Another solid jobs number this Friday could all but cement expectations for the Fed to raise rates next week and send the dollar even higher. However, investors can expect the lack of clarity on Presidents Trump’s plans to grow the U.S economy through "bold" fiscal measures to cap the move.

Currently, Fed-funds futures show a +89% chance that the Fed will raise rates on March 15. A strong non-farm payroll (NFP) print this week (Fri. 08:30am) should make the Fed’s decision that tad easier. The market is anticipating that employers probably added around +190k workers to payrolls, in line with the average over the past six-months and a sign of steady job growth. A miss of substance and fixed income dealers will be hastily repricing their U.S curve, while the dollar bulls will be cutting some of their positions. Investors will get a heads up from this morning’s U.S ADP non-farm employment (08:15 EST).

ECB President is not expected to flinch at tomorrow’s ECB meeting (07:45 EST) even after headline inflation reached the banks desired +2% target last month. ECB policy makers are expected to keep QE going until the end of this year with underlying price pressures muted.

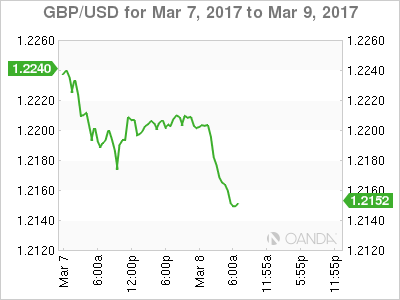

Today, the U.K’s budget arrives in a few hours (07:30 EST). Chancellor Hammond pledged on the weekend to set aside money to cushion the economy from Brexit. With the pound sitting atop of its two-month low (£1.2165), will it get a reprieve?

1. Global Stocks mixed, seek some policy clarity

For global equities, trepidation is setting in after one of the steepest post U.S election rallies in history. Investors require clarity and transparency and not Twitter policy innuendos.

In Japan, despite stronger Q4 GDP data (see below), the Nikkei eased slightly overnight (-0.5%) for the fourth consecutive session, as investors turned cautious ahead of a Friday’s NFP. The broader Topix fell -0.3%.

In Hong Kong, stocks extended their gains for a third consecutive session, helped by strength in mainland property developers. The benchmark Hang Seng index added +0.4%, while the Hong Kong China Enterprises Index gained +0.5%.

In China, stocks edged lower as small-caps pulled back amid lingering concerns over tighter liquidity. News that China unexpectedly posted a rare trade deficit (see below) last month did not have an impact. The CSI300 index fell -0.1%, while the Shanghai Composite Index was unchanged.

In Europe, equity indices are trading mixed ahead of the U.K Spring Budget. Financials are trading higher in the Eurostoxx, while energy and commodities are the laggards in the FTSE 100.

U.S stocks are expected to open little changed.

Indices: Stoxx50 +0.4% at 3,395, FTSE +0.1% at 7,344, DAX +0.4% at 12,009, CAC-40 +0.1% at 4,959, IBEX-35 +0.4% at 9,836, FTSE MIB +0.4% at 19,536, SMI -0.2% at 8,610, S&P 500 Futures flat

2. Crude prices fall on likely U.S. stocks build

Ahead of the U.S open, oil trades under pressure after industry data yesterday pointed to a potential ninth straight week of inventory builds, renewing concerns about an oversupply of oil despite output curbs by OPEC.

Brent futures are down -23c, or +0.4% at +$55.69, after settling down -0.2% Tuesday. U.S. West Texas Intermediate (WTI) crude fell -29c, or -0.6% to +$52.85 a barrel, after ending the previous session down -0.1%.

Yesterday’s API crude stocks rose by +11.6m barrels last week, more than five times market estimates. If that data is confirmed later today (10:30am) by the U.S. Department of Energy’s (EIA) it would be the ninth straight week of inventory builds. The market is looking for a +1.7m barrel inventory build.

The Saudi Oil Minister Al-Falih stated that compliance on OPEC/Non-OPEC oil cut agreement was not yet +100%, but it was "satisfactory." The Minister is looking at extension of oil cuts beyond the May period.

