INDICES

Yesterday, European stocks remained under pressure. The Stoxx Europe 600 Index slumped 2.08%, Germany’s DAX 30 shed 2.49%, France’s CAC 40 sank 2.11%, and the U.K.’s FTSE 100 was down 1.73%.

EUROPE ADVANCE/DECLINE

92% of STOXX 600 constituents traded lower or unchanged yesterday.

53% of the shares trade above their 20D MA vs 72% Wednesday (above the 20D moving average).

58% of the shares trade above their 200D MA vs 62% Wednesday (above the 20D moving average).

The Euro Stoxx 50 Volatility index added 3.6pts to 26.84, a new 52w high.

SECTORS vs STOXX 600

3mths relative high: Industrial

3mths relative low: Insurance

Europe Best 3 sectors

real estate, travel & leisure, banks

Europe worst 3 sectors

energy, insurance, utilities

INTEREST RATE

The 10yr Bund yield fell 2bps to -0.58% (below its 20D MA). The 2yr-10yr yield spread rose 1bp to -16bps (above its 20D MA).

ECONOMIC DATA

EC 10:00: Aug Balance of Trade, exp.: E27.9B

EC 10:00: Sep Core Inflation Rate YoY final, exp.: 0.4%

EC 10:00: Sep Inflation Rate MoM final, exp.: -0.4%

EC 10:00: Sep Inflation Rate YoY final, exp.: -0.2%

MORNING TRADING

In Asian trading hours, EUR/USD remained subdued at 1.1703 and GBP/USD extended its decline to 1.2888. USD/JPY retreated to 105.26.

Spot gold slipped to $1,906 an ounce.

#UK – IRELAND#

Rio Tinto, a giant metals miner, released a 3Q production report: “Pilbara operations produced 86.4 million tonnes (Rio Tinto share 71.4 million tonnes) in the third quarter of 2020, 1% lower than the same period of 2019, and 4% higher than the previous quarter. (…) Third quarter shipments of 82.1 million tonnes (Rio Tinto share 67.6 million tonnes) were 5% lower than the third quarter of 2019 with significant planned maintenance activity affecting the port during the period.”

J D Wetherspoon, a pub company, posted full-year results: “Total sales in the financial year were £1,262.0m, a decrease of 30.6%. Like-for-like sales decreased by 29.5%, having increased by 5.9% in the first half. (…) Earnings per share, including shares held in trust by the employee share scheme, before exceptional items, were -27.6p (2019: 75.5p). (…) The board is not proposing a final dividend payment for the year.”

#FRANCE#

LVMH, a luxury goods conglomerate, announced that 3Q revenue dropped 10% on year (-7% organic growth) to 11.96 billion euros and 9-month revenue was down 21% (-21% organic growth) to 30.35 billion euros. The company said 3Q sales reflected “a marked improvement in trends compared to the first half, notably a return to growth in Cognac and Fashion & Leather Goods (+12% organic growth)”. It also added that “the decision to pay an interim dividend will be discussed”.

Eurofins Scientific, a bioanalytical testing company, announced a ten-for-one stock split, effective upon the listing on Euronext Paris of the new shares expected to occur on November 19.

Saint-Gobain, a building materials supplier, was downgraded to “neutral” from “buy” at Goldman Sachs.

#BENELUX#

Just Eat Takeaway, an online food order and delivery service provider, was upgraded to “buy” from “hold” at HSBC.

#SWITZERLAND#

Nestle, a food and drink processing conglomerate, has initiated the sale process for its 5 billion dollars North American water brands, reported Bloomberg citing people familiar with the matter.

