U.S. Highlights

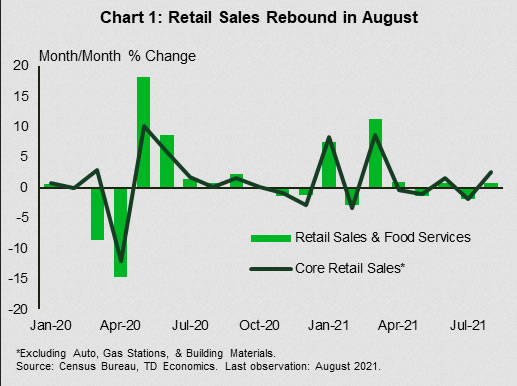

- Retail sales surprised on the upside in August, growing by 0.7% month-on-month. This followed a downward revision to the decline in July, but suggests resilience in the face of increased headwinds.

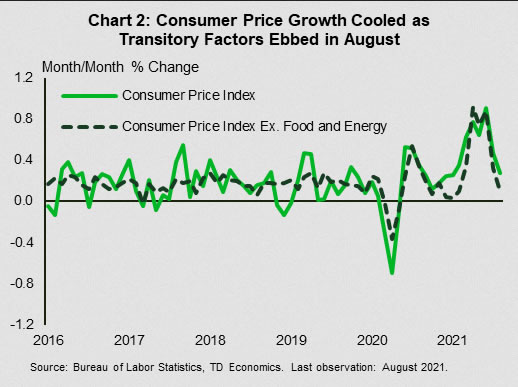

- Consumer price inflation slowed in August. From a peak of 5.4% year-on-year, the headline rate edged lower to 5.3%. Core inflation (ex. food and energy) decelerated more, moving from 4.3% to 4.0%.

- The Federal Open Market Committee will announce its next moves on monetary policy next week. It is likely to signal its intentions to begin tapering asset purchases in the near future.

Canadian Highlights

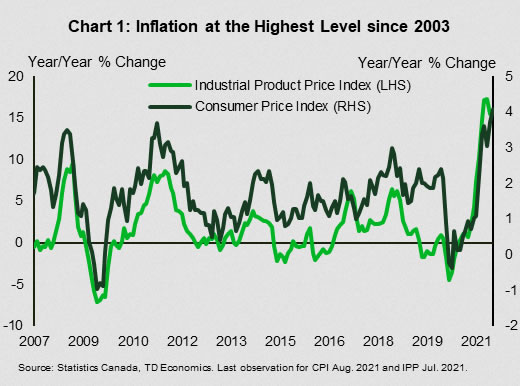

- Inflation accelerated to 4.1% year-on-year (y/y) in August from 3.7% in July, above the median analyst estimate for 3.9%. Durable goods prices were a major contributor to that acceleration, up 5.7% y/y (from 5.0% in July).

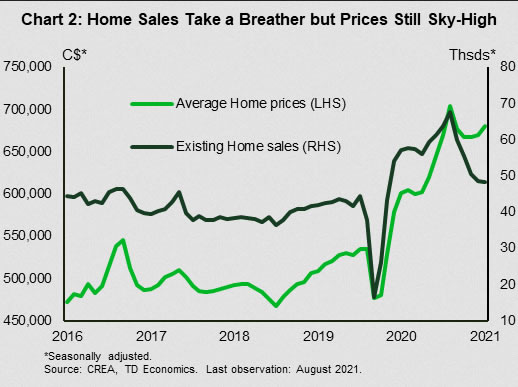

- Existing home sales dipped by a slight 0.5% m/m in August, marking the smallest of five straight monthly declines. Meanwhile, average home prices climbed a sturdy 1.7% month-on-month.

- The Delta variant continues to cast a shadow on the pace of the recovery. This week, Alberta declared state of emergency and re-imposed social distancing restrictions amid a record number of patients in ICUs.

U.S. – Transitory Setbacks vs. Transitory Inflation

The American economy continues to be buffeted by the pandemic and supply chain challenges. Still, it is showing its resilience. Retail sales in August surprised economists’ dour predictions for decline, rebounding by 0.7% month-on-month (Chart 1). A lack of inventory prevented consumers from spending on automobiles, while rising virus counts appear to have taken a toll on dining out. But, where consumers could spend, they did – at furniture and general merchandise stores, and, as they have been doing at a record pace since the pandemic began, at online retailers.

