The coronavirus crisis prompted investors to rush for US dollars, with the greenback skyrocketing against a basket of major currencies by nearly 9% over the past ten days in the aftermath. To ease the panic and avoid currency shortages in the banking sector, the Federal Reserve decided to enhance its latest stimulus package by increasing dollar supply in overseas markets through its swap line operations. Yet, whether such an action will bring calm to nervous investors remains a question.

How do FX swap lines function?

FX swap lines are part of monetary policy and aim to increase currency liquidity. Specifically, a swap is a contract where a domestic bank borrows one currency and simultaneously lends the equivalent amount of its own to a foreign bank for a specific period and under predetermined terms, with both sides paying an overnight interbank rate such as LIBOR. At the maturity date, the two sides will buy back their domestic currency based on the same exchange rate as in the first day of the transaction, eliminating the risk stemming from volatile FX markets.

Why do we need swap agreements now?

The swap tool has been around for a long time but it played an important role during the 2008/2009 financial crisis when growing demand for the US dollars dried up dollar reserves in economies such as the Eurozone and Japan. Why did traders rush for the greenback? Because it is the most accepted currency for international transactions, making 60% of all known central bank’s foreign exchange reserves and around 40% of the world’s debt, while it is also worth noting that almost 70% of liabilities held by non-American banks during the financial crisis was denominated in US dollars. Hence, banks need dollars to keep funding international trade activities.

The current economic situation is not much different at the moment. The rapid spread of Covid-19 put the global economy on lockdown, with governments canceling flights, closing schools and shops, and restricting outside activities to contain the pandemic which is still at an early stage in the US and Europe unlike China where active cases have started to decelerate after two months.

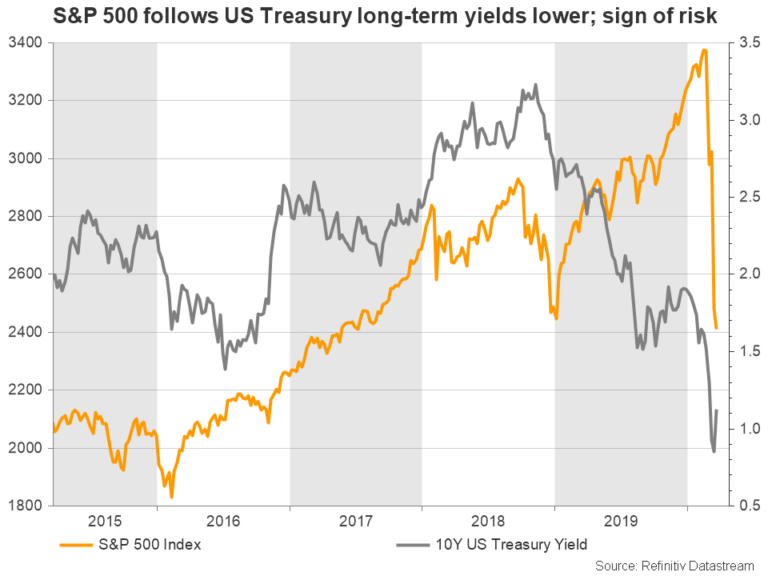

While medical trials have already started, scientists believe that it may take at least a year before a successful vaccine is available in the market. Meaning, the quarantine status may stay last some time, further squeezing business revenues and increasing demand for the US dollar, while the simultaneous fall in gold, US stocks and long-term Treasury yields reveals that traders liquidate their assets for US dollars when in fear of a recession.

