U.S. Highlights

- U.S. equities jumped early this week and continued to move higher over the course of it despite the prospect of higher corporate taxes announced by the Biden administration.

- A few dark spots in the short-term outlook are supply chain disruptions, which are pushing up prices and weighing on deliveries in the services sector, as well as imports and exports.

Canadian Highlights

- Canada registered an above-consensus, 303K gain in employment in March. The details of the report were solid, but optimism was tempered by a third wave of infections that is prompting renewed restrictions across the country.

- Housing markets also took center stage. Regional data pointed to continued strength in activity in March. Concerns over housing market froth contributed to a new stress test rule by the Office of the Superintendent of Financial Institutions.

Global Highlights

- G20 countries met this week to discuss a myriad number of issues facing the global economy. They agreed to boost the IMF’s reserves, extend debt service payments for low-income emerging markets (EMs) and called for international tax cooperation.

- Climate change and protectionism also made a comeback. The two issues had been conspicuously absent from recent G20 meetings.

U.S. – A Few Dark Spots in Bright Economic Growth Prospects

U.S. equities jumped early this week and continued to move higher over the course of it despite the prospect of higher corporate taxes announced by the Biden administration. While still in the proposal stage, higher corporate income taxes would be a shock to earnings and equity valuations, though potentially offset by faster economic growth if invested well.

The economic calendar, meanwhile, was marked by reports on business activity, production prices and international trade. The Institute for Supply Management’s (ISM) service-sector index pleasantly surprised, hitting an all-time high. All 18 industries reported a revival of activity thanks to warmer weather and an accelerating pace of vaccinations. The rebound lifted the employment sub-index to 57.2, the best reading since June of 2019. Prospects for sustained reopening and a surge in demand could provide businesses with incentives for pre-emptive hiring, provided another wave of the virus does not lead to further restrictions.

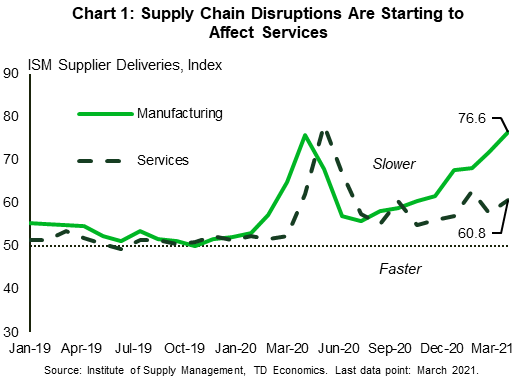

Still, several factors warrant caution. First, the uptick in the supplier deliveries index indicates supply chain disruptions are spreading beyond manufacturing sector to services. Respondents in the accommodation & food services, arts & entertainment and information industries all commented on delays (Chart 1). Logistical challenges may result in product shortages and a reduce the ability of businesses to meet rising consumer demand.

Second, the price sub-index rose to 74, the highest level in over a decade. This does not mean immediately higher consumer prices, but it does mean that businesses are facing high costs that could eventually be passed on. Corroborating this, the Producer Price Index (PPI) increased by 1.0% in March. Most of the increase was attributed to higher demand for goods, notably energy, which jumped 5.9%. The final demand index for services rose by 0.7% in March, with prices for transportation and warehousing rising by 1.5%.

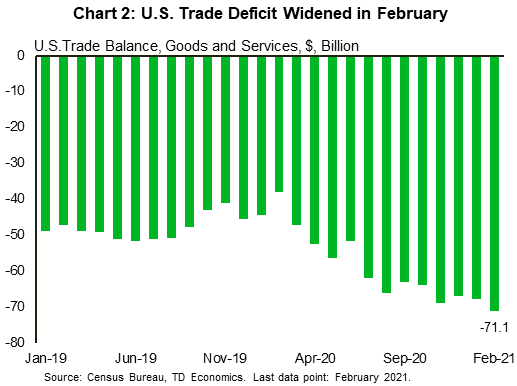

At the same time, February’s trade report is a reminder that until the whole world is over the pandemic, supply challenges and halting global demand will remain an important macro theme. The U.S. trade deficit rose to a record $71.1 billion, as exports declined more than imports (Chart 2). With major trading partners still struggling to contain the spread of the virus, demand for U.S. exports fell. At the same time, shipping congestion in ports of Los Angeles and Long Beach contributed to the decline in trade in the month. This has not yet been resolved, and alongside the disruption at the Suez Canal, will continue to show up in the economic statistics in the month ahead.

Canada – Third Wave Dampens Near-Term Optimism

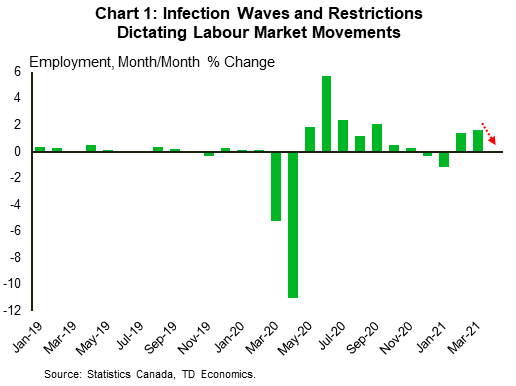

The uneven nature of the economic recovery is best captured by labour market trends, where the ebb and flow of employment data continues to move in tandem with caseloads and restrictions (Chart 1). Canada clocked in an above-consensus, 303K gain in employment in March. The strong reading was bolstered by the lifting of restrictions on some services industries across Canada’s largest provinces. Almost all details in the report were encouraging, with a decent split between full and part-time job gains, solid private sector job gains, and broad-based industry and regional strength. The labour force participation rate also edged closer to pre-pandemic levels, easing concerns over long-term scarring. While still early, the solid increase in hours worked (+2%) points to a stronger-than-expected outturn for economic growth in the first quarter, and a decent handoff to the second quarter.

