Summary

- Japan’s economy has been reasonably resilient so far in 2022. Growth has been moderate, although confidence surveys suggest mixed prospects for different economic sectors, consistent with only moderate growth ahead.

- We also expect relatively contained inflation going forward as well. While prices are elevated compared to recent history, inflation remains low by international standards.

- As for the currency, historically there have been two important drivers for movements in the yen: the currency’s safe haven characteristics and Japan’s yield differentials with the rest of the world. In more recent times the yen’s safe haven properties seem to have diminished to some extent, whereas yield differentials have remained a better indicator of potential trends in the yen.

- Given that yield spreads appear to be the more influential driver, trends in global monetary policy, especially those of the Federal Reserve, should be influential for the yen. The increasing divergence in monetary policy between a hawkish Federal Reserve and dovish Bank of Japan means we believe the yen still has room to weaken against the U.S. dollar in the medium term, even if the Ministry of Finance intervenes in FX markets again to support the currency.

- We believe that as yields continue to diverge, the yen can weaken toward a USD/JPY exchange rate of JPY149.00 by Q1-2023, before recovering somewhat as next year progresses.

Only Moderate Economic Growth Ahead for Japan

Japan’s economy has been reasonably resilient so far in 2022. Growth has been moderate; the economy expanded 0.9% quarter-over-quarter (not annualized) in the Q2, following a mere 0.1% gain in Q1. Taking a closer look at the details of the Q2 GDP report, this growth was broad-based, with private consumption growing 1.2% over the quarter and business capital spending increasing by 2%.

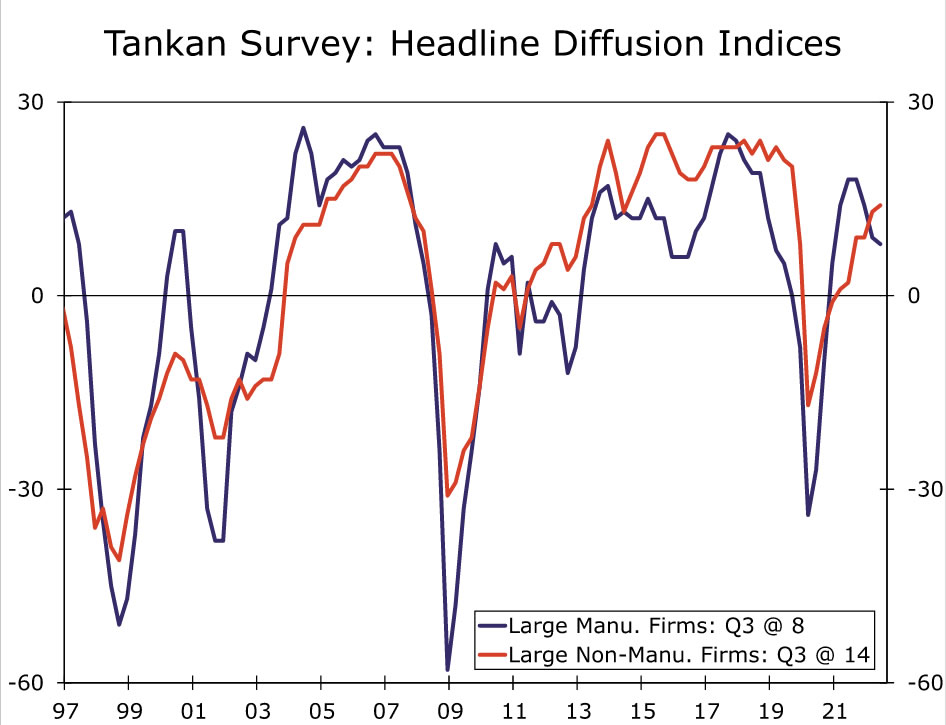

However, key measures from the Bank of Japan’s Q3 Tankan surveys showed business sentiment in some sectors becoming less upbeat. Confidence at large manufacturing firms continued to soften in Q3, with the large manufacturers’ diffusion index unexpectedly falling one point to 8 in Q2, the third consecutive decline. A positive Tankan survey reading indicates that of the surveyed businesses, optimists outnumbered pessimists. So while in Q3 some optimists likely became pessimists, there are still more optimists than pessimists overall. Future expectations also became less positive, as the forward-looking outlook measure for manufacturing firms fell one point to 9.

Meanwhile, service sector sentiment improved, with the large non-manufacturing index ticking up to 14 from 13, as Japan gradually reopens its borders to travel and tourism. However, uncertainty regarding how the service sector will fare amid a global slowdown may be clouding future expectations, as the outlook reading fell two points to 11. Ultimately, softening confidence is consistent with our expectation for only moderate growth ahead.

