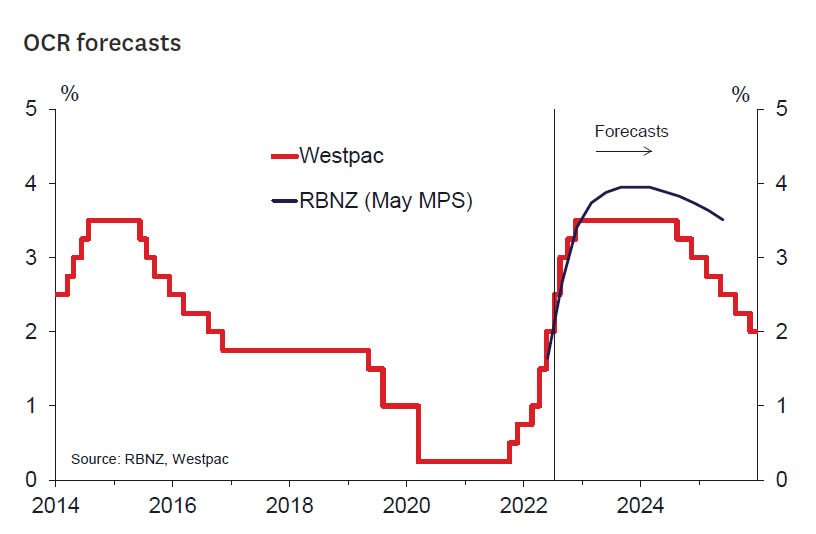

- The Reserve Bank increased the OCR by another 50 basis points to 2.50% as widely expected.

- The RBNZ endorsed the OCR path that it projected in its May Monetary Policy Statement, and repeated much of the language from that as well.

- The RBNZ’s focus remains on the risk of homegrown inflation pressures becoming persistent, with strong demand running up against capacity constraints.

- We continue to expect another 50 basis point hike in August.

- By that point, the OCR will be much closer to where we (and the RBNZ) see the peak for this cycle.

The Reserve Bank’s decision to lift the Official Cash Rate by another 50 basis points was almost universally expected. Not only was the move right in line with the path that the RBNZ projected in its May Monetary Policy Statement, but the key language in today’s statement was mostly identical. The RBNZ remains “resolute” in its commitment to bringing inflation back within the target range, and it intends to keep lifting interest rates “at pace”.

The lack of change in the message is itself the message. The RBNZ has not been fazed one way or another by recent developments, and its focus remains on the medium-term outlook. That’s useful to know – the alternative was that the RBNZ could have followed the more downbeat tone that has pervaded financial markets in recent weeks, with inflation being replaced by recession as the ‘big bad’.

The RBNZ is certainly not oblivious to recent developments, referencing both upside risks to inflation and downside risks to activity in the near term. But its focus remains on the mediumterm outlook and the homegrown inflation pressures that are becoming more pervasive. Demand continues to outstrip the economy’s capacity, and skill shortages and Covid disruptions certainly don’t help.

The RBNZ noted that the OCR path that was projected in its May Monetary Policy Statement is still broadly consistent with meeting its inflation and employment objectives. The addition of “broadly” could be taken to imply some wiggle room around what that projection would look like if they re-ran it today. But any meaningful change to the OCR path is more likely to come down to the flow of data between now and the August statement. That includes the CPI next Monday, the labour market surveys in early August, and the survey of inflation expectations, which remain a key concern for the RBNZ.

We continue to expect a fourth 50 basis point hike at the August review, which would bring the OCR up to 3%. It’s at that point that we might see a change of tone from the RBNZ. For one, the OCR will by then be much closer to the endpoint that the RBNZ envisages (the May projection peaked just below 4%), so the logic of “a stitch in time saves nine” becomes less relevant. Secondly, the Monetary Policy Committee will have the benefit of a full set of economic forecasts in August, along with additional time to consider the softening global backdrop. At that point, the RBNZ could signal that further rate hikes are likely, but the pace and extent of them will be played by ear.

There is one final aspect of the RBNZ’s forecast (and ours) that hasn’t garnered much attention yet: once the OCR does peak, it’s likely to fall again in the years to come. The RBNZ has been clear that in order to get on top of the inflationary pressures that have built up, it needs to take monetary policy settings above ‘neutral’ and into ‘tight’ territory, for at least some time. In other words, this is a good old-fashioned cycle, not a permanent shift.

That idea hasn’t really been reflected in longer-term market interest rates, which are more consistent with the OCR rising and staying there. If the economic outlook does turn gloomier from here, there’s plenty of scope for a fall in longer-term interest rates – and a de facto easing in monetary conditions – without the RBNZ having to do anything differently. So for now the RBNZ can afford to keep up its inflation-fighting message, without making concessions to the market’s worries.

{kind=link}