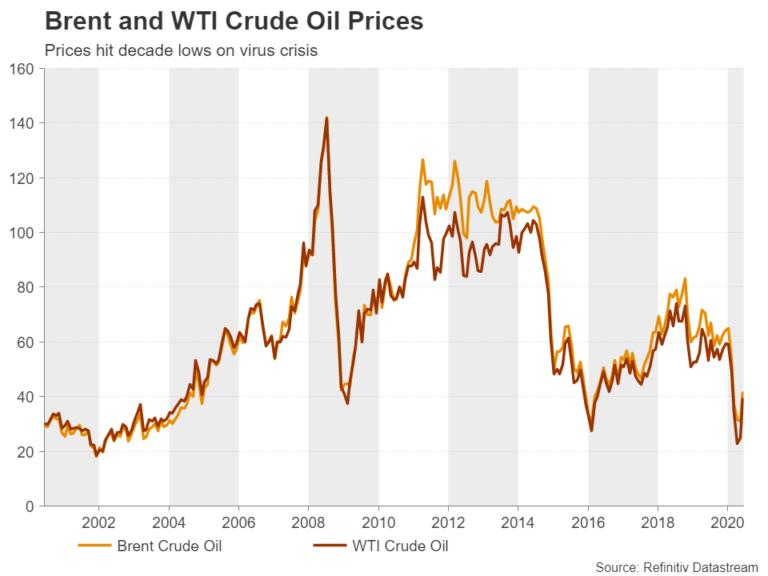

Few would argue that 2020 has been a good year for oil after the market turmoil sparked by the coronavirus crisis sent WTI prices crashing into negative territory for the first time in the US benchmark’s history. But just as the unexplainable recovery of global equities, oil is looking bullish once again, at least in the medium-term timeframe. The encouraging signs of rebounding economic activity as businesses emerge from the virus shutdowns bode well for oil and other commodities. But while stocks run the risk of being overrun by misguided optimism, the bullish bets made against oil may not be as far-fetched.

Oil started the year on the backfoot

Oil’s slide began long before the virus crisis caused a global economic shock in March as easing geopolitical tensions with Iran and some concerns about oversupply had started to weigh on prices early in the year. The sell-off accelerated in late January when it became clear that China – the world’s biggest importer of oil – was at the onset of a new virus outbreak.

