Highlights

- Inflation has joined the list of variables blown off-course by COVID-19. April’s print showed another sharp monthly decline that sent yearly price growth to deflationary territory for the first time since the aftermath of the financial crisis.

- A confluence of factors, including the expectation of lingering economic and labour market slack and subdued commodity prices, will likely keep CPI inflation at a near-standstill for the rest of the year.

- That said, it is important to note that April’s headline deflation may be misleading. Among other measurement issues, there have likely been sizeable changes to consumption patterns brought on by COVID-19, meaning experienced inflation may be higher than what the headline suggests.

- Canadian inflation expectations appear well-anchored around the target range, with some modest downside bias. This, combined with an expected return to more normal levels of economic activity, suggests a return of inflation to near the 2% target by late 2021. Still, over the medium and long term, there are meaningful risks that price pressures could rebound even more forcefully in light of the pandemic-driven monetary and fiscal stimulus and potential changes to global value chains.

Like most facets of the economy, COVID-19 has had a profound impact on consumer prices. April saw another sharp leg down, with CPI inflation falling 0.7% (m/m)1, bringing year/year CPI inflation to deflationary territory (-0.2%) for the first time since 2009. Unsurprisingly, a large chunk of the decline was led by gasoline and fuel prices, but weak and/or negative price changes were seen elsewhere too. This near-term downshift in inflation was to be expected given the unprecedented negative demand shock, but the economic impacts of COVID-19 are unlikely to be temporary. After many years of inflation predictably trending sideways, the unprecedented nature of the shock generates large uncertainty around the near- and longer-term path of inflation going forward.

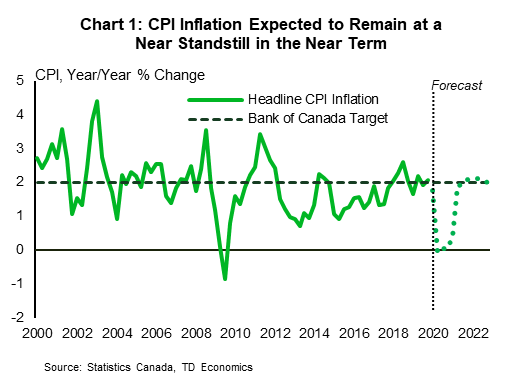

For most of 2020, we expect that persistent economic slack, an elevated unemployment rate, and lackluster commodity prices will keep headline CPI inflation (year/year) significantly below the 1% mark (Chart 1). However, the implications of such a low near-term trajectory are less clear. For one, on the monetary policy front, the Bank of Canada is fully expecting it and has already taken numerous preemptive easing actions alongside the federal government to mitigate against deflationary risks2. Second, changing consumer spending patterns mean that the reported inflation rate, which is based on fixed expenditure weights from 20173, may no longer be representative. Indeed, items experiencing a surge in demand, like food, are now facing significant upward price pressures.

Next year, we anticipate inflation to gradually move back towards the central bank’s 2% target by year-end as the economic recovery gains some traction. However, this outlook is subject to heightened uncertainty. The combination of unprecedented expansions in central bank balance sheets, massive government deficits, and the potential for changes in global value chains could fuel an even sharper upturn over the next few years. To the downside, a slower-than-projected recovery could induce further disinflationary pressures.

In The Near Term, Disinflationary Forces Remain The Key Risk

With most of the demand and commodity price hits centered in April, the most significant shock to monthly inflation is now likely in the rear-view mirror. Oil prices, for one, have rebounded, and that should help to support near-term inflation metrics. Still, most prices are likely to remain in abeyance as stores reopen and some attempt to lure cost-conscious consumers with discounts. When compared with year-ago levels, inflation will bear the marks of the current episode for some time. This is especially likely to play out in underlying (i.e., core) inflation metrics that remained resilient in May at around 1.8%. So, while headline inflation may move roughly sideways, core measures are likely to come down. This speaks more to a disinflationary environment (i.e., positive but falling growth in prices) than one of outright price declines.

Forces driving this view include:

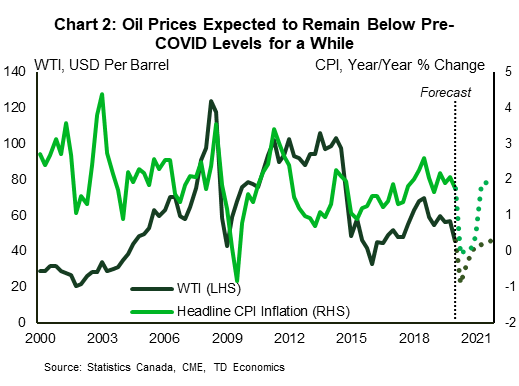

- Lackluster commodity prices: Despite the recent bounce in oil and some other commodity prices, most prices, specifically oil, are expected to remain lackluster relative to year-ago levels for the remainder of the year. Our expectation is for a gradual, subdued recovery in oil prices (Chart 2) following the unprecedented shock seen through March and April.

