After the production alliance between Saudi Arabia and Russia fell apart, pushing oil prices dramatically lower on concerns of a supply war at a time when the virus outbreak depresses demand, everyone is wondering what’s the floor for crude. We seem to be headed for a period where markets are flooded with supply as the major players compete for market share, which could keep prices at very low levels. Ultimately, the dust will settle and prices could recover, but that might take a while.

Pump at will

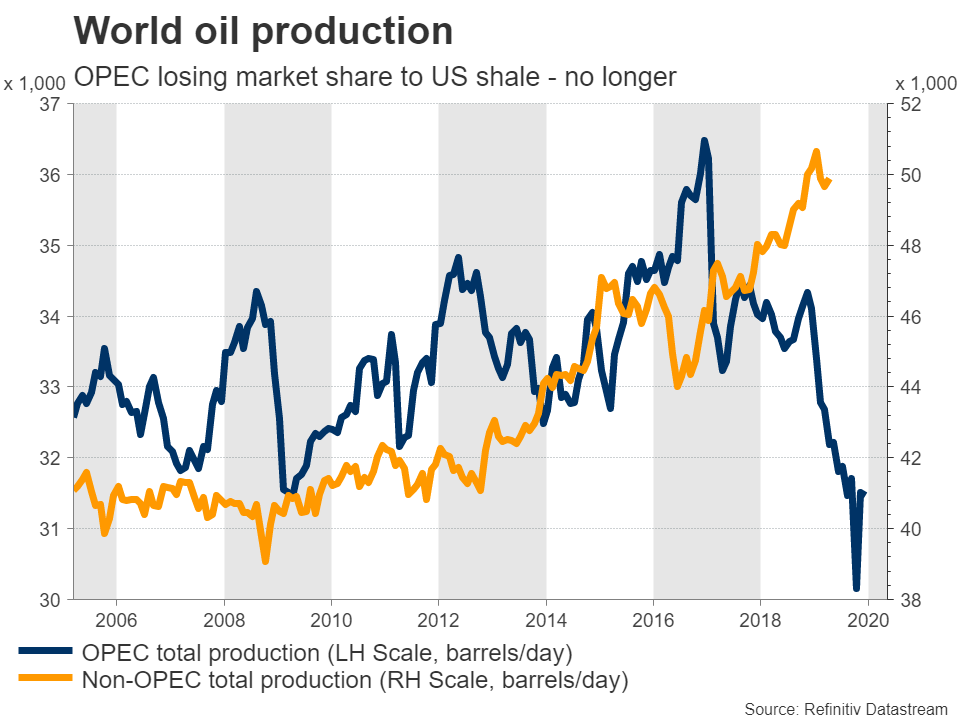

The three-year long collaboration between OPEC and Russia to manage oil prices is dead. Negotiations to cut supply collapsed over the weekend as Moscow was unwilling to reduce its own output any further to keep prices afloat, concerned that doing so would mean conceding more market share to US shale producers.

And the timing couldn’t be worse. Saudi Arabia – the de facto leader of OPEC – wanted to slash production to counter the demand shock from the virus outbreak, which has brought some of the biggest consumers of oil to their knees, most notably airlines. The latest forecasts by the International Energy Agency (IEA) suggest global oil demand is set to contract in 2020 for the first time since the financial crisis.

Russia’s refusal to ‘play ball’ sent a clear signal: this is now a supply war. At least, that’s how Saudi Arabia took it. The Kingdom immediately offered stunning discounts to its clients, aggressively undercutting its competitors, and also announced that it would ramp up its overall production by up to 3 million barrels per day (bpd) to reach new record levels, flooding the market with supply. Russia responded in kind, saying it could raise its own output by 0.5 million bpd.

Saudi vs Russia vs US shale?

All told, this will put the squeeze on US shale producers. Both Saudi and Russia think they can withstand lower oil prices much better than American firms can, considering that much of the shale industry is highly indebted and several firms might have to close down in the coming quarters if prices stay so low.

Yet, the US might not take it sitting down. The White House is reportedly considering federal assistance for the battered shale industry. That would be game changing, because the working assumption right now is that Saudi Arabia and Russia will keep pumping at record levels until some US players are squeezed out, at which point they will likely cut back their own production too and allow prices to rise again.

Therefore, if the federal US government truly intervenes to keep otherwise unprofitable producers in business, that could prolong the time it takes for US supply to decline, and by extension keep global prices lower for longer.

Pain train may not be over

With supply set to skyrocket as demand contracts, it’s almost impossible to be bullish on oil over the coming months. The only real argument is that prices may have already fallen too far too fast, and thus, a rebound may be in order.

However, that thinking may be flawed. It assumes that the situation – both from the demand and supply outlook – won’t worsen any further. Yet, each passing day reminds us that things can get worse, especially on the demand side.

The US just banned flights from Europe for a month. That could be extended further, or more realistically, other countries around the world could implement similar measures. In fact, with more and more countries going into lockdown and so many companies advising their employees to work from home, markets might even be underestimating the short-term impact on oil consumption.