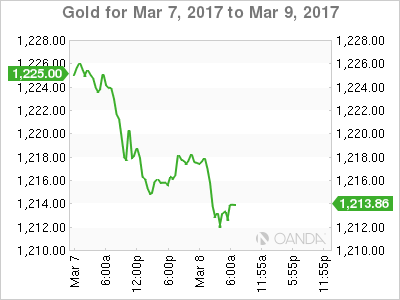

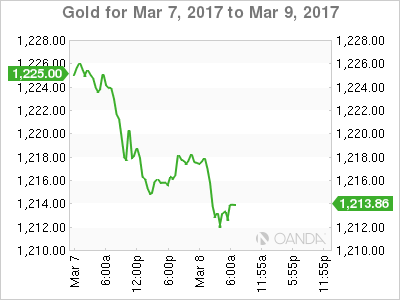

Gold’s (down -0.1% to +$1,224.86 per ounce) appeal as an alternative asset continues to suffer as political risk fades in Europe, and rising U.S yields supports the USD ahead of a Fed rate hike next week. On Friday, the metal hit +$1,222.51, the lowest since Feb. 15.

3. Treasury yield sentiment changing

After the biggest weekly selloff since November (U.S 10’s moved from +2.354% to +2.515%), sentiment on the Treasury bond market has actually turned bullish – the most bullish since October. The percentage of investors expecting lower yields rose to +20% last week from +18% a week ago (JPMorgan’s weekly Treasury client survey released Tuesday).

The share of investors expecting higher yields fell to +18% from 20%. The resulting gap of +2% reflects the most "net longs" since Oct 24.

The results would suggest some investors see the selloff as a buying opportunity and that a swift rise in yields may not in the cards. Next week’s Fed decision could change all that. However, the share of investors staying "neutral" still dominates at +62%, unchanged from a week ago.

Note: Overnight, yields on U.S 10’s backed up +1bps to +2.53%. Today at 01:00pm EST, U.S Treasury 10-year notes auction.

Note: German 5-year Bobl auction was technically ‘uncovered’ – less bids than offer volume. Average yield or -0.45%.

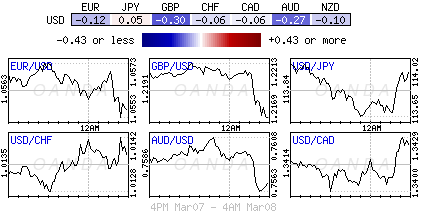

4. Big dollar consolidates across G10 pairs

USD strength remains evident, supported by higher Treasury yields, in another relatively quiet and stable overnight session. Investor focus is firmly on tomorrow’s ECB rate decision and Friday’s NFP print. Any discussions regarding a change in the ECB rate guidance is expected to gain traction in Q3 or Q4. EUR (€1.0555) ‘bulls’ should expect Eurozone politics (France and Netherlands) preventing the ECB from striking any ‘hawkish’ tone tomorrow, even as inflation data in the region improves.

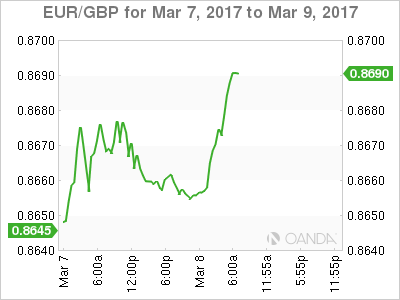

The pound (£1.2149) trades atop of its two-month low outright after the House of Lords yesterday voted to add extra conditions to the Brexit bill – it now goes back to the lower house. The market expects little impact to sterling from today’s U.K spring budget speech by Chancellor Hammond. However, bond dealers will be looking to see if Gilt issuance would be significantly reduced, as the economy has been resilient since the Brexit vote.

5. China trade in deficit, Japan Q4 final GDP revised higher

Lunar New Year distortions have China registering its first trade deficit in three years. In CNY terms, data shows that exports undershooting at +4.2% y/y vs. +14.6%e and imports surging +44.7% vs. +23.1%e.

Analysts note that some of the deviation should be attributed to the timing of Lunar New Year coming in late January this year versus early February last year and reason why China indexes discarded the headline print in the overnight session.

In Japan, Q4 final GDP improved slightly from the preliminary levels (+0.3% q/q vs. +0.4%e; y/y +1.2% vs. +1.5%e), but did miss the streets expectations. Consumption growth remained flat, though the CAPEX component was revised sharply higher to +2.0% from +0.9% prelim.