhoon impacts faded. Meanwhile, the initial evidence suggest Japan’s economy may face challenges again in the current quarter. Japanese exports to China represent around 3% of Japanese GDP, compared to the similar figure from the U.S. of just 0.5% of GDP, suggesting the Japanese economy could be more significantly affected by the coronavirus outbreak in China. We think Japan may just narrowly dodge recession in Q1, but the economy will probably be close to stagnating during the quarter. Accordingly, we now forecast that Japanese real GDP will decline 0.1% during full-year 2020, a significant downgrade from our prior estimate of positive growth of 0.4%. Our 2021 forecast is now for 1.2% growth, boosted by more favorable base effects from 2020.

Gonna Take a Look Around It

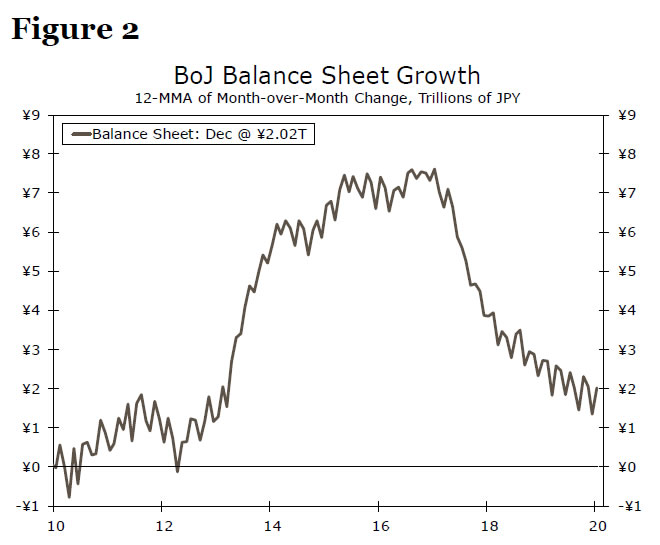

Against this more challenging economic backdrop, Japanese policymakers have been surprisingly quiet, a notable contrast to some other economies in Asia where monetary and fiscal authorities have stepped up efforts to support demand amid the virus outbreak. On the monetary side, the silence may reflect a realization from the Bank of Japan (BoJ) that its policy stimulus has perhaps reached, or is close to, a limit, and there is little appetite to add any further monetary stimulus. In fact, the BoJ has been gradually dialing back its efforts to support the Japanese economy for years now despite few signs of rising underlying inflation, purchasing ever-fewer Japanese government bonds (JGBs) and thus growing its balance sheet at an ever-slower pace (Figure 2). Accordingly, we see a limited chance of any significant BoJ policy response to recent economic weakness at this point.

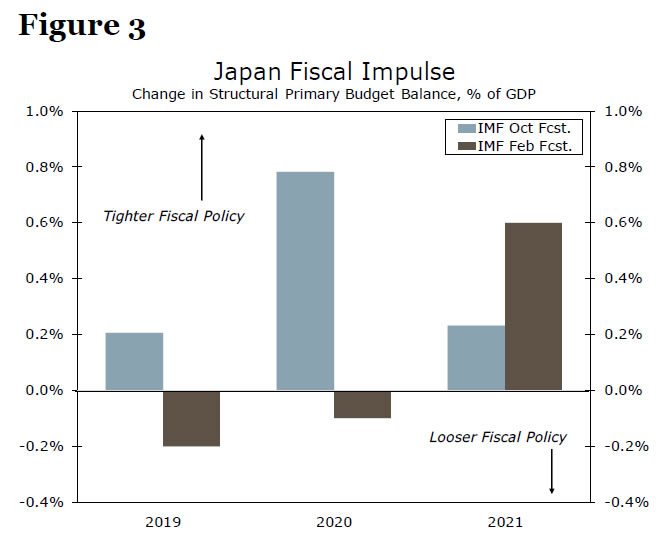

On the fiscal front, Japan already announced a comprehensive package of stimulus measures just a few weeks ago, including just under ¥10 trillion (~US$90 billion) in new government spending over the next few years. Just over one-third of that spending will come in the current fiscal year that ends in April, representing around 0.8% of annual GDP. This represents a huge fiscal swing for Japan’s government, which prior to the stimulus announcement was on course to tighten fiscal policy significantly in 2020, but is now expected to ease policy modestly (Figure 3). Given a reasonably large near-term fiscal stimulus has already been announced, the appetite for additional measures on the back of underperforming Japanese economic data is uncertain, particularly given one of the primary goals of last year’s tax hike was fiscal consolidation. That said, if there is going to be any additional policy response from Japan, it is arguably more likely to come from the fiscal side rather than the monetary side.

{kind=link}