The latest flash PMI and retail sales figures for the UK are due on Friday at 06:00 GMT and 08:30 GMT, respectively. These will be the last batch of major indicators before the Bank of England’s policy decision on May 5 so investors will be gauging them to get a sense of policymakers’ thinking on further rate hikes this year. Worries about slowing growth amid the cost of living crisis have been weighing on sterling since Russia’s invasion of Ukraine. Can the numbers lift the British currency out of the doldrums?

End of Covid rules is boosting services

Recent data out of the United Kingdom have been mixed. GDP grew a mere 0.1% month-on-month in February, but the survey data have been a lot more upbeat. The dominant services sector is still benefiting from the lifting of all virus curbs while the labour market continues to tighten. These effects were probably enough to sustain economic momentum in the early parts of April.

The services PMI is expected to moderate from 62.6 in March to 60.3 in April, remaining comfortably above the 50-neutral level that separates expansion from contraction.

Manufacturers are feeling more gloomy

However, the PMI indices globally are being inflated from record increases in their price components, overstating the true strength in business activity. Moreover, optimism is weakening, not just from the worsening cost pressures, but also from the uncertain outlook due to the heightened geopolitical tensions.

These have already begun to weigh on manufacturing firms, much more so than on services industries. UK manufacturers reported waning demand for consumer goods from both domestic and overseas clients in March and this trend likely accelerated in April. The manufacturing PMI is forecast to decline from 55.2 to 54.0 this month.

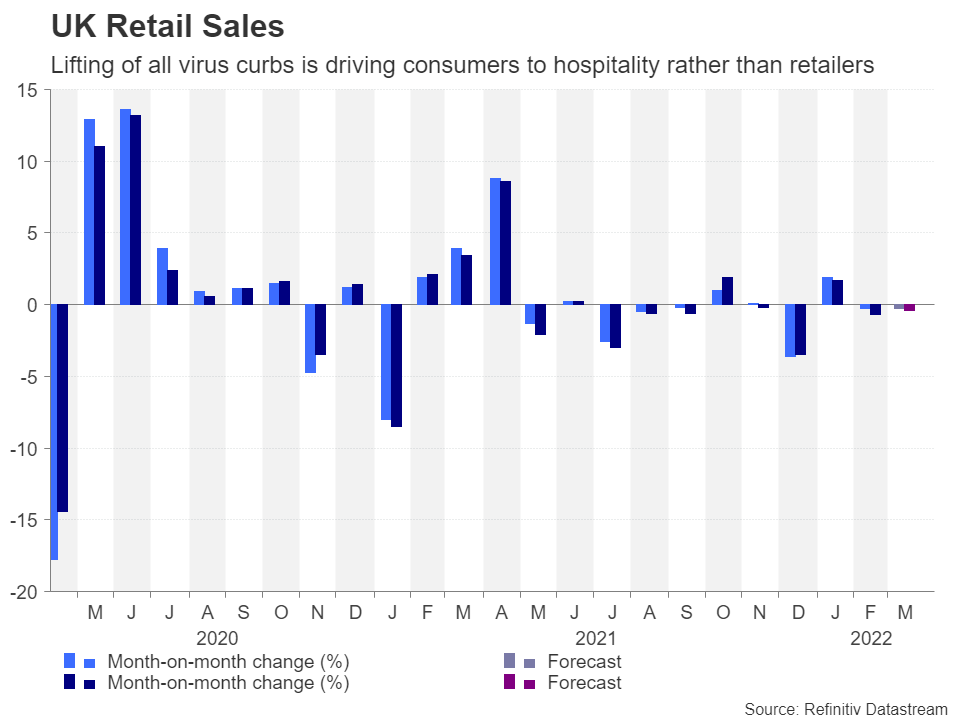

The big consumer squeeze is here

Higher food and fuel prices have started to eat into households’ disposable incomes, so consumers are naturally spending less on other goods as inflation hits 30-years highs. The full reopening of the British economy at the end of February has been a further drag on retailers as people have preferred to enjoy going to theatres and restaurants with no restrictions rather than to hit the high street.

Retail sales are expected to have fallen by 0.3% m/m in March. When excluding fuel sales, the drop is projected to have been slightly bigger at 0.4%. But what is more worrying is that the squeeze on consumers is only just starting. Many UK households will see their electricity and gas bills jump in April after the country’s regulator raised the cap energy firms can charge their customers. Adding to the pain, the national insurance rate went up for many taxpayers at the beginning of April, dealing a double blow to consumers.

BoE has been less hawkish lately

With the war in Ukraine also not looking like it will end anytime soon either, the growth outlook has dimmed significantly in the last few months, prompting the Bank of England to take a more precautionary stance against rapid rate increases. Despite that, expectations for how many times the BoE will have to raise rates by year-end remain elevated, with investors anticipating six additional 25-basis-point hikes on top of the 50 bps already delivered.

