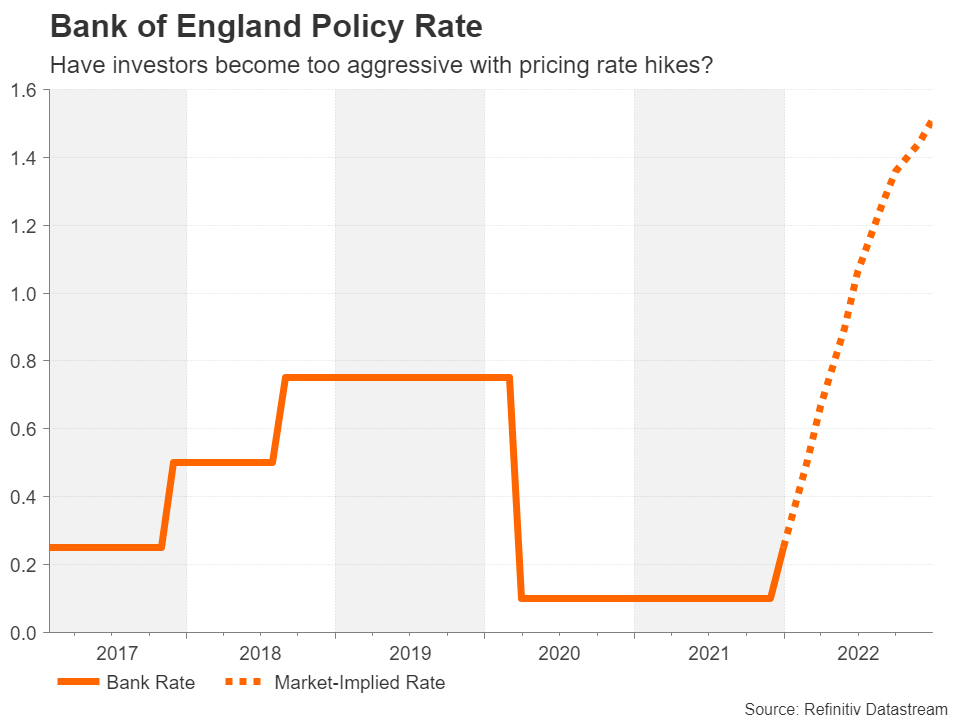

The Bank of England is widely anticipated to raise interest rates to 0.50% on Thursday when it announces its decision at 12:00 GMT. Having already lifted the Bank Rate in December, the expected hike in February would make it the first time since 2004 that the BoE has tightened policy in two meetings in a row, underscoring not only the urgency to cap price growth but also just how long it’s been when inflation was last such a big threat. Yet, rate hike bets haven’t been powerful enough to defend the pound from the US dollar’s recent assault. Can a hawkish tone revive cable’s uptrend?