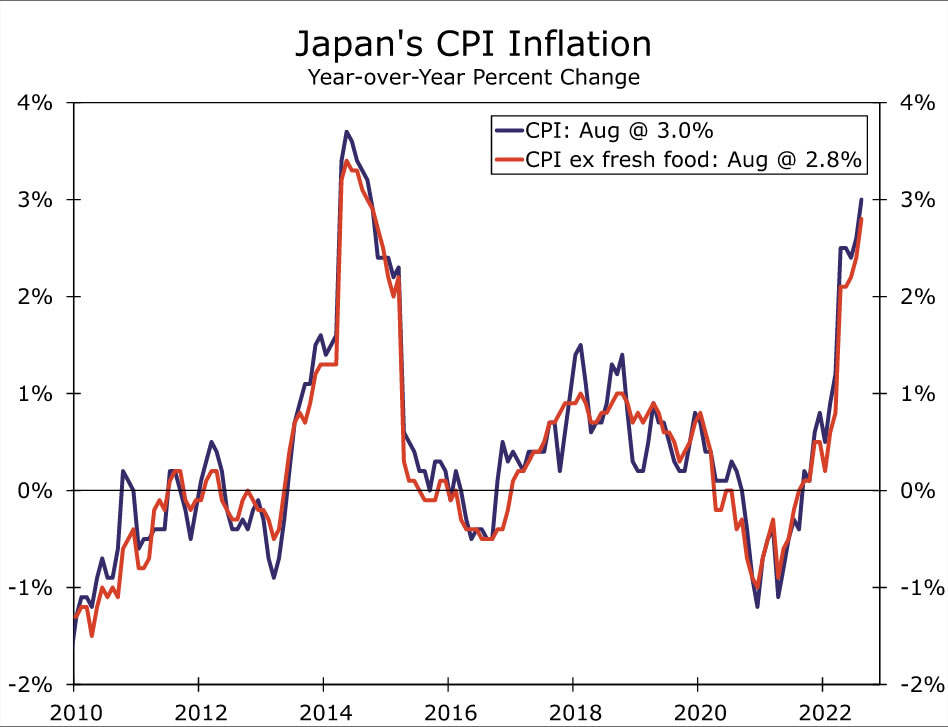

As for inflation, prices have picked up and are elevated compared to recent history, although inflation remains low by international standards. In August, nationwide CPI inflation reached 3.0% year-over-year, with the CPI excluding volatile components like fresh food and energy lower at 1.6%. We expect these moderate trends for growth and inflation to continue in 2022.

Bank of Japan: Easy Does It

With only limited growth and inflation as well as softening sentiment, we expect the Bank of Japan (BoJ) to maintain its easy monetary policy stance in the near-to-medium term. At the BoJ’s September meeting, the central bank was clear that no rate hikes are on the table. Thus, we do not expect any shift in the BoJ’s key policy parameters—the policy rate and the 10-year government bond yield target—for the foreseeable future. BoJ Governor Kuroda has said monetary easing will support the economy and help prevent a downturn, and the BoJ won’t hesitate to add to easing if needed.

Given the yen’s continued depreciation against the U.S. dollar, the Ministry of Finance recently intervened in currency markets for the first time in over 30 years, spending US$19.7B in September to support the currency. While the yen surged initially, that gain proved to be short-lived. The yen is currently down around 20% against the U.S. dollar year-to-date, and the Ministry of Finance has warned of yet another intervention to prop up the currency, committing to take “bold action” if there are “excessively one-sided moves”. Ultimately, we still expect weakness in the yen versus the U.S. dollar in the coming quarters, and view intervention as likely to provide only temporary relief for the currency.

Safe Haven vs. Yield Differentials: Which is More Influential for the Yen?

