The Reserve Bank of New Zealand will conclude its policy meeting at 02:00 GMT Wednesday. Domestic economic data have held up better than expected, but storm clouds are gathering and the RBNZ may take proactive action. Policymakers could expand their QE programme, and lay out the conditions for using more unorthodox tools. At a minimum, the RBNZ will maintain a very dovish tone, and if it doesn’t shoot down the kiwi through more action, it may still do so through words. Itching for more

New Zealand has arguably been one of the success stories of this crisis. The nation has eradicated the virus and economic data have held up quite well. The unemployment rate even declined in Q2, though that may have been a statistical quirk. People that have been laid off aren’t counted as ‘unemployed’ if they aren’t actively looking for work, and looking for work is quite difficult during a lockdown.

The RBNZ will acknowledge that things aren’t as bad as initially feared right now, but may still take more action to support the economy. New Zealand’s borders will stay closed for a long time given the resurgence of infections across the world, which will kneecap anything directly related to tourism. Ultimately, that will hit employment, economic growth, and inflation.

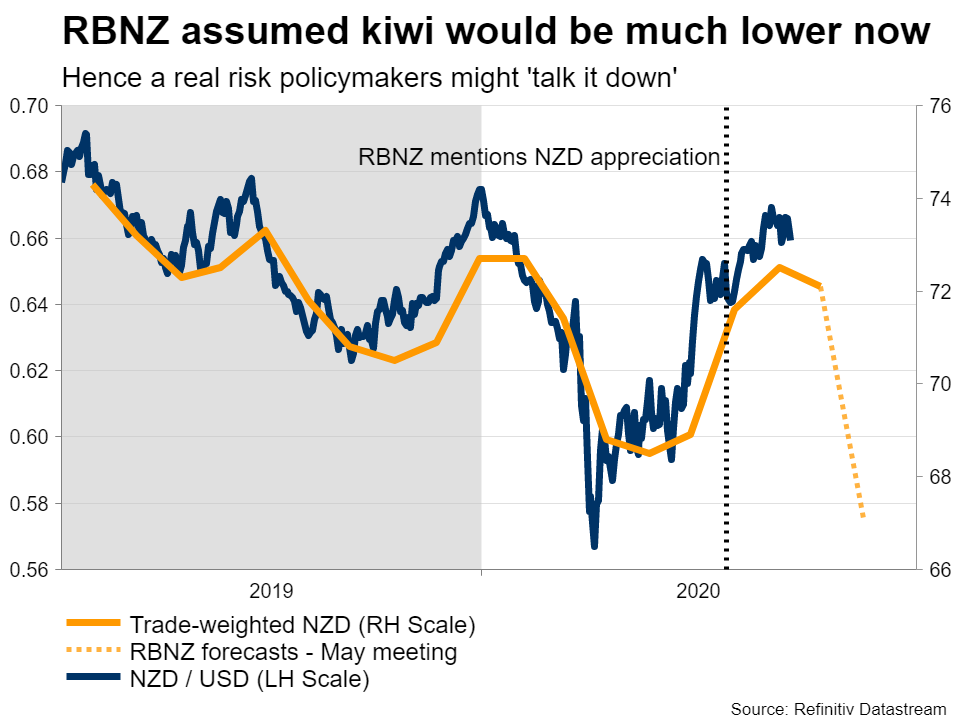

Moreover, if the global recovery stalls, that’s bad news for an export-heavy economy like New Zealand. And the recent appreciation of the kiwi won’t help. A stronger currency makes exports less competitive abroad, something the RBNZ already highlighted in June. The currency has moved even higher since then, which will make policymakers nervous.

How to shoot down a currency

In this environment, the RBNZ probably won’t wait around until the economy is hit. Monetary policy works with a lag, so if you know a shock is coming, it makes more sense to act now. The most obvious strategy is to expand the Quantitative Easing programme. Beyond that, the RBNZ has pledged to provide more detail about whether it might use more unconventional tools at this meeting. This might be the real driver for markets.

The reaction in the kiwi may depend mostly on how ‘open’ the RBNZ appears towards using negative rates. Markets are currently pricing in a 25 basis points rate cut to 0% by May 2021, and if policymakers signal negative rates are a realistic option if the economy stalls, then investors may price in even deeper cuts.

But if the RBNZ really wants to kill the currency, it has an even better alternative: opening the door for purchasing foreign assets.

Overall, the Bank will probably keep every option on the table, even if it doesn’t intend to implement it. Merely suggesting something could happen means investors will partially price it in, which has the same desired market effects – it lowers rates and limits the upside pressure on the currency, but without actually enacting that policy.