Worries about rising cost of living

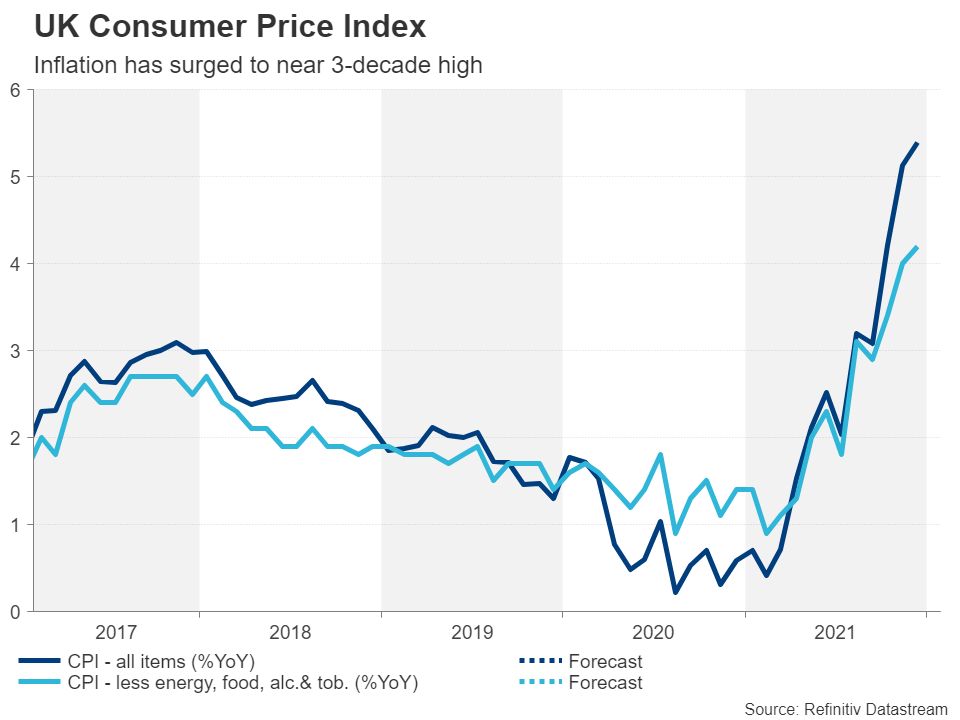

Inflation in the UK hit a near 30-year high of 5.4% y/y in December and the upsurge could get even greater in the coming months as energy bills are set to soar in April when the price cap is raised by the country’s regulator. With Britain’s labour market tightening very rapidly lately, the conditions are ripe for a wage-price spiral as employees feeling the strain of a jump in the cost of living find themselves with wage bargaining powers for the first time in years.

No shocks expected in February

Money markets have fully priced in a 25 basis points rate rise in February, to add to December’s 15-bps increase that lifted the Bank Rate back up to 0.25% from historic lows. But the rate hike expectations don’t stop there as investors are betting on at least four additional increases during the course of the year. Interestingly, the Bank of England is one of the few central banks that generally tends to agree with market pricing, nudging traders in the right direction only if it sees a risk of it missing its 2% inflation target by following the market-implied path.

Policymakers tried to do this back in the Autumn when they first started to panic about higher inflation. But their clumsy communication still ended up wrong-footing many investors in both November and December. That’s not likely to happen this time round, although the BoE could still surprise in two ways on Thursday.

Will BoE flag danger ahead?

Firstly, the Bank’s quarterly Monetary Policy Report will be crucial in letting markets know whether the current implied path is consistent with hitting 2% inflation within the forecast period. The main risk here is that policymakers might think markets have become too aggressive with rate hike expectations.

Whilst it’s fair to say that the UK economy is fairly strong right now and the recovery has been impressive given that it suffered more than all other major economies from the initial pandemic meltdown, the outlook is as uncertain as ever. British consumers face a double squeeze in spending power over the next few months, as apart from the looming surge in fuel bills, they are also about to be struck by higher taxes in the form of an increase in national insurance contributions.

Combined with a rise in borrowing costs, spending by both households and businesses could take a major hit and the Bank might make a point of stressing this risk in its report. However, policymakers’ recent hawkish rhetoric suggests this won’t be a significant concern for them at this point and the bigger question mark heading into the meeting is what the Bank will say concerning the balance sheet.

Balance sheet runoff eyed

Like the Fed, the BoE’s balance sheet has ballooned during the pandemic and with inflationary pressures emerging from all over the place, a decision on reducing it is more than likely. Policymakers already signalled last year that the balance sheet could begin to shrink when the Bank Rate reaches 0.50% instead of their previous guidance of 1.50%. However, they could go one step further than that and announce the outright selling of assets, namely, gilts.

In all likelihood, a decision on the latter will be saved for a later date and the most investors should expect is the balance sheet will be allowed to run off by not reinvesting in maturing bonds. Nevertheless, Governor Andrew Bailey could hint at a future sale of bonds in his press briefing, potentially boosting gilt yields.