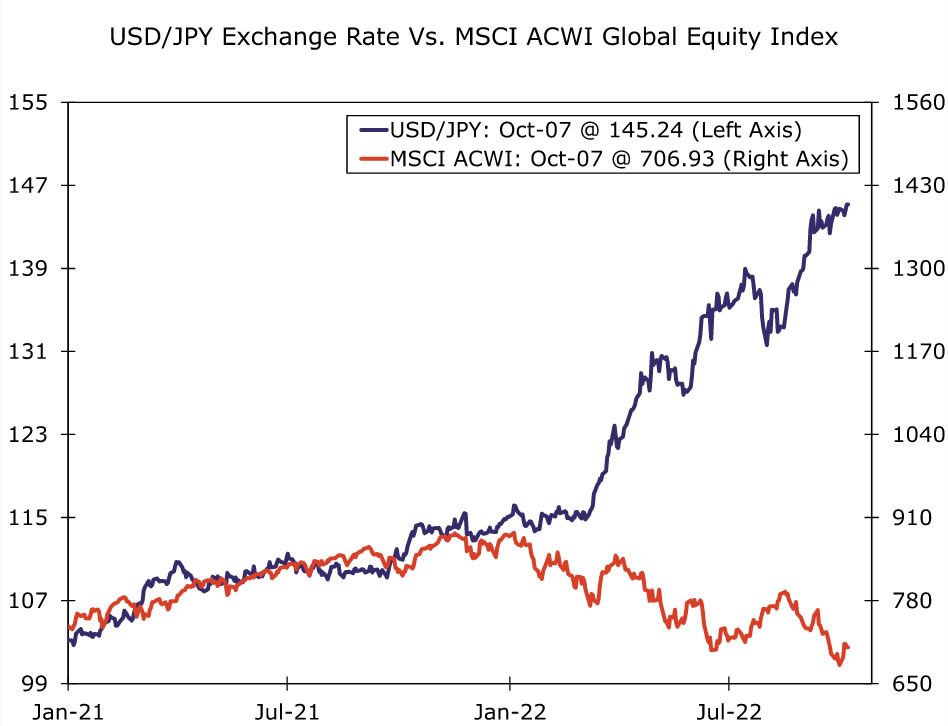

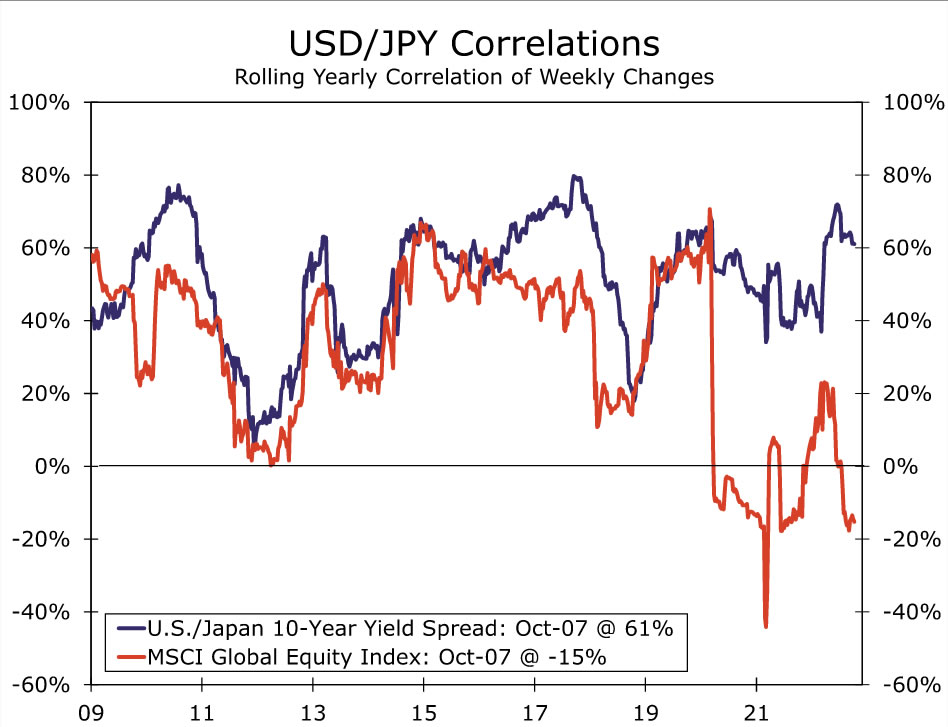

Historically, there have been two important drivers for movements in the yen. The first comes from safe haven characteristics of the currency. The second is Japan’s yield differentials with the rest of the world. Looking back at much of the past decade, both seem to be relevant influences for the currency. However, more recently, the yen’s safe haven properties seem to have diminished to some extent, while yield differentials have remained a better indicator of the yen’s potential future trend.

Safe haven investments are typically attractive during times of market volatility, and are expected to retain or gain value during times of market stress. In theory, safe haven currencies should do better when equity markets are down. To better understand the historical relationship between global equity markets and the yen, and examine the correlation between these variables over time. We used the MSCI global equity index (in local currency terms) to measure worldwide equity performance. We would expect the USD/JPY exchange rate to have a positive correlation with equity performance, with both moving in the same direction most of the time. That is, when an equity index declines, the USD/JPY exchange rate should also decline so that the U.S. dollar gets weaker and the Japanese yen gets stronger. Using weekly returns between 2010 and 2019 (prior to the pandemic), the correlation between the MSCI global equity index and USD/JPY is indeed positive at +35%. However, since the start of 2020 (essentially when the pandemic began), the correlation between equities and USD/JPY has turned negative. And indeed, weekly data since March 2022 (when the Fed first began to lift the fed funds rate) show that MSCI index returns had a negative correlation with changes in USD/JPY, with the correlation at -24%. This would imply a negative relationship between the currency pair and global equities, or in other words when equities fall, USD/JPY rises or the yen weakens against the U.S. dollar—antithetical to the characteristics of a safe haven currency. While it is not obvious why the yen’s safe haven characteristics have diminished, recent history suggests looking elsewhere for a more reliable currency driver, as the equity-yen correlation has broken down.