#SWEDEN#

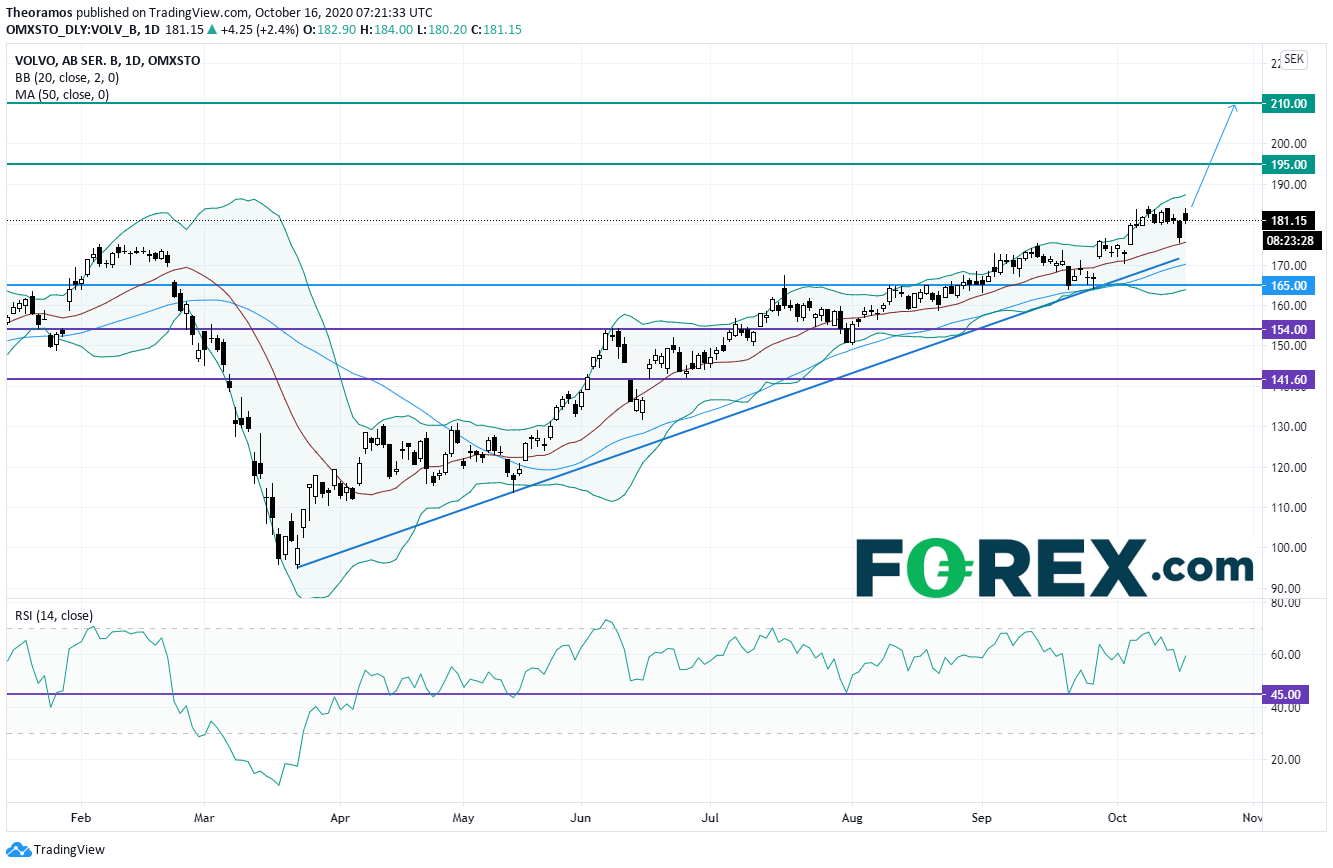

Volvo, a vehicle manufacturer, announced that 3Q net income declined 23% on year to 5.72 billion Swedish krona and adjusted operating income dropped 34% to 7.22 billion Swedish krona on net sales of 76.85 billion Swedish krona, down 22% (-16% currency adjusted). The company said: “Towards the end of the quarter transport activity was back on roughly the same level as a year ago in most markets. This led to an improved sentiment among our customers, which is reflected in increased order intake for trucks, engines and construction equipment as well as a gradually improving service business.”

From a daily point of view, the stock is trading above a rising trend line drawn since March 2020. Furthermore, the 50 DMA is playing a support role, while the Relative Strenght Index is carried by the key support at 45%. Above 165SEK, targets are set at 195SEK and 210SEK in extension.