U.S. Highlights

- Another solid jobs report showed that the U.S. economy added 431k jobs in March. Wage growth picked up and the unemployment rate fell 0.2 percentage points to 3.6%.

- President Biden presented a $5.8 trillion budget to Congress with a hefty focus on defense spending. Separately, the President also announced releases from the strategic petroleum reserve to combat rising energy prices.

- Nominal consumer spending and income rose in February. Real income, however, pulled back as prices rose rapidly. Inflation, as measured by the year-on-year percent change in the personal consumption price index accelerated to 6.4%.

Canadian Highlights

- Fiscal policy dominated headlines this week as Ontario signed on to the national child-care plan and an update on climate change initiatives was announced.

- These developments come ahead of the expected release of the federal government’s budget next week (April 7th) which is likely to feature new measures to address housing affordability and other platform promises.

- With economic data continuing to show healthy growth the groundwork is set for a 50-basis point hike by the Bank of Canada in April.

U.S. – Economic Recovery Battles Inflation Headwinds

On the agenda this week were several important data releases including consumer income and spending, manufacturing activity, and the March employment report. President Biden also released his budget proposal and announced a plan to release supply from the strategic petroleum reserve in order to combat rising prices.

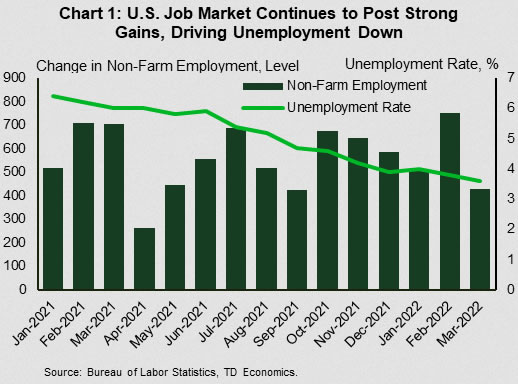

Jumping right in, nonfarm payrolls expanded by 431k in March with most sectors posting job gains. The only exceptions were transportation & warehousing and utilities. The unemployment rate edged down to 3.6% from 3.8% in February as household employment growth exceeded growth in the labor force (Chart 1). Wages continued to post solid year-on-year growth, ticking up from 5.1% in February to 5.6%. Overall, the report indicates a job market driving full steam ahead, and barring further disruptions, could be back to its pre-pandemic level of employment by the middle of the year.

The ISM Manufacturing Index indicated that factory activity, while still expanding, slowed in March. The index pulled back to 57.1 from 58.6 the month before. There were notable declines in new orders and an increase in prices paid. On the upside, the backlog of orders declined, while the employment index rose.

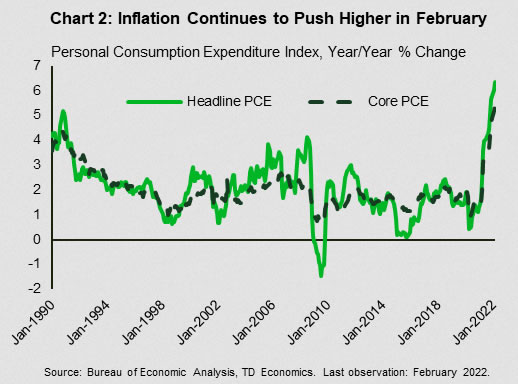

Turning to the household sector, nominal personal income and spending rose 0.5% and 0.2% respectively in February. An even stronger gain in prices however took a bite out of real disposable income, which declined for the third consecutive month, largely reflecting waning transfers to households. Inflation, meanwhile, continued to accelerate. The personal consumption expenditure (PCE) index rose 6.4% year-over-year (y/y) versus 6.1% in January (Chart 2). The core PCE index also accelerated to 5.4% y/y in February, up from 5.2%. From the Fed’s perspective, inflation is uncomfortably high as supply chains remain stressed, Covid shutdowns in China hamper trade and the Russian-Ukraine war sparks further volatility.

In response to rising energy prices, President Biden plans to release up to 180 million barrels of oil from the strategic reserve over the next six months. While the release may help to alleviate near-term market tightness, the reserve is currently at a 20-year low. Further releases would drive the stockpile even lower, ratcheting up risks surrounding global spare capacity over the longer term.