On the supply side, it’s not just Saudi Arabia and Russia competing for market share. Some of OPEC’s biggest players, like Iraq and Kuwait, have already followed in Saudi Arabia’s footsteps and slashed the prices they offer to customers. And with the OPEC supply pact now over, the entire of OPEC is free to increase production to its heart’s desire, something the United Arab Emirates already signaled.

The bottom line is that if prices are in freefall amid a supply flood, each producer – no matter how big or small – has an incentive to increase their own output even further according to game theory, in an effort to reach a better outcome for themselves. Hence, it might be a matter of time before the rest of OPEC and Latin American producers join this fight.

How low can oil go?

Admittedly, that’s a tricky question, as we’ve never seen a period where global supply is surging while demand is being devastated – it’s usually one or the other.

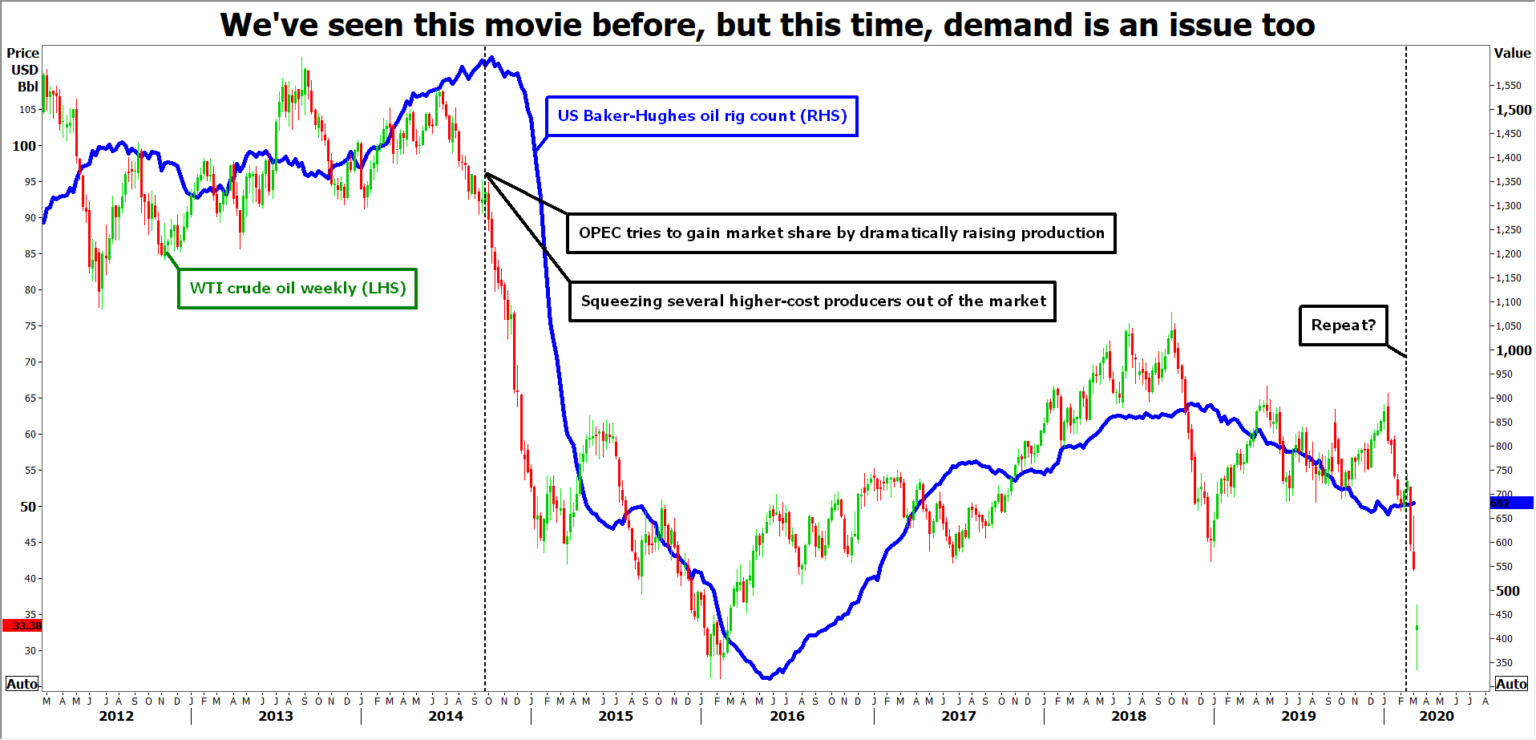

The last time we saw a supply fight was back in late 2014, when OPEC opened the floodgates and overran the market with oil to squeeze out higher-cost US producers. That ended with WTI prices reaching a low of $26/barrel in early 2016, even without demand destruction.

