Executive Summary

- Today’s release of the Eurozone manufacturing and services PMIs in our view provides the clearest indication yet of the economic damage the Eurozone economy could suffer from the COVID-19 virus. The March services PMI slumped to a record low, while the manufacturing PMI also fell sharply.

- While the prospective economic downturn looks to be quite broad-based, the declines in service sector output are likely to be particularly noteworthy. Should the PMI surveys stay around current levels, or fall further, a Q2 GDP decline of more than 8% quarter-over-quarter annualized, perhaps extending into a double digit decline, appears well within the realm of possible outcomes.

- Considering the dire growth outlook, we expect a bias toward further Eurozone monetary and fiscal policy easing to persist. In this environment the euro could remain subdued in the nearterm, with little in the economic and policy fundamentals to suggest meaningful gains in the EUR/USD exchange rate for the time being.

Europe’s March Confidence Surveys Highlight Economic Damage

Today’s data calendar saw the release of the Eurozone manufacturing and service sector PMIs for March, which we view as the most critical European data so far in terms of trying to glean insights about the economic damage from the COVID-19 virus. Until now, Eurozone economic figures have essentially been “pre-virus” data—for example, the PMI surveys held up quite well through February, while activity data (e.g. retail sales and industrial output) are available only through January.

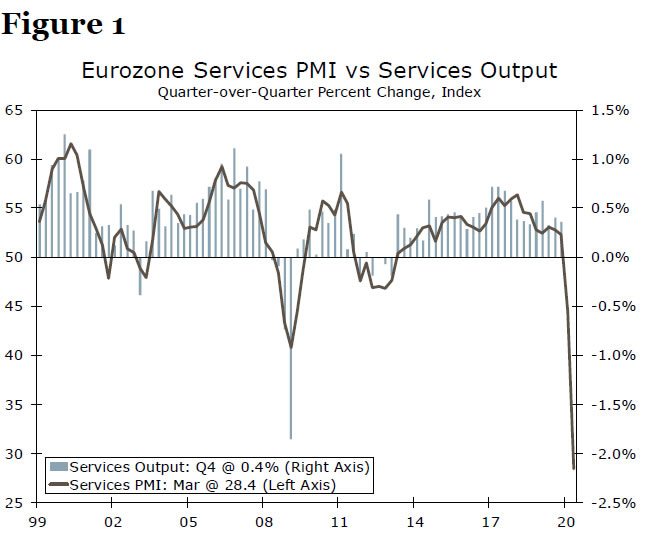

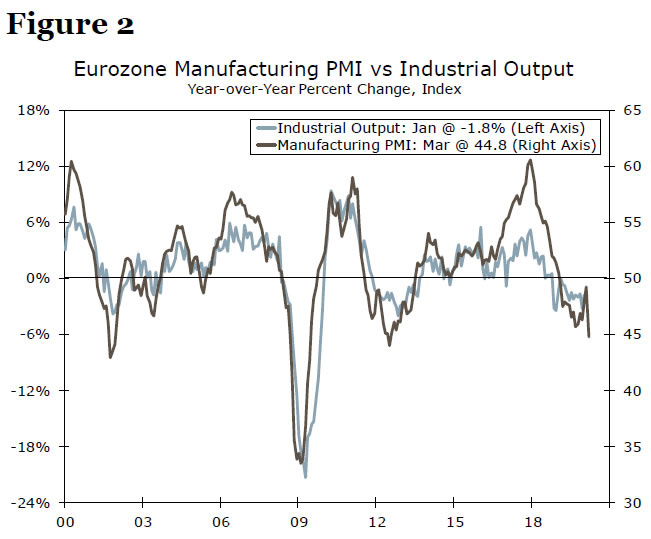

The Eurozone March PMI surveys confirmed that the economic damage from the COVID-19 crisis will be very severe. The March services PMI fell to a record low of 28.4 from 52.6 in February, even weaker than the consensus forecast which was for a reading of 39.5. Meanwhile the manufacturing PMI also fell noticeably to 44.8 in March, from 49.2 in February. Other than representing dramatic declines, what could these results tell us about the potential for Eurozone GDP growth in Q1 and Q2? In this article we use the PMI surveys to estimate to potential order of magnitude of Eurozone GDP declines during the first half of this year. To be clear these do not represent precise forecasts, but rather a “ballpark” for where Eurozone GDP outcomes may end up.

