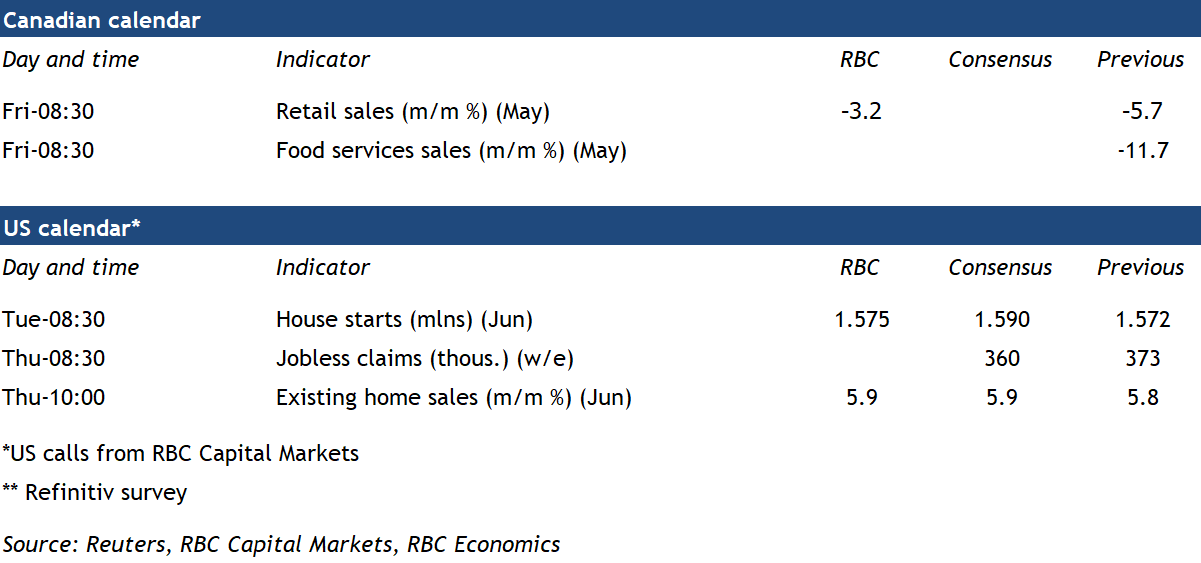

The big story next week will be the preliminary read on June retail sales after softer readings in April and May. Our own consumer tracker points to a sizable rebound in June sales, up 5-6% month over month after a decline in May similar to the 3.2% advance Statistics Canada estimate. The rebound in June came as provincial economies started to reopen – with particular gains for store types that were hit hard by lockdowns, such as clothing and footwear.

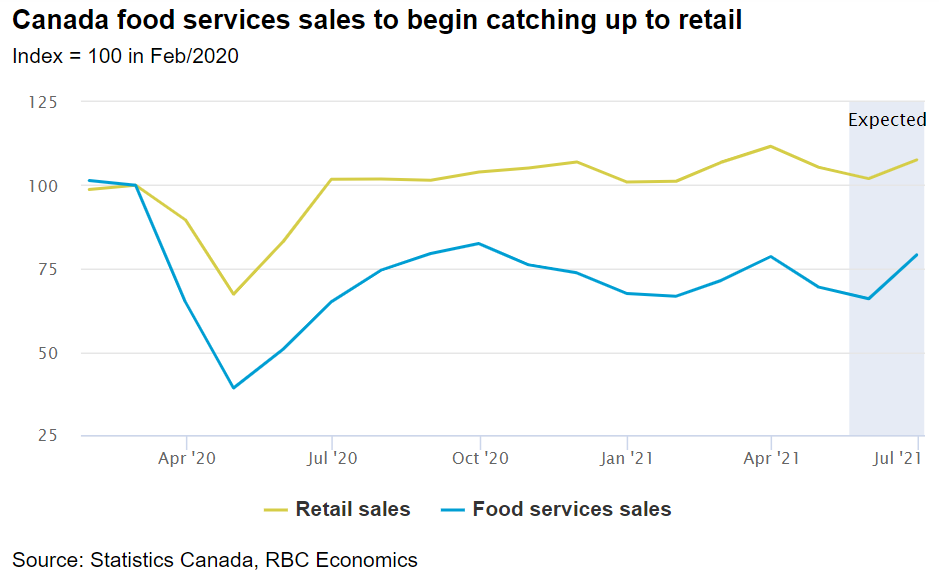

In fact, retail spending on goods outside of items like clothing has actually been quite strong. Even sizeable declines in April and May do not appear large enough to have pushed sales below pre-pandemic levels. In part, that’s because contactless shopping for goods has been made easier by expanded e-commerce infrastructure. Meantime, household purchasing power has been propped up by government support payments all while many services—which aren’t counted in the monthly retail sales data—have simply been unavailable for consumption. But as pandemic restrictions are gradually lifted, there are signs that a long-awaited rotation in household spending back to ‘high-contact’ services is finally beginning. Data on food services spending for May (to be released next week) will still be weak, but we expect a significant strengthening in June and the months to follow, as travel and hospitality services become the primary fuel for consumer spending growth.

Week ahead data watch:

- Vaccine distribution continues to progress, with close to 80% of the eligible (age 12+) population in Canada having received at least one dose and more than half now fully vaccinated with two doses. Provinces continue to ease restrictions, with Ontario entering Step 3 of the reopening process on July 16.

- US existing home sales are expected to hold close to May levels in June—still high by historical comparison but a decline from exceptionally strong levels earlier in the spring.

Next week’s flash PMI releases will offer an early guide to the health of the manufacturing sector in July in Europe and the US.

{kind=link}