During the Asian day Tuesday, the RBA will announce its policy decision and the forecast is for the Bank to keep rates unchanged once again. July has been anything but boring for AUD traders. The fuss began after the minutes of the latest meeting showed a discussion regarding the level of the neutral policy rate in Australia, which was enough to raise speculation that the Bank may be preparing for a lift-off soon. However, a few days later, both Governor Lowe and Deputy Governor Debelle poured cold water on such expectations, signaling that markets shouldn’t read too much into that conversation. Lowe made it clear that the Bank is likely to stay on hold for a while.

Having said that, we think that this meeting will still be closely watched for any updated signals on policy, and in particular, whether the Bank is comfortable with the latest rise in Australian yields as well as AUD appreciation. Indeed, both Lowe and Debelle noted that a lower Aussie would be desirable, implying there is a risk that the statement communicates a greater-than-previous discomfort about the recent surge in AUD. In such a case, the Aussie could correct lower.

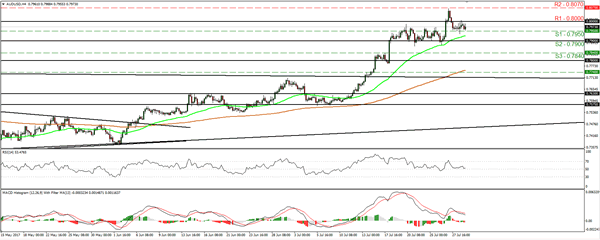

AUD/USD traded in a consolidative manner on Friday, staying between the support of 0.7950 (S1) and the round figure of 0.8000 (R1). On Thursday, the pair slid back within the sideways range between 0.7900 (S1) and 0.8000 (R1) and thus, we consider the short-term outlook to have turned back to neutral. That said, if the RBA appears more concerned than previously with regards to Aussie’s appreciation, we may see the pair sliding below 0.7950 (S1), and challenging the lower bound of the aforementioned range, at 0.7900 (S2). A clear dip below 0.7900 (S2) could set the stage for extensions towards our next support of 0.7840 (S3).

As for the bigger picture, as long as AUD/USD is trading above 0.7800, which acted as the upper bound of a wide range that had been containing the price action since the beginnings of March 2016, we still see a positive longer-term outlook. We would treat any possible retreat that stays limited above 0.7800 as a corrective phase.

Today’s highlights:

Eurozone’s preliminary CPIs for July will be in focus. The forecast is for the headline rate to have held steady, while the core rate is expected to have ticked down. We view the risks surrounding both forecasts as skewed to the upside. The July 2016 monthly CPI prints, which will be dropping out of the yearly calculation now, were -0.6% mom and -0.7% mom respectively. Therefore, even in case we get soft monthly prints today, as long as they are better than the dreadful prints of July 2016, they could still drag the yearly rates higher. What’s more, the yearly change in oil prices turned positive in July, which further supports the case for an upside surprise in the headline rate. In case of better-than-expected CPIs, the euro could come under renewed buying interest. We also get the bloc’s unemployment rate for June.

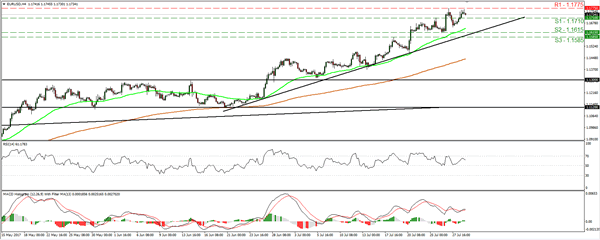

EUR/USD traded higher on Friday, broke back above 1.1710 (S1), but hit again resistance at 1.1775 (R1) before retreating somewhat. The rate continues to trade above the uptrend line drawn from the low of the 22nd of June and as a result, we consider the near-term picture to still be positive. Even if the pair retreats a bit more today, we think such a correction could encourage the bulls to take the reins again and shoot for another test at 1.1775 (R1). The catalyst for such an advance may be accelerating Eurozone CPIs today. A clear break above 1.1775 (R1) is possible to open the way for our next resistance of 1.1880.

In the US, the Chicago PMI and the Dallas Fed manufacturing activity index, both for July, are due out. We also get the nation’s pending home sales for June.

As for the rest of the week:

On Tuesday, besides the RBA decision, we get a raft of economic data from the US: the core PCE price index for June, personal income and spending data also for the same month, as well as the ISM manufacturing PMI for July. In the UK, the manufacturing PMI for July will be in focus. On Wednesday, New Zealand’s employment data for Q2 and the US ADP employment report for July are to be released. Thursday is ‘Super Thursday” in the UK, meaning that besides the BoE rate decision and the meeting minutes, we also get the quarterly Inflation Report. Finally on Friday, the US employment report for July will take center stage and expectations are for another solid report overall. We also get Canada’s employment data for the same month.

EUR/USD

Support: 1.1710 (S1), 1.1615 (S2), 1.1585 (S3)

Resistance: 1.1775 (R1), 1.1880 (R2), 1.1980 (R3)

AUD/USD

Support: 0.7950 (S1), 0.7900 (S2), 0.7840 (S3)

Resistance: 0.8000 (R1), 0.8070 (R2), 0.8160 (R3)