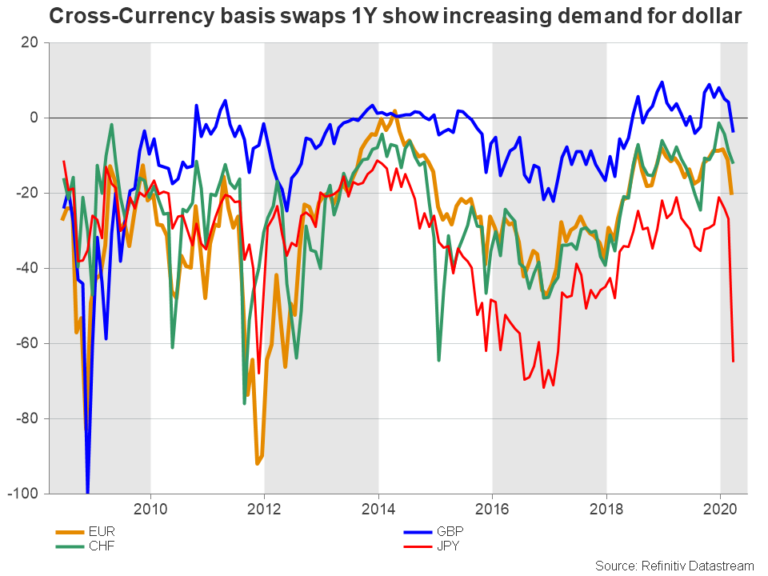

The volatility in the cross-currency basis swaps is a closely watched indicator for adjustments in dollar demand. Particularly, deviations below the zero-line indicate that the premium price to buy the dollar is rising probably due to surging demand for the currency.

In response and in consideration that the virus could disrupt the global interconnected banking sector, the Fed announced additional swap lines of a three-month duration to 14 central banks including the European Central Bank, Bank of Japan, Bank of England, and Swiss National Bank, while also relaxing the contract terms. Initially, the news narrowed the distance from the zero line. However, on Monday the cross-currency basis swaps, especially the Japanese one, resumed its negative direction suggesting that more needs to be done.

Considerations

What could go wrong with the swap currency plan? Well, the fact that important emerging countries such as China and India and other G20 members have no swap line arrangements with the US at this stressful period for the global economy is an important thing to consider. The countries have a large amount of dollar reserves in US assets such as Treasuries, which they could liquidize to meet dollar demand, pushing US interest rates and prices higher, while also disturbing the Fed’s QE effect.

The stricter requirements big banks are setting for funding, and credit quality checks to limit risks also increase the case that swap lines may not flow to the ones in need. Maybe some help from governments could allow more companies to access the extra dollar offering from the Fed.

Last and most important, unless the root of the problem which is the virus, is tackled, the Fed alone may not have the power to address dollar shortages abroad, in which case aid from other institutions such as the International Monetary Fund and World Bank may be needed.

Impact on the dollar

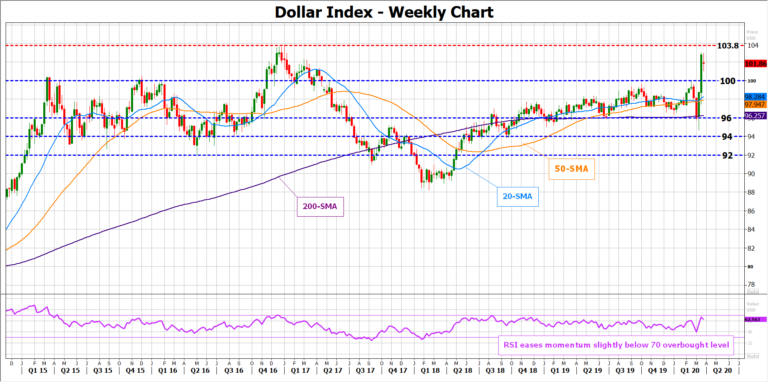

The US dollar index, which gauges the greenback’s strength against six major currencies, soared above the 100.00 level this month for the first time in three years before hitting a wall around the 2017 peak of 103.80. The Fed’s swap line announcement pushed the index a little bit lower last week, but the bulls returned soon as the virus saga continues to feed the risk-off sentiment. Traders continue to consider the dollar a safe-haven asset as the US is still relatively in better condition than other economies with a weaker GDP growth such as the Eurozone and Japan where central banks have limited or no space for extra monetary stimulus and instead seek support from fiscal policy which is a more complicated task – especially in the EU which is politically divided.

Hence unless a solution is found to the above considerations, the dollar may keep facing upside pressure as its main counterparts lose ground. Still, from a technical perspective, the pair could pause its rally in the short-term before heading up again as the market seems to be trading at the edge of the overbought territory and slightly below a strong resistance area.

A close above 103.80 could generate additional gains towards the 109.00-112.00 area. Otherwise, should the coronavirus outbreak slow down in the EU and the US earlier than expected, the index could slip back below 100.00 to retest the 94.00-96.00 region, while steeper declines may also retest the 90.00-92.00 zone.

{kind=link}