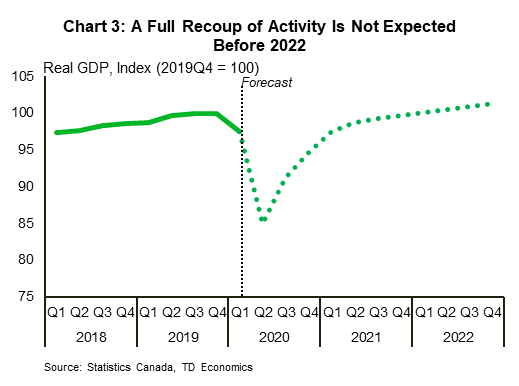

- Sizeable output gap: An output gap is an unobservable variable that represents the difference between actual GDP and potential GDP (the level of economic output that can be produced when the economy is operating at trend capacity). COVID-19 has dealt a major blow to aggregate demand and the level of economic activity. And while potential output itself has fallen (given the impacts of COVID-19 on labour and productivity), actual output has fallen by much more. When a sizeable negative output gap persists, the underlying weaknesses in demand create downward pressures on price growth. Even as economies reopen, a full recoup of lost activity (Chart 3) to levels consistent with potential output will take time. This delay is expected to be exacerbated by consumers turning more cautious with respect to their spending habits. In a recent report exploring the impact of COVID-19 on household finances, we noted that COVID-19 is anticipated to drive an increase in household savings rate. Uncertainty relating to income and employment, and the sizeable hit to household wealth mean that consumers are likely to remain cautious. This will show up not only in reduced demand for discretionary items in the consumer basket, such as clothing, restaurants, and recreation, but also in greater price sensitivity more generally.

- Labour market slack: On a related note, COVID-19’s impacts on the economy were perhaps most prominently seen in labour markets, where the Canadian economy shed upwards of 3 million jobs since February, sending the unemployment rate soaring to 13%. Labour markets impact inflation through the wage channel. The April LFS report came with a reported 11% spike in average hourly wages. However, this spike is misleading given that a substantial portion of job losses was concentrated in lower-wage industries such as accommodation and food services. Holding February’s sectoral shares constant, wage growth would still be high, although less drastic. However, this is unlikely to last. Looking ahead, the expected hit to corporate incomes and lingering unemployment will put a lid on labour demand growth and wage growth.

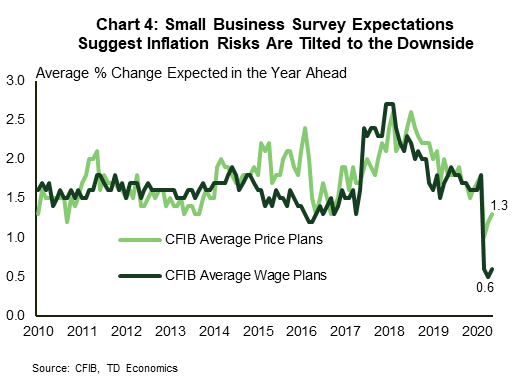

- Well-anchored inflation expectations (at a lower level): Employers’ and households’ expectations of future price growth can be self-reinforcing, impacting prices through wage contracts, benefits indexing, and future pricing plans. Canada’s inflation-targeting regime since 1991 has been successful in keeping inflationary expectations within the 1-3% target range, and this appears to mostly remain in place despite the COVID-19 shock. Useful gauges of inflation expectations show persistently weak price growth expectations in both the short and long run. For instance, surveys by forecast surveys such as Consensus Economics’ show a 0.6% consensus inflation forecast for Canada in 2020 and 1.8% in 2021. Meanwhile, responses to the CFIB’s small business barometer show average price growth plans of 1.3% and wage growth plans of 0.6% for the year ahead (Chart 4)4. Market-based measures also confirm the narrative that inflation expectations are anchored to the downside. Indeed, bond yields remain near historical lows across the curve for Canada and most advanced economies.