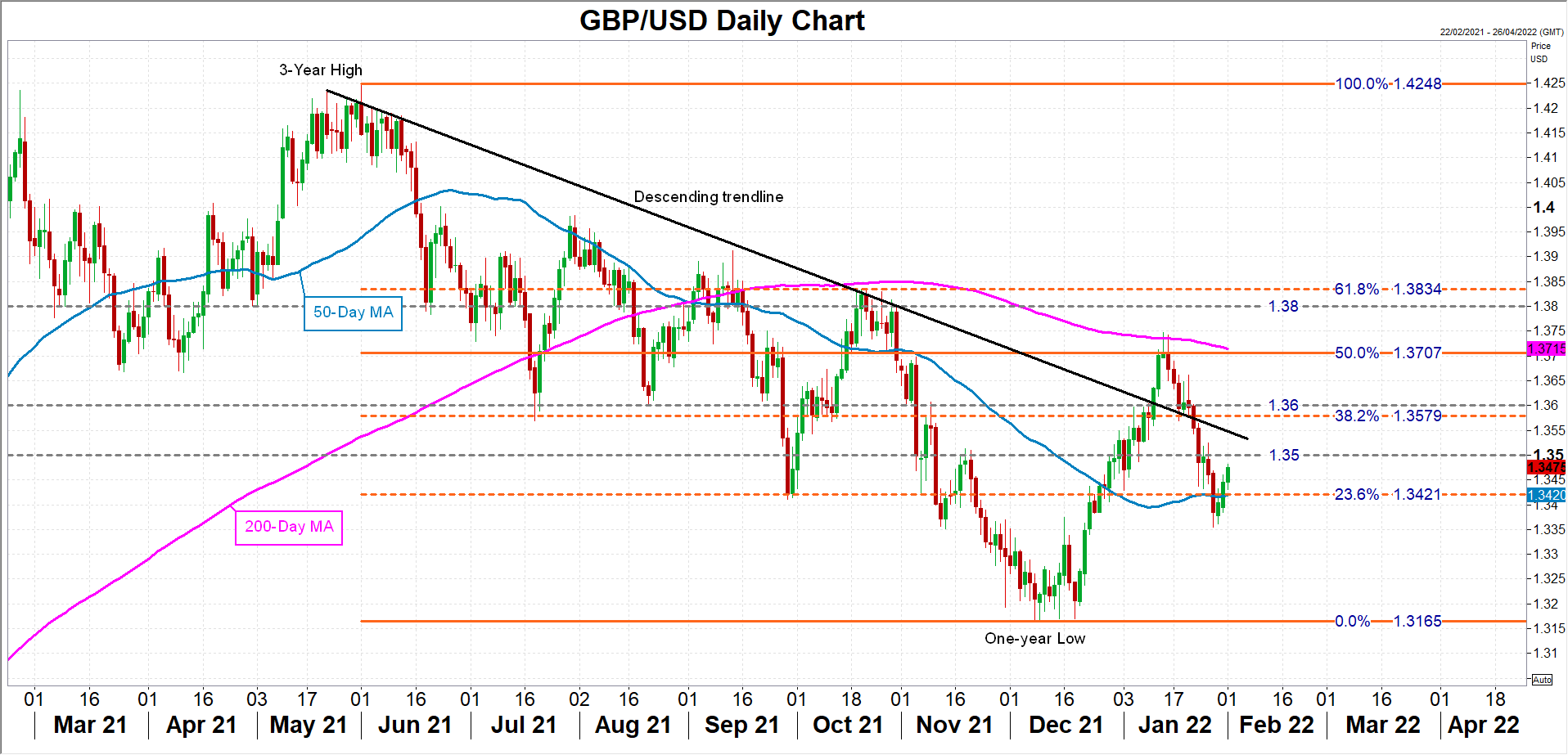

Pound finding its feet again

The UK 10-year yield has just crossed above 1.30% for the first time since March 2019 and a further spike could help sterling claw back some of its recent losses against the greenback. The $1.35 and $1.36 level are key targets for cable in the near-term as they stand in the way of re-challenging the January top of $1.3748. Only a break above this high can restore the pound’s bullish posture.

Alternatively, if the BoE tries to talk down some of the more hawkish market expectations, cable can slip back below its 50-day moving average and revisit December’s one-year trough of $1.3165.

In the meantime, the pound has been paying little attention to the happenings in No. 10 Downing Street where Boris Johnson is under pressure to resign. The stripped-down report into the alleged breaches of lockdown rules by Downing Street staff, including the Prime Minister, has found there were serious failings in leadership. Johnson has apologised and appears to be clinging on for now. However, the police are also investigating some of those events and the full report that is expected to be published after the police inquiry has ended could be more damning. Thus, the drama for Johnson is far from over.

{kind=link}