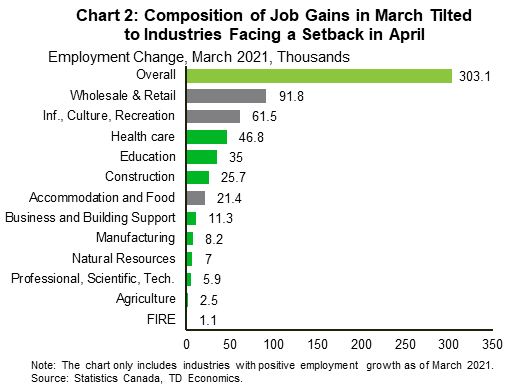

Still, optimism was dampened by a rising rate of infections and hospitalizations across the country. This has prompted a new round of restrictions in Canada’s largest provinces. Ontario, which was responsible for the bulk of the month’s job gains (+182K), has reinstated restrictions on retail, restaurants and personal services industries across the province. B.C., Alberta, and Quebec have recently enacted similar, though less stringent restrictions. Against this backdrop, the K-shaped nature of the recovery is likely to be amplified further. For instance, the recovery in some of Canada’s largest provinces (in particular, Ontario) is likely to continue to lag the Maritime and Prairie provinces. Likewise, close-contact industries are expected to face another setback in April (Chart 2). While the trajectory of caseloads and hospitalizations and the duration of restrictions remains uncertain, a pick-up in the pace of vaccinations across the country suggests that there is light at the end of the long tunnel.

Meanwhile, some sectors are expected to continue to provide some offset to lingering weaknesses in the close-contact services industries. One such area is housing, where activity continues to rise unabated. Indeed, regional real estate data released this week pointed to another expansion in activity in March in Vancouver and Calgary, with near-flat performance in Toronto.

The torrid pace of activity in the past year has led to renewed concerns on its sustainability and impact on financial stability. In that vein, the Office of the Superintendent of Financial Institutions (OSFI) announced new rules on mortgage qualification this week. The proposal would result in a 46 basis point (bp) increase over the current qualifying mortgage rate for uninsured mortgages. This increase is less significant than the 2018 B-20 rule change. The rule may result in compositional changes in demand. However, the comparatively modest increase, combined with still-tight markets, suggests that the impact of the proposal on sales and prices is likely to be less than in 2018. As interest rates continue to trend higher more broadly, we expect activity to moderate to more sustainable levels by the second half of the year, irrespective of the new rule.

Global – G20 Tackles a Host of Issues Facing the Post-Pandemic Global Economy

A meeting of central bankers and finance ministers from 19 of the world’s largest economies plus the European Union – the G20 – met virtually this week to discuss a host of issues facing the global economy.

The G20 acknowledged the improved global economic outlook due to vaccination campaigns and continued policy supports, especially in advanced economies. Still, it highlighted the uneven recovery both across and within countries. The Group vowed to fight rising inequalities caused by the pandemic. It also committed to protect those most impacted, including “women, youth, informal and low-skilled workers.”

Recognizing the unique challenges faced by low-income emerging markets (EMs), the G20 extended it Debt Service Suspension Initiative (DSSI) until end-2021. The DSSI, which was due to end in June, was launched last May to offer temporary debt relief to low-income EMs reeling from the impact of the pandemic. So far, 46 countries have requested debt relief worth $12.5 billion. The new extension would cover an estimated $9.9 billion in bilateral debt payments. The extension provides much needed relief to EMs, but more is needed to fill the funding gaps of some of the poorest countries.

This is where the IMF comes in. In an official communiqué released after the meeting, the G20 called on the IMF to increase its special drawing rights (SDRs). SDRs are a type of reserve asset that can be sold for cash. This is not the first time the proposal to increase SDRs has been made. Last year, the U.S. vetoed the proposal. This year, the proposal has U.S. backing. Following the G20 meeting, the IMF’s Managing Director said that the new SDR allocation of $650 billion is likely to be approved by August.

Meanwhile, climate change made a roaring comeback on the agenda. G20 leaders took a forceful stand saying that climate change and environmental protection are “increasingly urgent.” The G20 called on countries to “develop forward-looking strategies investing in innovative technologies and promoting just transitions toward more sustainable economies.” Climate change took a backseat during the Trump era but is likely to retake center-stage in future post-pandemic meetings.

Discussions surrounding protectionism also made a comeback. These discussions had been dropped by the G20 since 2017 (also at the behest of the Trump administration). The Group also talked about reforming the WTO. These are welcome developments, especially at a time when the pandemic has accelerated protectionism, increased deglobalization pressures and made countries more inward-looking.

On a related note, the G20 also called for cooperation for a “globally fair, sustainable and modern international tax system.” The Italian Finance Minister said that an agreement on international corporate taxes is likely by July. Talks are likely to take place within the broad framework laid out by the Biden administration this week. The American proposal calls for the world’s biggest corporations to pay taxes to national governments based on their sales in each country as part of a deal on a global minimum tax. European countries have backed Biden’s proposal. But they have also made it clear that it needs to be accompanied by a deal to allow Europe to tax the global profits of American tech giants. If the U.S. acquiesces to Europe’s demands, European countries would be able to raise corporate taxes from American tech companies and other large multinationals. In return, a global minimum corporate tax would allow the U.S. to raise additional revenue from U.S.-based European companies and other multinationals.

{kind=link}