The British pound came under fire this week, after the UK threatened to undermine the divorce deal it has already signed with the EU and walk away from the trade negotiations altogether if no agreement is reached by mid-October. While this ultimatum is probably just a hardball negotiating tactic, it still sets the stage for a painful correction in sterling over the coming weeks as political uncertainty intensifies. Ultimately though, a last-minute deal is the most likely outcome.

Power play

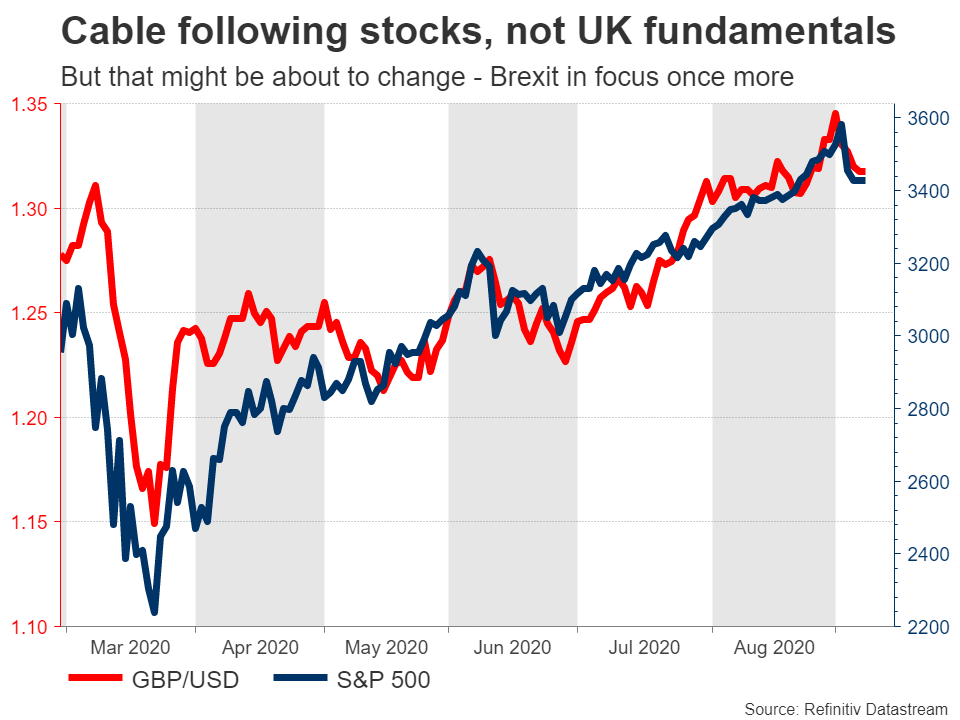

Financial markets have been ignoring the stalemate in the Brexit talks for months, with the pound instead responding mostly to changes in global risk sentiment. But all that changed this week. The UK threatened to introduce legislation that would fly against the promises it made in the divorce pact last year, while Boris Johnson declared that the middle of October is the deadline for reaching a trade deal. Otherwise, the UK will leave without one when the transition period ends on December 31.

This heavy dose of brinkmanship was apparently the straw that broke the camel’s back, with the pound moving sharply lower in the aftermath as investors priced in a higher probability of a disruptive no-deal exit.

Yet, this is not very shocking. The clock is running out and the two sides are still far apart on key issues, so Johnson is simply attempting another negotiating ‘power play’ to put pressure on the EU. And why not – the same tactic worked last year. London threatened to walk away from the talks and Brussels eventually blinked, as a no-deal scenario would be a lose-lose outcome.

Turbulence ahead

The focus now turns to this week’s negotiating round, though expectations for a breakthrough are low. The main sticking point is the so-called level playing field. The EU wants Britain to continue following some regulations on subjects like environmental protection and minimal state subsidies to businesses, to ensure that UK firms do not have an unfair advantage over their EU rivals.

That of course is anathema to Brexiteers, who argue that the whole point of Brexit was to break free from such rules. Other sources of disagreement include the enforcement mechanism of any deal, how much power the European Court of Justice should have, and fishing rights.

October is not the real deadline

To put it bluntly, these are the core issues that have been furiously discussed for years now, so it is highly unlikely that a resolution will be found within a few weeks – unless radical concessions are made. But that typically only happens when the clock is about to strike midnight and a do-or-die deadline is approaching.

Politically speaking, it is much easier to ‘sell’ any compromise to the public if the alternative is an immediate economic catastrophe, implying that we are unlikely to see any real progress until the last possible moments.

Does that mean mid-October? Maybe not. That is the deadline set out by Prime Minister Johnson because there is an EU summit on October 15-16, where European leaders would hopefully endorse any agreement. But it is not a ‘hard’ deadline by any means, as the EU could call an emergency summit at any time before the year ends in case an agreement is reached.

In fact, it is more likely that this deadline will pass without a deal. Any resolution might come later, perhaps in November, as the clock ticks down and forces leaders to water down their demands.

Does Boris Johnson even want a deal?

