Summary

- The European Central Bank (ECB) delivered another large rate hike at today’s monetary policy announcement, though its forward guidance was perhaps somewhat less hawkish than at previous recent meetings.

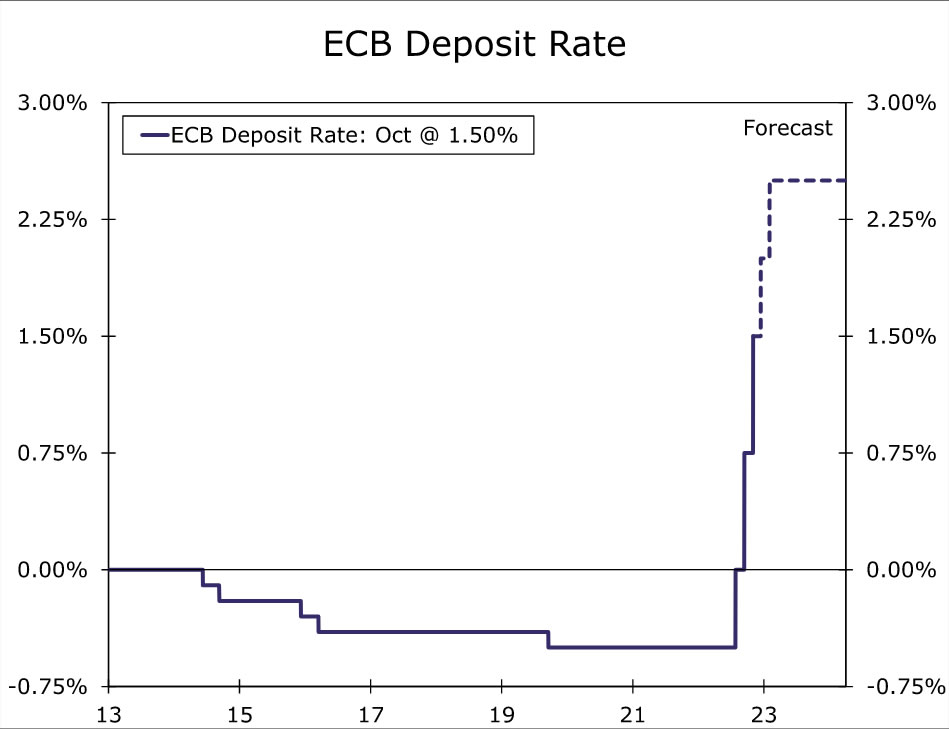

- The ECB raised its Deposit Rate by 75 basis points for a second straight meeting, to 1.50%, matching the consensus forecast. In a widely expected move, the ECB also adjusted the terms on its targeted longer-term refinancing operations, given the evolving economic circumstances and especially the surge of inflation. Going forward, the ECB will adjust the interest rates applicable on those operations from what had previously been very favorable terms.

- Overall, we view the mildly less hawkish guidance and widespread signs of a contracting Eurozone economy as consistent with a smaller 50 basis point Deposit Rate hike to 2.00% in December, especially if CPI inflation recedes to any extent in the interim.

European Central Bank Goes Big

The European Central Bank (ECB) delivered another large rate hike at today’s monetary policy announcement, though its forward guidance was perhaps somewhat less hawkish than at previous meetings. With the possibility of an ECB pivot at the meetings ahead, and with changes to long-term refinancing operations potentially impacting the profitability of European banks, today’s announcement is overall a modest negative for the euro.

The ECB raised its Deposit Rate by 75 basis points for a second straight meeting, to 1.50%, matching the consensus forecast. The central bank also raised its main refinancing rate and marginal lending rate by 75 basis points.

However, there were hints in the accompanying statement that smaller interest rate increases may not be that far away. The ECB said:

“With this third major policy rate increase in a row, the Governing Council has made substantial progress in withdrawing monetary policy accommodation. The Governing Council took today’s decision, and expects to raise interest rates further, to ensure the timely return of inflation to its 2% medium-term inflation target. The Governing Council will base the future policy rate path on the evolving outlook for inflation and the economy, following its meeting-by-meeting approach.”

The reference to “substantial” progress, as well as following a meeting-by-meeting approach, both hint at the possibility of transitioning to smaller rate increases at upcoming meetings. With reference to the economic outlook, ECB President Lagarde said growth risks were on the downside while inflation risks were on the upside.

In a widely expected move, the ECB also adjusted the terms on its targeted longer-term refinancing operations (TLTRO III), given the evolving economic circumstances and especially the surge of inflation. Going forward, the ECB will adjust the interest rates applicable on those operations from what had previously been very favorable terms. The ECB said:

“From 23 November 2022 until the maturity date or early repayment date of each respective outstanding TLTRO III operation, the interest rate on TLTRO III operations will be indexed to the average applicable key ECB interest rates over this period. The Governing Council also decided to offer banks additional voluntary early repayment dates.”

And also that:

“Finally, in order to align the remuneration of minimum reserves held by credit institutions with the Eurosystem more closely with money market conditions, the Governing Council decided to set the remuneration of minimum reserves at the ECB’s deposit facility rate.”

Finally, there were no signals from today’s announcement regarding quantitative tightening. The ECB said it intends to reinvest in full the principal payments from maturing securities purchased under the Asset Purchases Program for an extended period of time past the date when it started raising the key ECB interest rates. Regarding the Pandemic Emergency Purchase Program, the Governing Council intends to reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024. The guidance regarding quantitative tightening is unchanged from previous announcement. At the current juncture, our view remains an “in principle” decision on quantitative tightening will be announced at the ECB’s December meeting.

Overall, we view the mildly less hawkish guidance and widespread signs of a contracting Eurozone economy as consistent with a smaller 50 basis point Deposit Rate hike to 2.00% in December, especially if CPI inflation recedes to any extent in the interim. That view appears to be shared by market participants, with German two-year government yield down around 18 basis points to 1.85% since the ECB’s announcement, and with the euro also down today. If the Federal Reserve fails to pivot at its monetary policy announcement next week, the euro could see further downside in the weeks and months ahead.

{kind=link}