Hence, it’s safe to assume that prices can go even lower this time – though that might ultimately depend on how quickly the virus outbreak is brought under control and how much damage this crisis inflicts on the global economy.

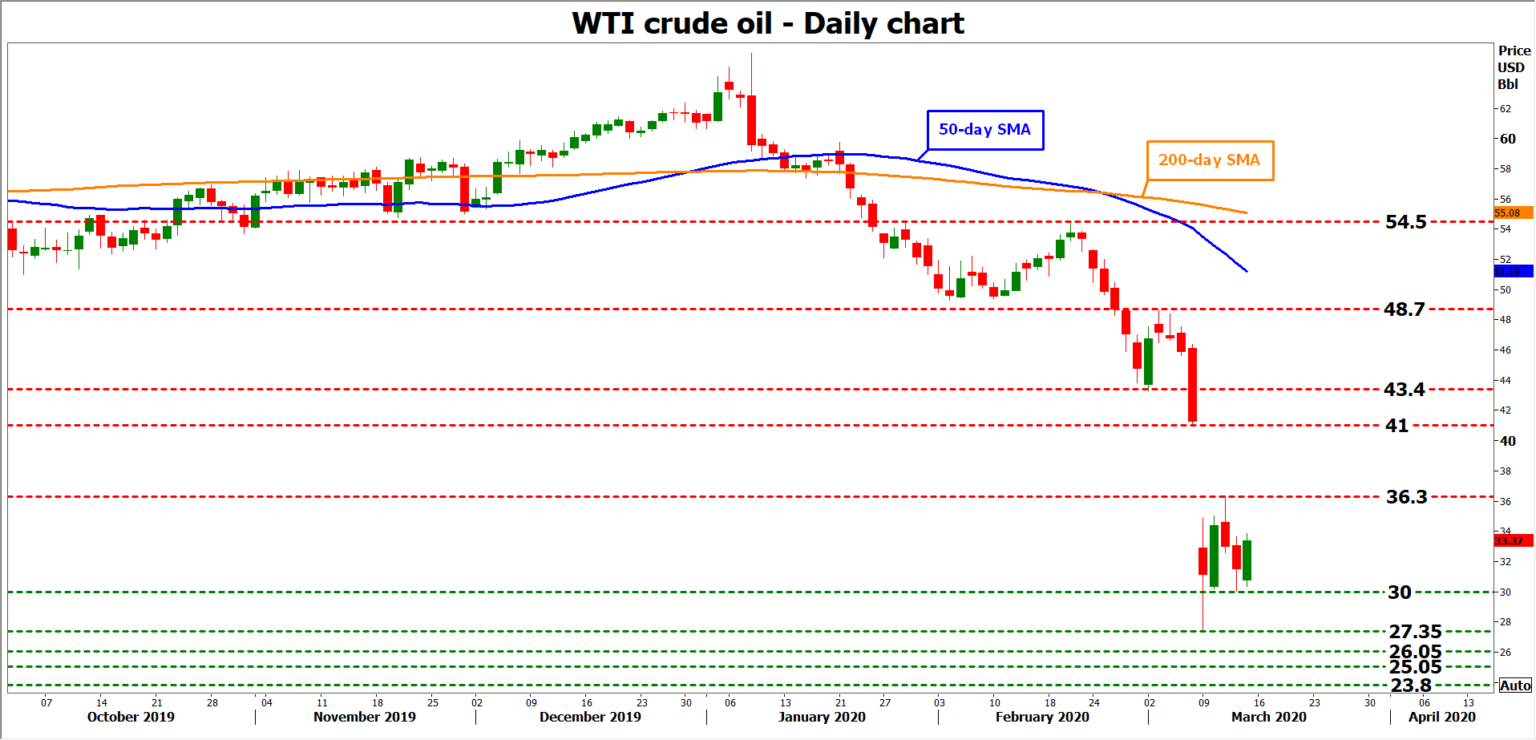

Taking a technical look at WTI, a move below the $30 handle could set the stage for another test of 27.35. A negative break could open the door for the 2016 low of 26.05, while even lower, the 2003 trough of 25.05 would attract attention.

But eventually, Russia might play ball again

Looking beyond the next few quarters though, this doesn’t seem like the ‘end’ of oil either. Prices might continue to fall only as long as Saudi and Russia are willing to endure the pain on their own economies, or until US production is curtailed.

The latter might happen sooner, meaning that once Saudi Arabia and Russia feel that enough American supply has gone offline, they will likely come back to the negotiating table to curtail their own production and lift prices again.

In short, this is an endurance contest: who can withstand lower prices for longer? The one that cries ‘uncle’ first will forfeit market share to the winners, and irrespective of who that is, prices are likely to climb again as the current situation favors nobody in the longer term.

An old market adage says “the cure for low oil prices is low oil prices” and that might be true this time as well, assuming of course that the virus situation doesn’t spiral out of control.

Looking at WTI, a recovery could stall around 36.30 initially, with an upside break turning the focus to 41.00.

{kind=link}