The rebound in retail sales is encouraging, showing there is still gas in the consumer tank and that while slowing after its stimulus-fueled surge in the first half of the year, it will not become a drag on economic activity. Even the sources of weakness in retail sales in August have a silver lining. The slowdown in auto production will not last forever. As long as demand is there, sales should rebound once inventories are rebuilt – if not this year, then next. The setback in spending at food services and drinking places is no doubt a consequence of the worsening virus trend, but there are signs of better days. Cases are now falling in the worst hit states.

At the same time, the acceleration in inflation – the consequence of buoyant demand and constrained supply – appeared to slow in August. Overall consumer prices were up 5.3% relative to a year ago, below the 5.4% peak in June and July. Excluding food and energy, the rate of core inflation slowed to 4.0% from 4.3%. The slowing is more evident on a month-on-month basis where price growth cooled to 0.3%, down from 0.5% in August and a peak of 0.9% in June. The core rate was up just 0.1% (Chart 2).

Just as important, some of the biggest contributors to inflation pulled back in August. For example, used vehicles prices had skyrocketed through the spring and early summer, adding over a percentage point to headline inflation, but pulled back 1.5% in August. This gives credence to the view that as the pandemic shock passes and transitory influences fade, the rate of price growth will also return to its pre-pandemic calm.

Into this to-and-fro, the Federal Open Market Committee meets next week to deliberate on the course of monetary policy. Importantly, the Fed’s statement will come alongside renewed projections for economic growth, unemployment and inflation. Economic growth projections are likely to be downgraded, but to rates that are still well above trend. The pace of improvement in unemployment is also likely to be slowed, but still make progress. The inflation forecast is also likely to see an upgrade in the near-term, marking to the data.

With these economic views, the Fed is likely to communicate that in order to ensure inflation remains transitory it must begin preparing to withdraw policy support. The first step is to slow the pace of asset purchases, which is likely to happen this calendar year. The Fed’s statement is likely to emphasize that this does not mean that policy rate hikes are around the corner, but as long as growth continues, they may not be too far on the horizon.

Canada – Blame Both Supply & Demand for Inflation

Inflation and housing data took center stage this week, with both likely to be important issues for Canadians as they head to the polls next week. On the inflation front, consumer prices continued to rise in August, accelerating to 4.1% year-on-year from 3.7% in July. One must time travel all the way back to 2003 to experience inflation at a similar level.

While the increase in consumer prices is notable, they are rising from last year’s low levels when Covid-19 restrictions were still weighing on demand and prices for many goods and commodities. Energy prices are a case in point. Last month gasoline prices were up a whopping 33% relative to a year ago. Excluding gasoline, consumer price growth appears tamer at 3.2% year-over-year. Service prices were also depressed last year, but are now also on the rise as consumers resume travelling, dining out and other postponed activities.

Recovering consumer demand is just one part of the story. Ongoing supply-chain disruptions are also putting upward pressure on usually-benign goods inflation, with durable goods prices up 5.7% from the year ago. With retailers trying to rebuild inventories, container freight shipping costs have risen exponentially this year. Furthermore, developing countries – where many consumer goods are manufactured – are also dealing with pandemic-related disruptions and shutdowns of their own. High commodity prices and shortages of inputs are, in turn, leading to higher prices at factory gates. The industrial product price index, which tracks prices for major commodities sold by Canadian manufacturers – is up 15% from the year-ago (Chart 1).

While talking about inflation, it’s hard not to mention the housing market – another area where prices have been on fire over the last year and half. Activity in the housing market has come off the boil in recent months, but prices remain elevated. Including this week’s August data, home sales have been falling for five consecutive months and were just 8% above their pre-pandemic level. Meanwhile, price pressures, which had been easing over the spring and early summer, picked up again in August, rising a sturdy 1.7% month-on-month (and up 27% from where they were in February 2020, Chart 2). Even with the drop in sales, inventories of homes for sale also remain very low. As a result, the housing market is still tight and firmly in sellers’ market territory. This is likely to continue to put upward pressure on home prices in the near-term.

All told, inflation is likely to remain elevated for the remainder of this year even as downside risks to domestic and global growth emerge as a result of the Delta variant. On that front, this week Alberta declared a state of emergency and re-imposed social distancing restrictions amid a record number of patients in intensive care units. Still, the pandemic is increasingly just as much a supply as demand problem and while price growth may slow in some areas, it may push even higher in others. As long as economic growth is only postponed, the Bank of Canada will continue to reduce the pace of its asset purchases in order to ensure that inflation remains temporary. Policy rate hikes are likely still not on the immediate horizon, but pose the question a year from now and the answer is likely to be different.

{kind=link}