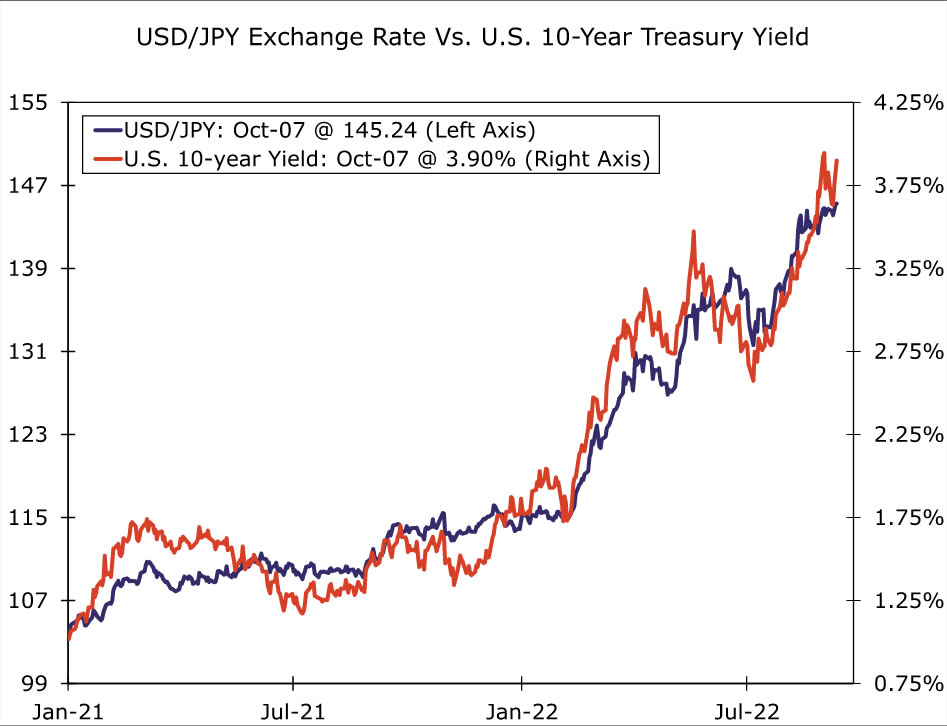

That brings us to yield differentials between the U.S. and Japan. To compare these differentials, we used the difference between the yield on the 10-year U.S. Treasury bond and the yield on the 10-year Japanese government bond (JGB). Similarly to equities, we would also expect USD/JPY to have a positive correlation with this yield spread. Given the BoJ targets a JGB yield near zero, rising U.S. yields as a result of Fed tightening should ultimately be supportive of the dollar. A stronger dollar would drive up the USD/JPY exchange rate and reflect a weaker yen. Indeed, using weekly percentage changes since 2010, the correlation between USD/JPY and the yield spread is +42%. In contrast to the yen and equities, there does not appear to have been any significant change in the relationship between the yen and yield spread during the pandemic, meaning the post-2010 correlation is representative of the historical behavior of the two variables. In our view, this yield spread, heavily influenced by BoJ and Fed policy, remains a better driver of the yen’s movements than safe haven dynamics. When looking at the correlations between the weekly percentage change of the Treasury-JGB yield spread versus USD/JPY starting in March 2022, we observe a higher correlation of +68%.

The rolling yearly correlation of weekly changes in the yield spread and the MSCI index versus USD/JPY show that the two correlations sharply diverge in 2020 and have remained apart since, a sign that safe haven characteristics of the yen may not as reliable an influence as they were pre-pandemic. Given that yield spreads appear to remain a more influential driver of the USD/JPY exchange rate, trends in global monetary policy and bond yields, especially those of the Federal Reserve and United States, should be influential for the yen. The FOMC has committed to doing “whatever it takes” to bring inflation down, and we expect the FOMC to hike the fed funds rate by 75 bps in November and 50 bps in December. Looking ahead to 2023, we expect further tightening, with 25 bps rate hikes at both the February and March meetings. If realized, the target range for the fed funds rate would peak at 4.75%-5.00% in March 2023.

In stark contrast, the Bank of Japan likely will remain comfortable with easy monetary policy for the foreseeable future. Given the increasing divergence between a dovish BoJ and tighter Fed monetary policy, the yen still has potential to weaken against the U.S. dollar in the medium term, even if the Ministry of Finance intervenes in FX markets again to support the currency. We believe that as yields continue to diverge, the yen can weaken toward a USD/JPY exchange rate of JPY149.00 by Q1-2023. However, once the United States falls into recession and given our outlook for the Federal Reserve to eventually ease monetary policy, we do subsequently see potential for the yen to strengthen heading into late 2023.

{kind=link}