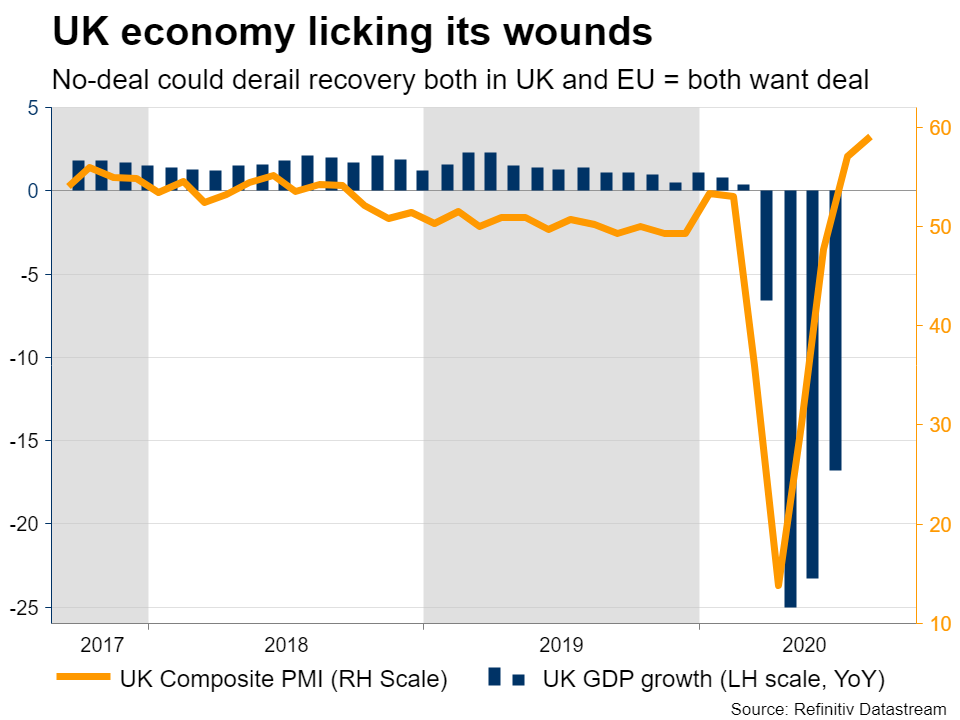

Yes he does, and do not be fooled by comments stating the opposite – they are just theatrics meant to increase his negotiating leverage. The last thing Boris wants is a disorderly Brexit come year-end that throws the economy back into the meat grinder, deepening the scars the pandemic has left.

It would be politically disastrous for him. It would strengthen the hand of the new popular opposition leader, Keir Starmer, empower the Scottish National Party in its demands for Scottish independence, and perhaps alienate some lawmakers in his own party, ultimately eroding his control over Parliament.

To be clear, all this does not go to say that a deal will get done. In the end, it may prove to be impossible and London might decide that having little EU market access is a price worth paying for retaking maximum control of its political and regulatory destiny. But it does imply that both sides want a deal.

Pound set to suffer, but perhaps not for long

All told, the coming weeks might be a difficult period for sterling. The political posturing is set to intensify and as we approach the middle of October without a deal in sight, markets could price in an even greater probability of a no-deal exit. The pound may suffer as a result, especially considering that large speculators like hedge funds are now net-long on the currency according to the latest CFTC positioning data, which leaves plenty of room for shorts to build up.

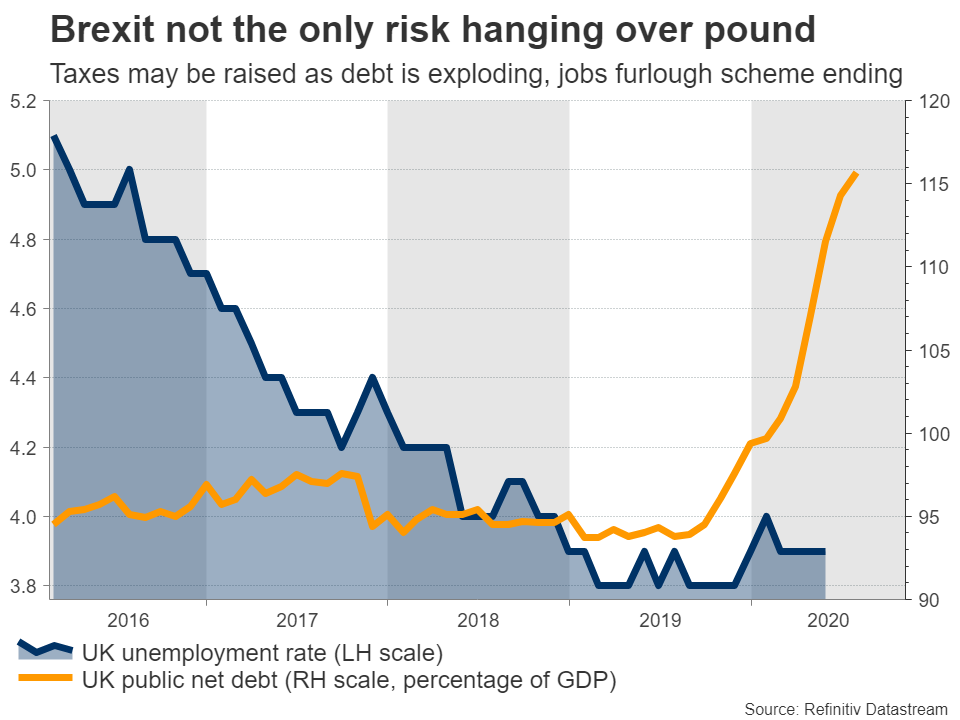

And while Brexit is important, it is not the only risk. The government’s furlough scheme is set to end in October, meaning that large swathes of people might be left unemployed when their wage subsidies vanish. Meanwhile, the explosion in government debt has the Treasury talking about raising corporate taxes to plug the hole in public finances. Both could be a disaster for the pound.

That said, an eventual deal still looks more likely than no-deal. That would imply that sterling might suffer for a while, but if some eleventh-hour agreement is finally reached in November for example, the currency could stage a powerful rebound. Hence, the logical conclusion is pain for now, but relief later.

The risk of course is that a compromise never comes. If by mid-November there is still no sense that a deal is imminent, then the pound will probably fall even more aggressively, not least because of expectations that the Bank of England will be forced to take more action to support an economy about to be hit by trade barriers.

Buckle up, it is going to be a wild ride.

{kind=link}