Jawboning at the least

The market seems to expect the RBNZ to expand its QE programme, but not so much the openness to foreign asset purchases, which implies a downside risk for the kiwi.

Even if the Bank doesn’t explicitly signal that it’s open to foreign asset purchases, it may still talk the kiwi down. The trade-weighted New Zealand dollar is now almost 8% higher than the RBNZ assumed in its latest forecasts, so policymakers might try to ‘jawbone’ it more forcefully, for instance by expressing concerns about its appreciation or even hinting at FX intervention as an option.

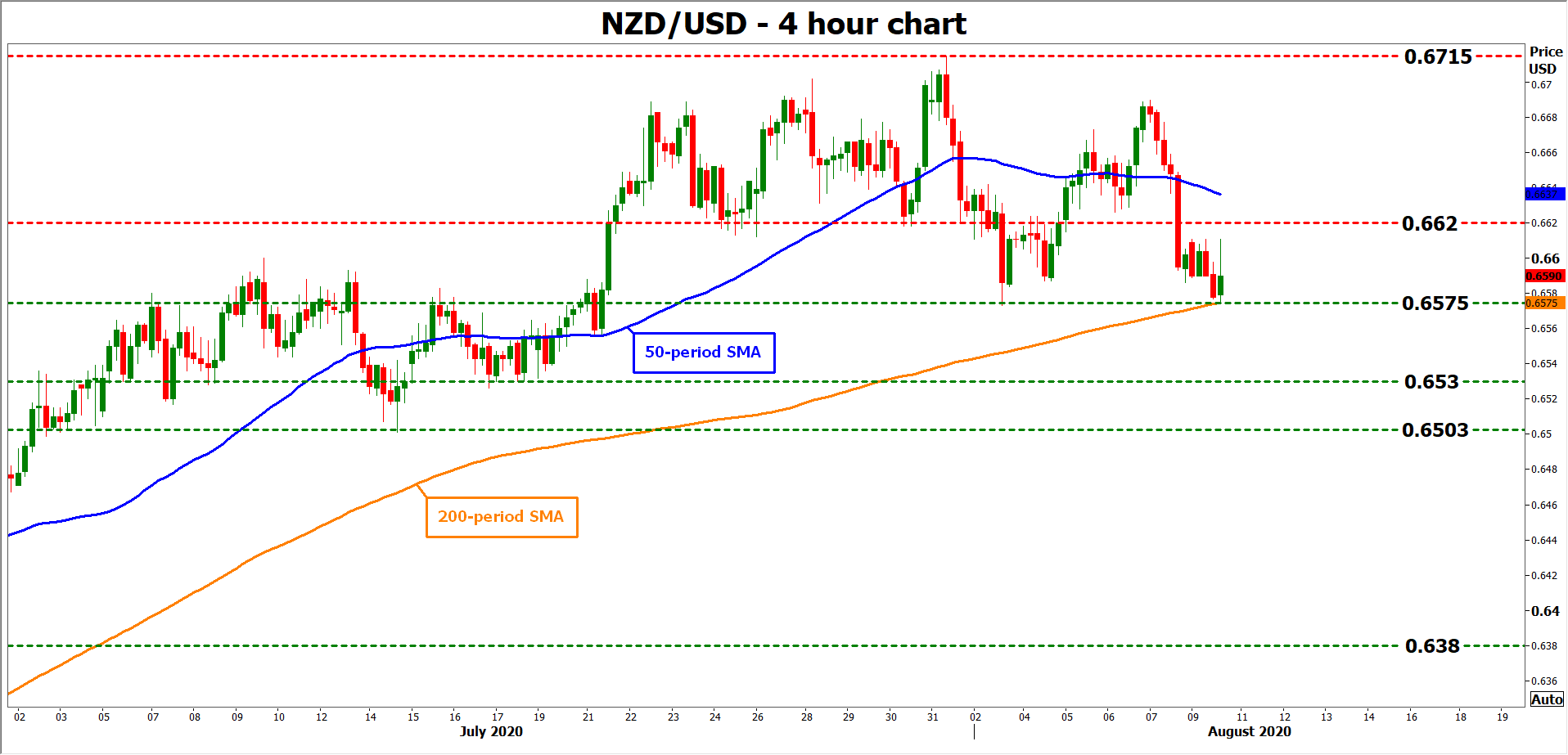

Taking a technical look at kiwi/dollar, a break below the 0.6575 zone and the 200-period simple moving average (SMA) could open the door for the 0.6530 zone.

On the flipside, if the RBNZ surprisingly closes the door to negative rates for example, the pair may shoot back above 0.6620.

{kind=link}