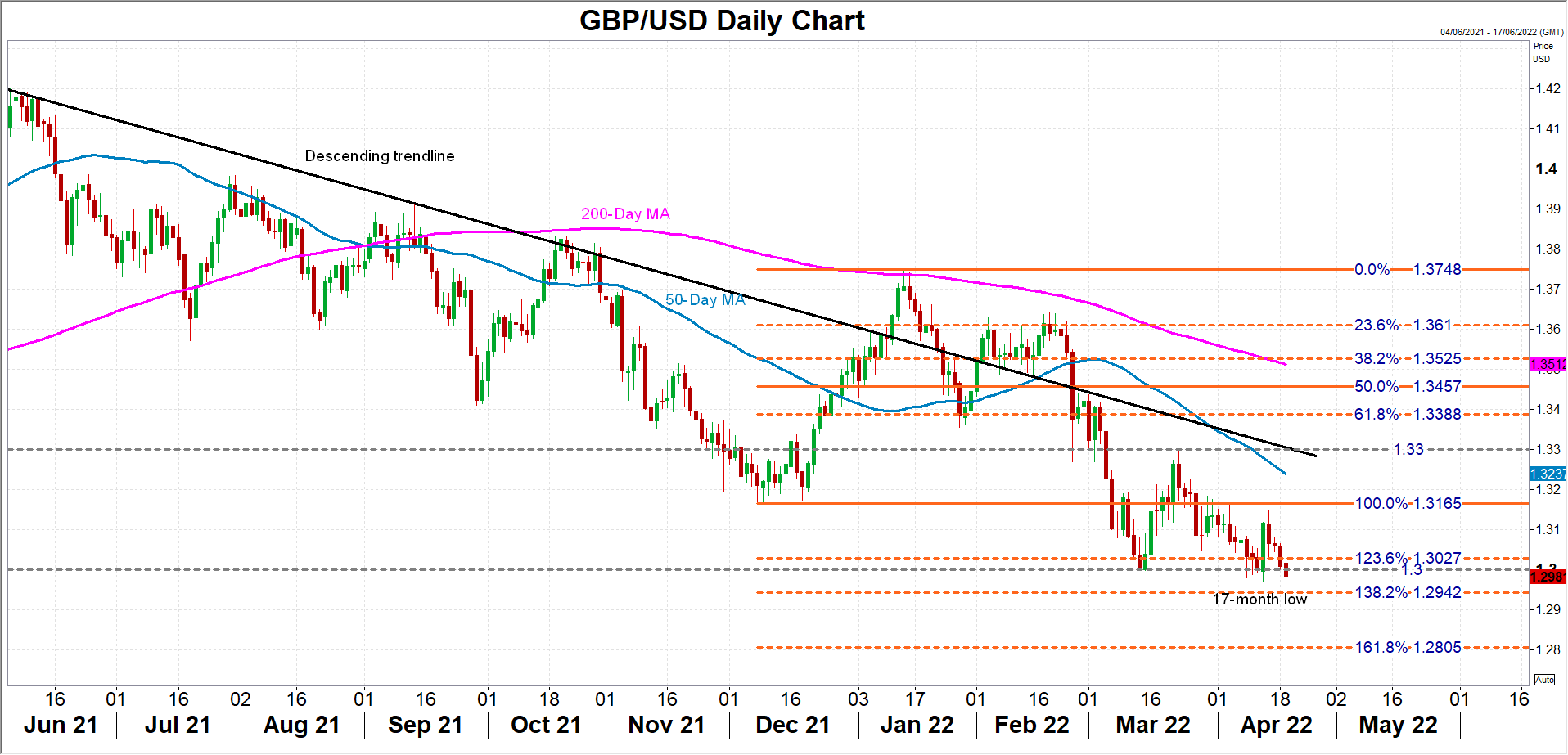

But those hawkish bets haven’t done the pound any favours, at least not against the US dollar. Concerns that the UK is headed for a stagflationary environment has been a major dampener on the pound this year. Cable brushed a 17-month low of $1.2970 earlier this month and is struggling to regain a foothold above the $1.30 handle.

Cable is testing $1.30 level again

Should the upcoming releases disappoint, intensifying fears about a slowdown or even a recession, sterling could slip as low as $1.28, which is just below the 161.8% Fibonacci extension of the December-January uptrend.

On the other hand, positive surprises in the data could help the pound regain some bullish posture and bring into scope the 50-day moving average at $1.3238.

Nevertheless, the odds of a big upside reversal are low at the moment for cable. A slightly more hawkish-than-expected tone by the BoE at the May meeting could potentially go some way in changing its fortunes around. But as things stand, the pound’s best hope is a de-escalation of the Russia-Ukraine conflict.

{kind=link}