Finally, President Biden presented his budget proposal for the 2023 fiscal year. The $5.8 trillion budget would raise taxes on billionaires and corporations. A new tax proposal would require households worth more than $100 million to pay a rate of at least 20% on their income as well as a tax on unrealized capital gains on assets such as stocks, bonds, or privately held companies. On the spending side, the budget would increase spending on the military, law enforcement, affordable housing and supply chains, while attempting to reduce the federal deficit by $1 trillion over a decade.

Canada – Fiscal Plans Take the Spotlight

Fiscal policy news dominated the headlines this week in Canada, as the last province signed on to the national child-care initiative, the federal government outlined a plan to reduce greenhouse gas emissions, and attention shifts to the federal budget announced to be released next Thursday (April 7th).

Early this week, Ontario signed on to the federal daycare program, setting the stage for a 50% reduction in daycare fees by the end of the year – on the path to $10 per day care throughout the province. The program is estimated to save the average family $6,000 per child in 2022. With inflation ripping at multi-decade highs reduced expenditures for a big line item in young families’ budgets is a welcome lift.

Next, the federal government rolled out its 2030 Emissions Reduction Plan. The plan outlines the path to achieve a 40-45% reduction in carbon dioxide emissions (relative to 2005) by 2030 – with an intermediate goal of a 20% reduction by 2026. To help meet the target, an additional $9.1 billion in funding for new investment was announced.

Following these major announcements, the federal budget will be released next week. Announcements will likely include measures addressing housing affordability, healthcare spending, details on the actions combatting climate change, and possibly some funds to offset the effects of high inflation. Chart two shows the trajectory of two regional FRB manufacturing surveys on an ISM adjusted basis. The Empire State and Philadelphia Fed manufacturing surveys showed a noticeable deceleration in growth in January, notching multi-month lows. The Empire state survey fell from 60.8 to 54.4, while the Philadelphia Fed survey fell from 60.2 to 57.6. Importantly, both readings still indicate expansion, but slower than in the prior months.In totality, these initiatives will likely raise expenditures by roughly $10 billion per year over the next five years. Moreover, with the war in Ukraine turning attention to defense spending, additional investment on this file is likely.

Revenue raising measures are likely to be modest. A banking and insurance sector tax seems probable, carbon taxes are set to rise, and there may be some levies on foreign investment in housing. However, these are not going to be the focus of the budget. Moreover, despite only modest additional revenue measures, the trajectory for the deficit will likely remain unchanged as higher inflation will lift tax revenues and bolster government coffers.

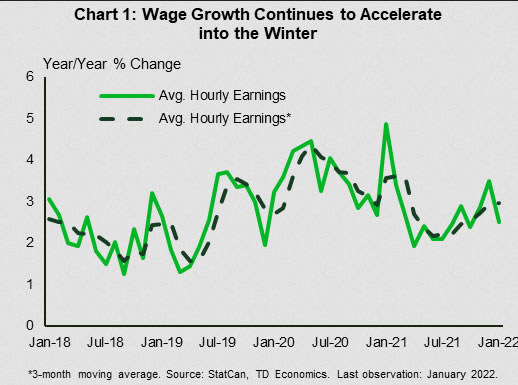

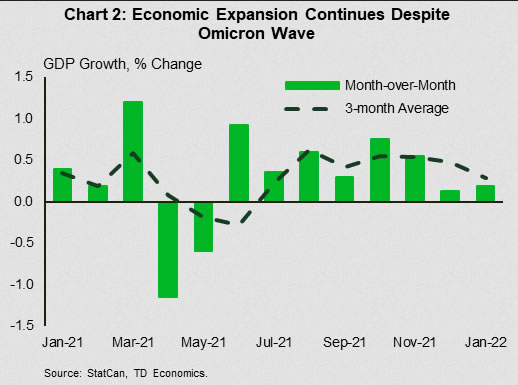

Economic data this week showed solid wage growth continued into 2022 (Chart 1) as the fixed composition wage measure in the Survey of Payrolls, Employment and Hours posted a 2.5% year-over-year gain in January 2022. January’s GDP number confirmed that pandemic restrictions didn’t stop the expansion (Chart 2) and with most restrictions in the rearview mirror, and strong growth in February, the recovery continues to gain steam.

Amid strong economic growth, an increasingly tight labor market, and fiscal fuel being added to the fire, look for the Bank of Canada to continue leaning against inflation by raising rates 50 basis points at its April meeting.

{kind=link}