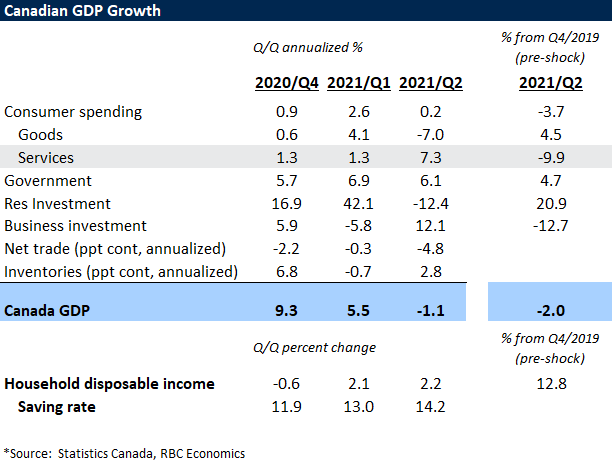

- GDP unexpectedly posted a 1.1% decline at an annualized rate in Q2.

- June output rose 0.7%, but early estimate for July was for a 0.4% decline – in contrast to expectations for a solid gain.

- High-contact service sectors bouncing back into the summer largely as expected, but supply chain disruptions and slowing housing markets keeping a lid on output.

The drop in Q2 GDP was surprising given earlier monthly GDP reports showing a modest increase despite the spring wave of virus spread and lockdowns. Activity bounced back 0.7% in June (matching the early estimate a month ago) but April and May data were revised to show larger declines. The larger surprise was a preliminary estimate that GDP declined 0.4% in July despite most provincial economies continuing to ease restrictions.

Our own tracking of card transactions shows spending in those hardest-hit high-contact service sectors like accommodation & food services continuing to accelerate through July, but supply chain disruptions are limiting goods production and a cooling in housing markets , which continue to come off the boil, means residential investment has shifted from a major driver of growth to a drag. Exports plunged 15% (annualized) in Q2 – led by a pullback in motor vehicle and parts production. Residential investment fell 12% on cooling home resale markets, but was still over 20% above pre-shock levels in Q2.

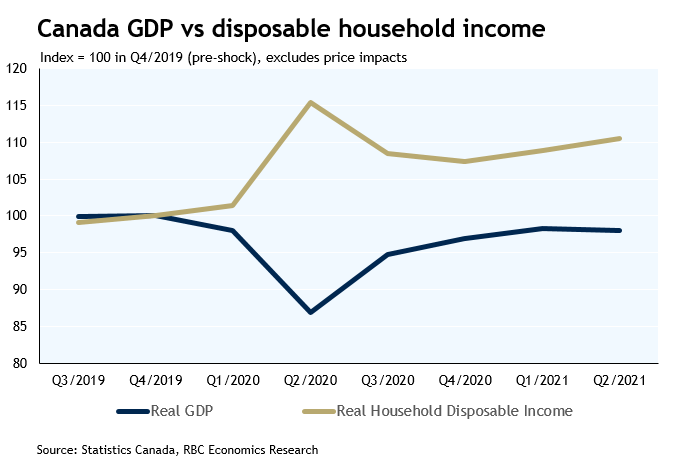

While the GDP numbers are clearly softer than expected, not all the data was bad. The preliminary estimate that July output dropped 0.4% was at odds with an earlier-reported 1.3% increase in hours worked that month. Business investment strengthened sharply in Q2, and household purchasing power continued to build. Household disposable income rose another 2.2% in Q2 (non-annualized) and the saving rate increased to 14.2%. Household spending on services was almost 10% below pre-shock levels, so there is still substantial room for stronger spending on services to help drive stronger economic growth over the second half of the year, even with goods production bumping up against capacity constraints. The recovery, particularly in spending on services, depends heavily on virus risk, but relatively high vaccination rates are expected to limit the need for a repeat of the widespread lockdowns of the last year and a half. All said, though, the data is clearly flagging less momentum than previously expected heading into the summer.

{kind=link}