- Today’s ECB meeting ended with no new decisions or a signal about the decisions that are to be taken at the December meeting, as widely expected (see our preview here). Lagarde personally expected PEPP to end in March22. TLTRO would be part of the December discussion.

- ECB concluded that the growth risks are broadly balanced, while at the same time acknowledging that the euro area is witnessing slower momentum.

- ECB’s transitory inflation narrative, citing rising energy prices, supply-demand mismatches and German VAT base effects as the main drivers for current high inflation rates.

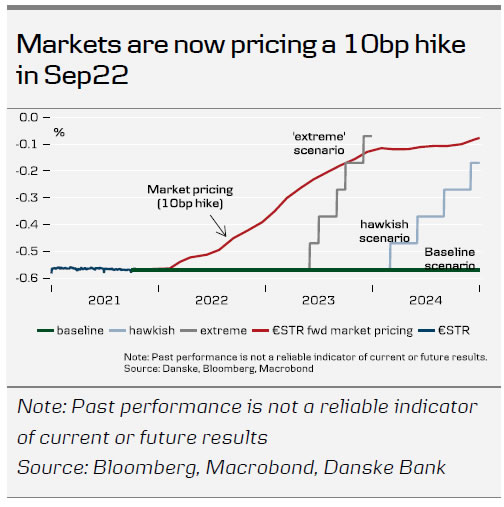

- Regarding market pricing, there was some convoluted push-back, which leaves ECB data dependent. So far, ECB was not concerned about the recent increase in short-term rates’ impact on financing conditions.

Inflation, inflation, inflation – but not like other central banks!

At today’s ECB meeting, ECB discussed three things according to Lagarde: Inflation, inflation and inflation. She boiled the conclusion down to three factors that drives inflation (see below), that made ECB conclude that the recent inflation pressures are transitory.

We had two main questions that we sought to get answered today

1) Not like other central banks: Asked to the question of ECB compared to other central banks that are turning more hawkish she said that comparison was ‘odious’.

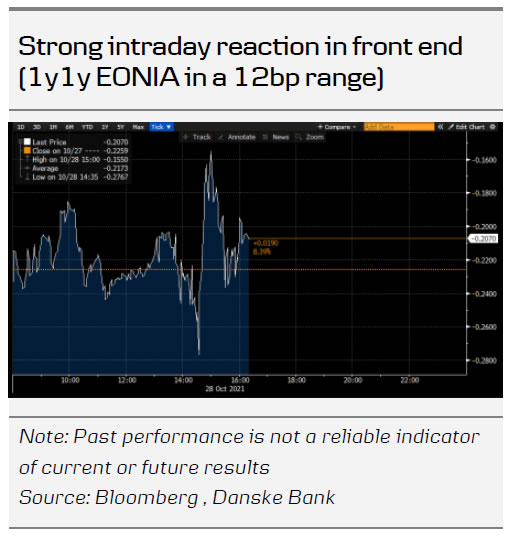

2) Markets pricing are ahead of themselves: Lagarde was asked several times on this issue. The first time was clear that ECB do not agree with market pricing, however the subsequent answers were less convincing, which also lead to strong intraday reaction in markets, where for example 1y1y EONIA swap traded within a 12bp top to bottom range through the press conference. On her clearest answer she said that; ‘Our analysis certainly does not support that the conditions of our forward guidance are satisfied at the time of liftoff as expected by markets nor any time soon thereafter,’

Ultimately, we are of the view that ECB do not expect to hike rates in the foreseeable future given ECB transitory inflation narrative. Whether this new found data dependence will last remains unknown. In any case, if inflation proves longer-lasting, the comments today makes us less confident that ECB would not change policy rates eventually.

ECB says inflation surge is transitory, but markets doubt it

During the press conference, Lagarde stressed that the euro area economy continues to recover strongly, although momentum has moderated. While consumer spending remains strong, supply shortages are holding back production, clouding the outlook for the coming quarters. That said, risks to the economic outlook are still seen as broadly balanced and Lagarde also downplayed the risk of stagflation, arguing that there is no ‘stagnation’ in the first place (just somewhat slower growth momentum).

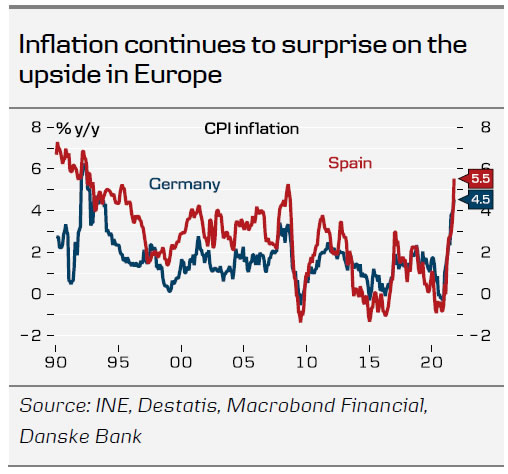

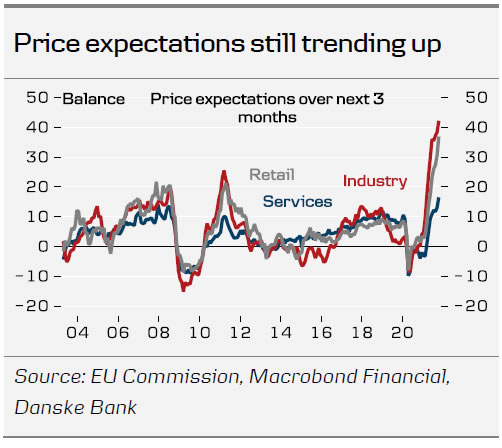

Lagarde also clearly stayed true to the ECB’s transitory inflation narrative, citing 1) rising energy prices, 2) supply-demand mismatches and 3) base effects (such as German VAT) as the main drivers for current high inflation rates. While inflation is expected to stay high in the near-term (lasting a bit longer than previously expected), ECB still expects inflation pressures to ease again over the course of next year. One important reason for this remains that ECB does not yet seem worried about a wage-price-spiral, stating that the gradual return to full capacity will underpin a rise in wages only ‘over time’. Upcoming wage rounds in Germany during 2022 will be key to watch in that respect in our view (see Research Euro Area – German wages: what to watch in 2022, 25 October). However, with Spanish and German CPI inflation surging to the highest level since the 1990s in October and price expectations still adjusting upwards across sectors, markets are increasingly discounting ECB’s temporary inflation narrative.

EUR/USD uptick to prove temporary

Despite Lagarde’s very dovish signals and overall appearance, EUR/USD followed the rates market higher. In our view, this is likely a temporary correlation and likely to soon be replaced by more downside risk as the European economy underwhelms amid inflation surprises. We do not generally see much of a link between spot EUR/USD and rising expectations towards euro area interest rates. On the contrary, Fed will probably lean more in to their hawkish views and arguably, too, the economy is better equipped at handling a slight slowdown in growth and higher yields. On net, we continue to forecast 1.10 in 12M EUR/USD.

{kind=link}