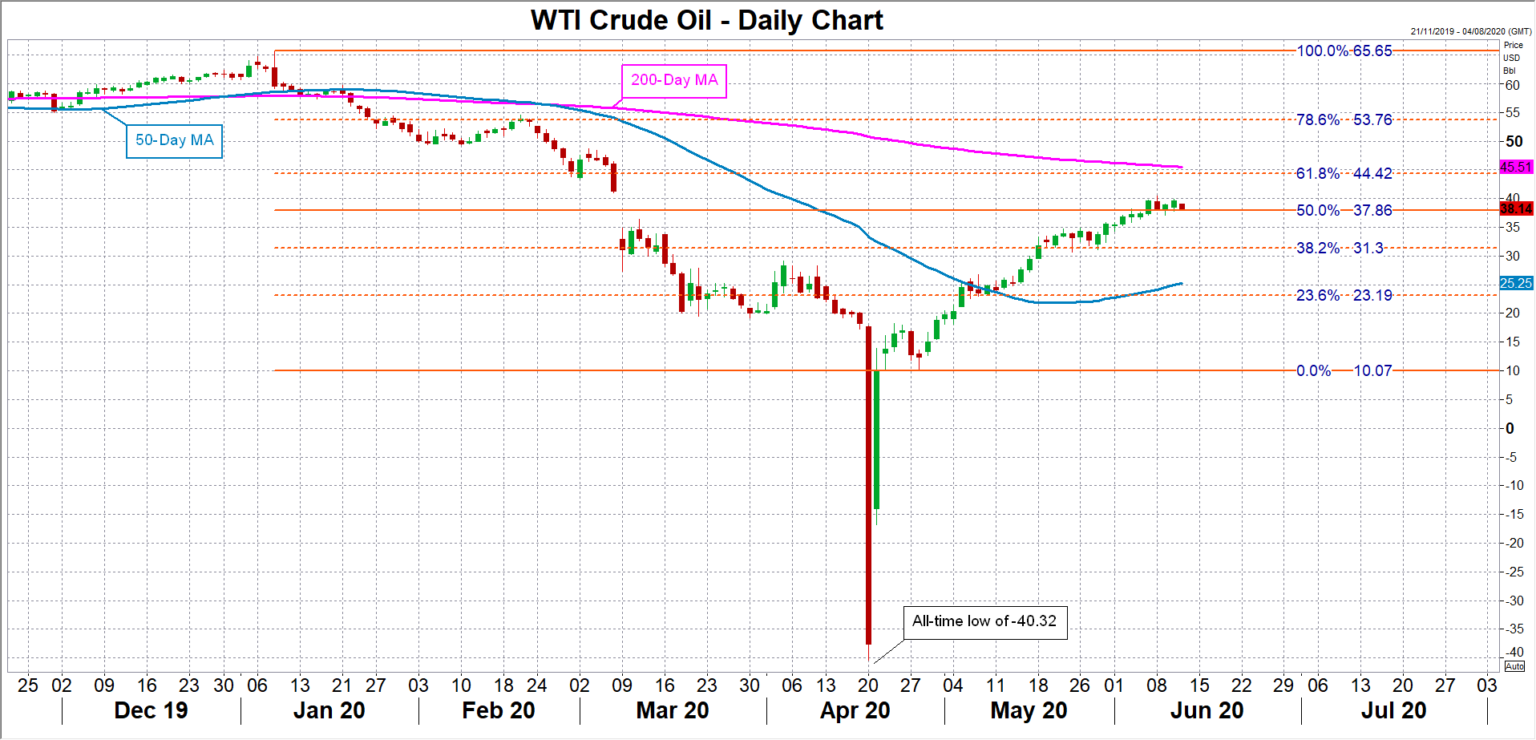

As the regional epidemic soon turned into a global pandemic, oil was in freefall. Brent crude plunged to the lowest since 1999, hitting a low of $15.98 a barrel. But it was WTI oil that suffered the highest volatility, with the price collapsing and falling into negative territory for the first time ever. That never-seen-before phenomenon was brought on when holders of May contracts were so desperate to dump their investment before the contracts expired, they were willing to pay others to take ownership. The fast sinking demand for oil had triggered an acute shortage of storage capacity in April, raising fears among traders about where to store the oil once they took delivery of it.

OPEC+ saves the day, but oil not completely out of the woods

Although the oil market has rebalanced somewhat following the steep production cuts by major producers in May, such a rare occurrence could happen again as the risks stemming from the virus fallout have not fully subsided. But the likelihood of a similar erratic movement in prices is diminishing as demand begins to recover.