- Less-than-anticipated CAD depreciation: Despite the overall disinflationary environment, there are some offsetting forces. These include potential price hikes by stores as some implement surcharges to cover COVID-10 related costs and the unprecedented demand loss. Also, items in high demand, such as food and cleaning products, will exert their own upward pressure. One key immediate offset to the prevalining disinflationary forces, however, is a lower Canadian dollar, which is still around 5 cents lower than its pre-COVID levels given the combined impacts of the oil price shock and USD flight to safety. This is an inflationary driver through the import price channel. However, the impact on the Canadian dollar this time around has been much less significant both compared to Canada’s own experience in the 2014-2016 oil price shock, and to other commodity-exporting countries this year (see our report on the Canadian dollar). This depreciation is also expected to reverse more quickly5.

Current Basket Weights May Misrepresent The True Inflationary Picture

Despite the unambiguously disinflationary environment, it is important to take a step back and note the challenges associated with measurement and the representativeness of current measures. Statistics Canada has noted that data collection was impacted (conducted remotely online) and that calculation for several items was imputed given the lack of transactions6. This suggests that potential measurement error may be higher than average. More important, however, is the fact that weights assigned to each item are held constant at 2017 consumption levels. COVID-19 has changed consumption behavior, due to both – involuntary expenditure changes amidst government-mandated business closures, and an expected drop in discretionary spending due to the uncertain labour market backdrop. Transitory and modest changes to expenditure patterns can typically be ignored, but the unique nature of the COVID-19 shock means that such changes may become permanent. It remains uncertain whether (and for how long) these impacts will linger.

A useful first step would be to look at core inflation measures that exclude fuel prices, an item that has disproportionately contributed to March’s and April’s CPI decline. As noted, the Bank of Canada’s core inflation measures7 have remained surprisingly sturdy, with the three measures averaging 1.8%. Typically, the Bank of Canada uses these measures to look-through temporary volatility in headline CPI. However, a continuation of current trends may elongate the gap between core and headline inflation measures, prompting a potential re-think of expenditure baskets.

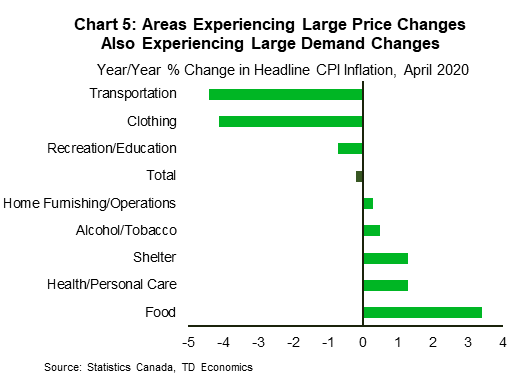

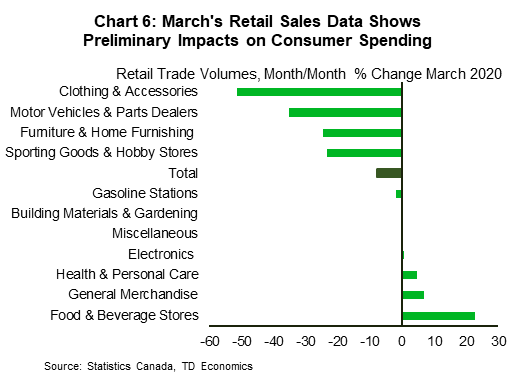

There is a lack of definitive and timely data on how consumption behaviour has responded to COVID-19, and this was one of the reasons cited by Statistics Canada for maintaining the current basket. With recent declines in prices centered across categories that are in substantially less demand due to both involuntary and discretionary reasons (Chart 5), one can confidently assert that price pressures were higher than the headline figures suggest. March’s retail sales data (Chart 6) can be useful as a gauge for preliminary impacts on consumption, but retail sales are only a small part of overall consumer spending. Our approximate “guesstimate” is that headline inflation is now likely closer to the 1% mark8.

Longer Term Inflation Mired With Uncertainty

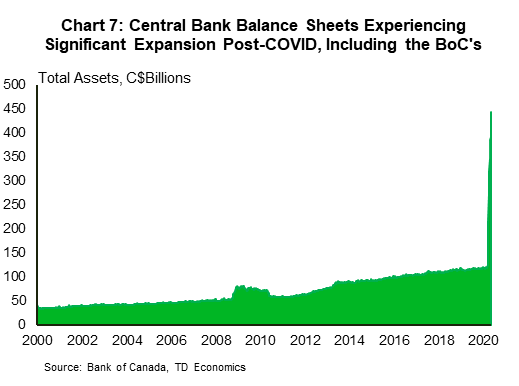

The outlook becomes more complicated in the long term, given the degree of uncertainty related to the path of the economic recovery and the timing of the output gap closure. To the downside, a slower-than-expected recovery (i.e., L-shaped) would elongate current disinflationary pressures. Meanwhile, the COVID-19 shock also adds new forces to the inflation equation in Canada and globally that were largely absent in the past few decades. These new forces tilt the risks to the upside, and include expanded central balance sheets (Chart 7) due to quantitative easing, unprecedented government stimulus and a spike in net debt/GDP ratios, and potential changes to global supply chains.

