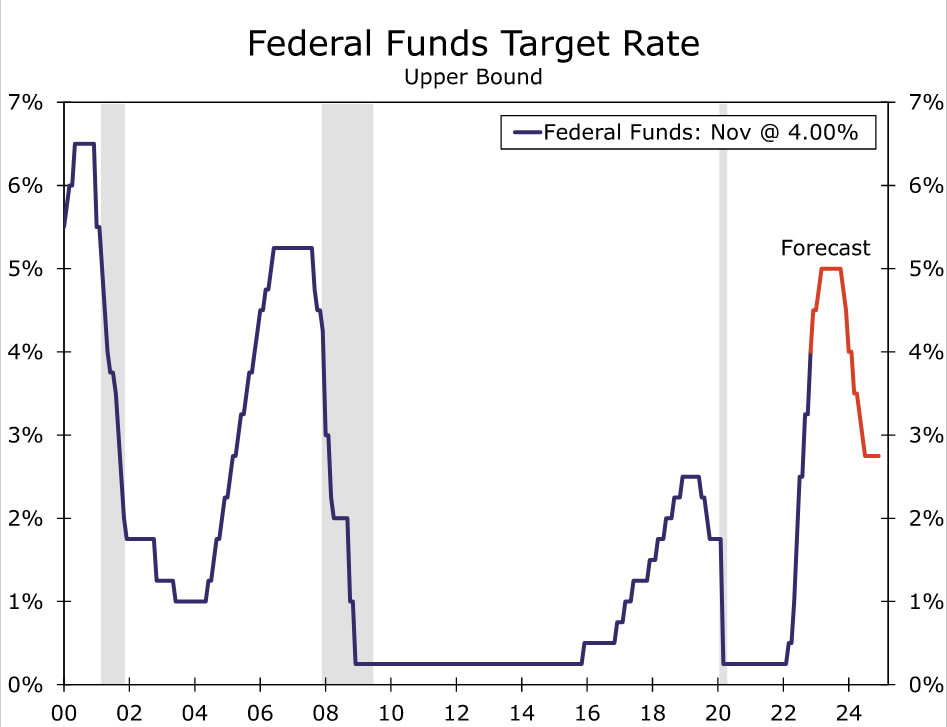

Summary

- The FOMC raised its target range for the federal funds rate by 75 bps today, which was widely expected.

- Today’s statement was very similar to the one that was released after the last meeting on September 21. That said, the FOMC noted for the first time that it will consider the cumulative degree of tightening and the lags inherent in monetary policy changes when deciding on future rate moves.

- These changes to the statement indicate to us that the Committee is prepared to slow the pace of tightening at future meetings. But Chair Powell suggested in his post-meeting press conference that the FOMC is not yet done tightening policy. Moreover, the Committee may need to raise rates higher than most members thought in September.

- In our view, the bar for another 75 bps rate hike at the December 14 meeting is fairly high. Today’s events strengthens our conviction that the Committee will deliver a 50 bps rate hike in December.

- But there are two more employment reports and two more CPI reports that will be released between now and December 14. The outcome of the December 14 meeting will depend crucially on what those data releases tell the FOMC about the state of the U.S. economy.

Source: Federal Reserve Board and Wells Fargo Economics

FOMC Is Not Yet Done, Although Pace of Future Tightening May Slow

As universally expected, the Federal Open Market Committee (FOMC) hiked rates by another 75 bps at its meeting today, bringing the target range for the federal funds rate to 3.75%-4.00%. The Committee has increased the target range by 375 bps since March, the fastest pace of tightening since the early 1980s when, much as today, inflation was viewed as Public Enemy #1.

As is customary for the first FOMC meeting of the fourth quarter, the Committee did not release a Summary of Economic Projections (SEP), in which the FOMC details its macroeconomic forecasts including the so-called “dot plot.” (The next SEP will be published at the conclusion of the December 14 meeting.) Consequently, market participants need to infer the Committee’s expectations regarding future policy moves from the published statement and Chair Powell’s press conference. In that regard, the statement that was issued today read very much like the September 21 policy statement. Specifically, the FOMC said “recent indicators point to modest growth in spending and production,” and that “job gains have been robust in recent months.” The Committee continued to describe the inflation rate as “elevated,” and it continues to anticipate that further increases in the target range for the federal funds rate will be “appropriate.” Indeed, Chair Powell noted in his post-meeting press conference that the FOMC still has “some ways to go” on tightening policy, and that the terminal fed funds rate may be higher than the 4.50%-4.75% target range that was shown by the median “dot” in the September SEP.

But the FOMC made one meaningful change to the statement, which we anticipated in our recent FOMC “Flashlight” report. Specifically, the Committee stated for the first time that it will “take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” As noted above, the FOMC has now raised rates by 375 bps since March. But rate hikes do not have an instantaneous effect, and the effects of previous tightening are still filtering into the economy. Moreover, the current target range for the fed funds rate is now at a level that most observers would consider to be “restrictive.” That is, rates are now exerting headwinds on the pace of economic activity. The economy could decelerate significantly, if not begin to contract, if the FOMC continues to tighten policy aggressively.

In our view, the use of this new clause in the statement signals that the Committee is prepared to slow the pace of tightening at future meetings. We have been forecasting that the FOMC will raise the target range for the fed funds rate by 50 bps at its December 14 meeting. Today’s developments reinforces our conviction regarding this forecast. And markets seem to agree. Market pricing prior to the news was consistent with a 40% probability of a 75 bps rate hike on December 14. As of this writing, that probability now stands at only 25%.

The FOMC does not need to make another rate decision for six weeks, which is why it mentioned “economic and financial developments” in the statement. Notably, the employment report for October is slated for release on Friday, November 4 with the November report scheduled for December 2. We will also get two more CPI reports between now and December 14 (November 10 and December 13). Continued strength in payrolls and/or higher-than-expected inflation outturns could lead the Committee to reconsider on December 14. That is, the FOMC could very well determine at that meeting that another 75 bps rate hike is “appropriate” if growth remains strong and/or inflation remains elevated.

The Committee clearly thinks it needs to tighten further and, in our view, December will not be the last meeting in this cycle at which the FOMC hikes rates. We currently look for the Committee to increase the target range for the fed funds rate by 25 bps on February 1 and by a final 25 bps on March 22. But we think the bar is currently high for another 75 bps rate hike on December 14. Although individual FOMC members will have different opinions on the appropriate pace of tightening going forward, we believe the “consensus” thinks that 50 bps on December 14 would be more appropriate than 75 bps, at least at the present conjuncture. Stay tuned.

{kind=link}