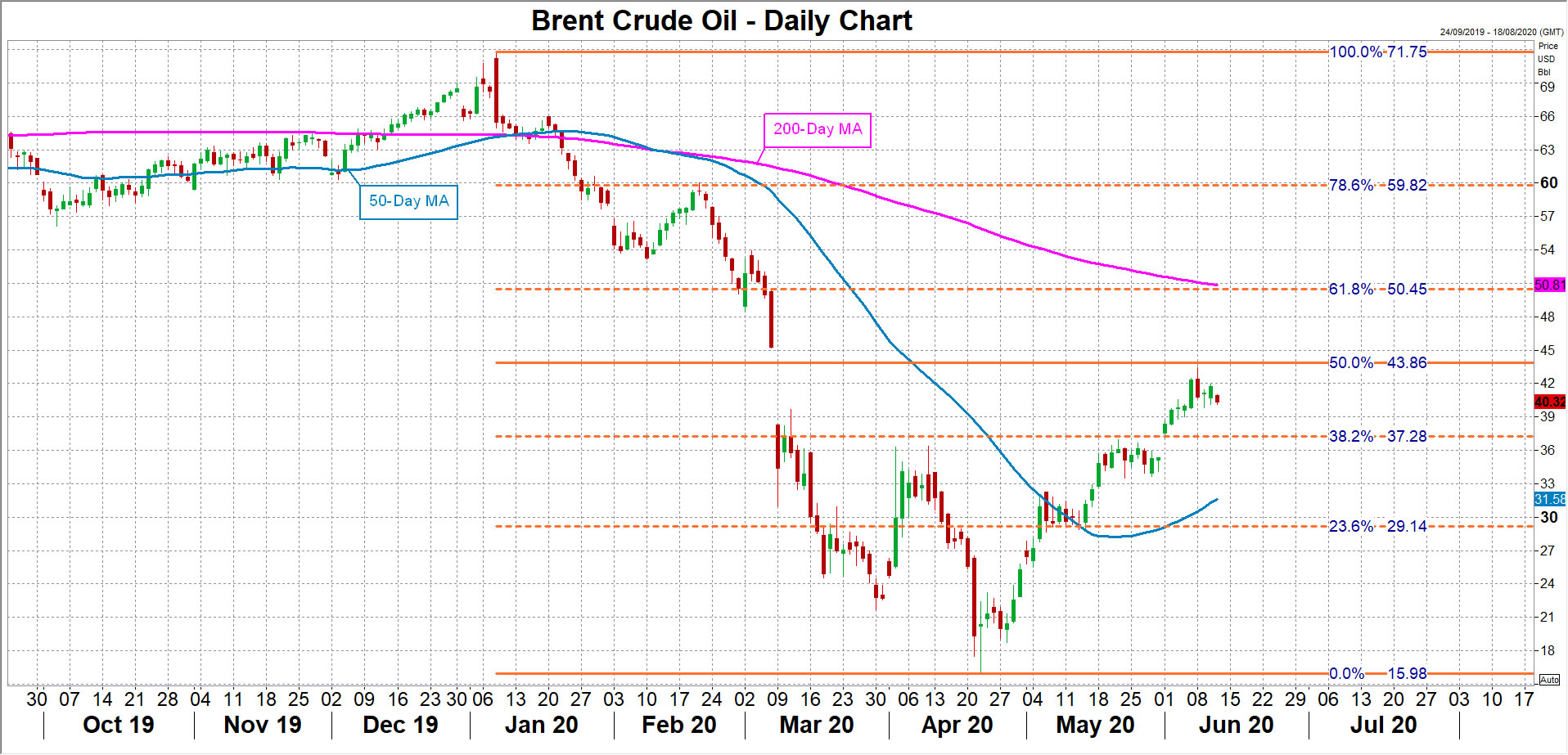

The combination of output cuts by the OPEC-led alliance and the improving economic picture as lockdown restrictions around the world are gradually lifted has spurred a more than 150% recovery in the price of Brent and an astonishing 195% jump in WTI prices from the April lows. On a technical level, both benchmarks are at critical levels. Brent has reached the 50% Fibonacci retracement of January-March downtrend and when adjusting for the negative spike, WTI is also trading around its 50% Fibonacci.

While reaching the halfway level is symbolic, both Brent and WTI need to hit the 61.8% Fibonacci, at 50.45 and 44.42 respectively, for a more convincing signal that the latest upswing is sustainable. Coincidently, the 61.8% Fibonacci marks happen to lie just below the 200-day moving averages, adding further significance to these levels.

Near-term prospects are positive

As things stand, the near-term prospects for additional gains are strong. The OPEC+ group of countries has just agreed to extend their supply cut of almost 10 million barrels per day (bpd) by one month until the end of June. There were hopes that the deal would have been extended by three months, but this may not necessarily be such a bad thing.