The first step in developing our estimate is to understand the significance of various Eurozone economic sectors. For 2019, services output accounted for 73.5% of GDP, while industrial output accounted for 20% of GDP. The other sectors of the economy were much smaller, with construction output around 5% of GDP and agricultural output 1.5% of GDP. The takeaway is that if one is able to calculate reasonable estimates of the services and industrial sector, one has a reasonable estimate of the overall GDP outlook.

Services Output: Slides in Q1, Slumps in Q2

Given its dominance within the economy, we first assess the outlook for the service sector. Here, we note the Eurozone services PMI has a close correlation with quarter-over-quarter services growth across the economy. Using a statistical regression since 1999, we note a solid R-squared or degree of explanatory power of 65%. Figure 1 uses that statistical regression to “line up” the services PMI with services output growth.

Given the March services PMI, the Q1 average of 44.5 mechanically lines up with a services output decline of -0.4% quarter-over-quarter, or a fall of 1.6% quarter-over-quarter annualized. In effect, the full impact of the COVID-19 virus is not seen in Q1 as arguably January and February activity were largely unaffected. An even more interesting exercise however is to presume the service PMI remains near its reading of 28.4 through much of Q2. If so, mechanically that lines up with a services output decline of 1.85% quarter-over-quarter, or 7.2% quarter-over-quarter annualized. It is still possible, however, that the services PMI could fall further during Q2. Moreover, actual services output could overshoot to the downside (as for example happened in Q1-2009). Overall, there is every reason to expect Q2 services output could fall by as much as 8% quarter-overquarter annualized or more.

Industrial Output: Extending an Existing Negative

The decline in the March manufacturing PMI to 44.8 is perhaps not quite as dramatic in terms of its implications for the industrial sector outlook. Once again we line up the manufacturing PMI with industrial output, going back to 1999. Using realistic assumptions for February industrial output and the manufacturing PMI as a guide for March, we view the decline in the PMI as consistent with perhaps a 5.5% month-over-month slump in Eurozone March industrial output. Again using regression analysis, and presuming the manufacturing PMI remains close to current levels during Q2, mechanically the March PMI output is consistent with a Q1 industrial output decline of 0.2% quarter-over-quarter, but a more marked Q2 industrial output decline of 3% quarter-over-quarter.

That said, we suspect the risks to these estimates are tilted to the downside. Over the weekend the Italian government said Italy’s industrial sector will be completely shut down for the next two weeks, something which is likely not well captured by these initial March PMI figures. We see potential for the manufacturing PMI to fall further, and industrial output to weaken further, during Q2.

Putting it Together: It Doesn’t Look Good

To recap, the March PMI surveys are likely consistent with a moderate decline in services output in Q1 and a much larger decline in Q2. For the industrial sector, we view the figures as consistent with a small decline in output in Q1 and a larger decline in output in Q2. Making reasonable assumptions about construction output and combining all the sectors together, these PMI figures could be a prelude to a Q1 GDP decline of 1.6% quarter-over-quarter annualized, and a Q2 GDP decline of 8.4% quarter-over-quarter annualized. Allowing for the possibility of overshoot there is a distinct possibility the Eurozone economy could record a double-digit decline in Q2, with the contraction in output during the current episode likely to be of a similar order of magnitude to the falls seen during the global financial crisis.

Fiscal Policymakers Stepping Up

Given the dire near-term outlook for the Eurozone, governments across the region have finally started to step up with fiscal stimulus. In particular, Germany suspended its balanced budget rule and the government announced supplementary budget of €156 billion for additional social spending and company aid, or around 4.5% of GDP. In addition, Germany has agreed to set up a fund of €600 billion to provide loans and guarantees, as well as buying stakes in stricken businesses. Italy’s government has announced a €25 billion stimulus plan, though that appears likely to fall short of what is required for Italy’s hard hit economy. Further stimulus measures are possible and perhaps likely, with recent market discussion turning towards whether the region’s European Stability Mechanism fund could be mobilized to provide support for some of the region’s economies.

Still given the magnitude of the COVID-19 shock on the economy, we doubt that prospective fiscal policy measures (as well as past monetary policy measures) will be sufficient to prevent a large economic downturn. As we highlighted earlier in this report, the Eurozone economy could face large contractions in activity in the coming quarters. During this period, we suspect the bias will remain tilted towards even further easing in Eurozone monetary policy and fiscal policy. From a currency perspective, the outlook suggests the euro should remain relatively subdued in the near-term. Given the economic outlook and policy outlook, we see little reason to expect meaningful gains in the EUR/USD exchange rate for the time being.

{kind=link}