On the fiscal side, the expanded borrowing by governments is largely flowing through to “bridge” support payments to vulnerable households and individuals, and to a lesser extent, business. These are meant as a temporary backstop, akin more to filling a hole than providing an expansionary boost to demand.

On the monetary policy front, lowering the overnight rate to the effective lower bound (0.25%) was needed to prevent the more pressing near term danger of lingering deflation. For now, the impacts of the Bank of Canada’s large-scale asset purchases can largely be seen in stabilizing bond yields and credit spreads. Indeed, the aim of these purchases is exactly that – to support liquidity and prevent borrowing rates from spiking amid the uncertainrisk-off environment. Past QE experiences in the U.S., Japan, and the Eurozone have not resulted in any noticeable inflation response (although they may have had other unintended consequences that are beyond the scope of this note). However, the current scale is more significant than that seen in past episodes. Also, unwinding these policies has at times proven a difficult task9. Cross-country comparisons should also be treated with caution given each country’s unique currency and current account position.

Globally, there are also concerns around debt monetiziation as government stimulus coincides with large-scale asset purchases (see our recent report on debt monetization globally)10. On this note, the Bank of Canada has recently provided reassurances and emphasized the importance of central bank independence and its commitment to inflation-targeting. However, if debt monetization where to happen elsewhere, it could present upside risks to global inflation which could potentially be imported into Canada.

Finally, the current experience, even for countries that have implemented QE before, comes against potential supply shocks both domestically and globally. As noted in a recent Bank of Canada speech, negative hits to supply tend to drive inflation higher. This risk has increased in the past three years as deglobalization and protectionism became more prevalent. COVID-19 may accelerate this move as lockdown measures disrupt supply chains and labour mobility, and create logistical challenges. We may already be witnessing a mild version of this with the recent increases in food prices.

From a policy perspective, central banks are likely to accommodate some temporary overshoot of inflation as they focus on ensuring a smooth economic and labour market recovery from this unprecedented slump. That said, the Bank of Canada has reassured markets that they have the tools required and will act to respond to any evolving persistence in price pressures.

Bottom Line

After a decade of relative price stability and well-anchored inflation, COVID-19 came along and tore up the inflation picture both globally and in Canada. In the near term (2020), we believe that the sizeable hit to demand and commodity prices will keep inflation subdued in the 0-1% range. However, this disinflationary environment may mask some notable upward price pressures associated with changing consumer spending patterns. Inflation is expected to gradually return to its 2% anchor by late 2021, predicated on a “U-shaped” recovery. However, given the unprecedented macroeconomic environment, this outlook is subject to a range of uncertainties, including an uncertain economic recovery path, record stimulus, and potential supply-side adjustments.

End Notes

- This follows a 0.9% m/m drop in March.

- In its April MPR, the Bank of Canada noted that inflation will likely hit 0% in Q2.

- Weights were updated in 2019 based on results from the 2017 Survey of Household spending.

- Responses to the Bank of Canada’s Business Outlook Survey and its new Survey of Consumer Expectations will be key survey indicators to watch for going forward to gauge inflation expectations.

- Supply-side responses were lagged in the 2014 oil shock experience, which meant prices remained on a downward spiral for a long time until OPEC+ agreed on coordinated production cuts in late 2016. This time, the shock is creating a much larger imbalance, but the prompt supply-side (both coordinated and market-driven) response is supporting a quicker price response (although price levels are expected to remain low for a while).

- See Statistics Canada’s technical supplement here: https://www150.statcan.gc.ca/n1/pub/62f0014m/62f0014m2020006-eng.htm

- The Bank of Canada uses its three core measures (CPI Trim, CPI Common, and CPI Median) to look through temporary volatility in Headline inflation.

- This “guesstimate” is subject to a significant degree of uncertainty and the assumptions used to arrive at it are based on conclusions from retail sales data in Canada and globally, in addition to other timely data such as Google mobility trends. Another useful source that was utilized is a University of Cambridge Working Paper studying consumer behaviour in response to COVID-19 in Spain (See http://www.econ.cam.ac.uk/research-files/repec/cam/pdf/cwpe2030.pdf).

- The Taper Tantrum experience in the U.S. in 2013 is an example of this.

- This point was also addressed here: https://www.piie.com/blogs/realtime-economic-issues-watch/high-inflation-unlikely-not-impossible-advanced-economies

{kind=link}