First, after July, there will still be hefty cuts of 8 million bpd, which will run until the end of the year. In addition, non-compliant countries will be forced to make up for their past overproduction in the coming months, meaning the actual cuts could be more than 8 million bpd after July. This, together with the rise in demand from the economic recovery that is currently underway in most major markets, should go some way in eliminating the supply glut.

US producers struggle most from the price slump

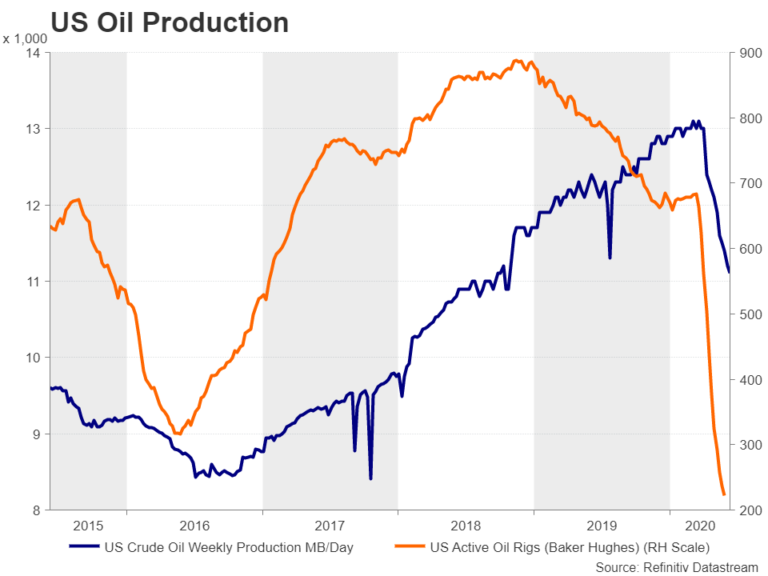

But the biggest boost to oil could come from a side effect of the price collapse, namely, the devastating impact the oil slump has had on US shale producers. The number of active oil rigs in the United States has fallen dramatically since late March as the rock bottom prices have put many shale companies, most of which are high-cost producers, out of business. Total US crude oil production has also fallen sharply since April, helping to accelerate the market rebalancing.

As more small and/or non-profitable producers go out of business in the coming months, the squeeze on supply is likely to increase, pushing up prices. Many analysts have raised their price forecasts in recent weeks, while the International Energy Agency has upped its demand outlook.

This is exactly what Russia has been hoping for – to allow prices to fall enough to hurt the US shale industry, which has been a major source of competition for Russian producers, but to contain the subsequent rally by limiting the cuts so as not to revive production from those that have left the industry.

V-shaped recovery not set in stone

But even if Russia is successful in preventing a too steep rebound in oil prices, most of the predictions are centred on the assumption that the V-shaped recovery that is taking shape will stay V-shaped, and that there won’t be a second wave of the virus outbreak. The euphoria that the worst of the virus impact is over has already infected equity traders, with many stocks on Wall Street fast approaching record territory.

In comparison, the oil rally may be better justified to the extent that there’s been a supply-side correction. But further gains without concrete evidence that the world economy is well and truly recovering from the pandemic may raise questions about the sustainability of the uptrend. Prices have currently stalled around the 50% Fibonacci and this may be the perfect spot to consolidate until the outlook becomes clearer.

Second virus wave could derail oil’s rebound

If fears of a second wave are proved to be unfounded in the coming months, which would allow the lockdown measures to be relaxed further and hence, demand continues to rebound, then the risk to oil prices would become tilted to the upside.

Unfortunately, however, the reality is that the pandemic is far from over and some countries like the United States are already seeing worrying signs of a possible flare-up in infections. If some parts of the world are forced to re-impose social distancing restrictions and plans to reopen economies are disrupted, oil could be set for another sell-off. But this time, there’s no telling how low prices would go.

{kind=link}