U.S. Highlights

- Results from the midterm elections showed the Democrats maintained control of the Senate but lost their majority in the House of Representatives.

- U.S. housing data continue to slide in October, with housing starts down 4.1% m/m to 1.4 million units, while existing home sales fell 5.9% m/m to 4.3 million.

- Retail sales surprised to the upside in October, rising by 1.3% m/m. Gains were relatively broad based and suggest the U.S. consumer remains on a firm footing. Real consumer spending is set to accelerate to 3% in Q4.

Canadian Highlights

- Canadian consumer price inflation held steady at 6.9% year-on-year (y/y) in October, as CPI excluding food and energy decelerated slightly to 5.3% y/y (from 5.4% y/y previously).

- Rising gasoline prices and mortgage interest costs were major contributors to inflation in October, though food prices saw an encouraging deceleration.

- Housing sales saw a surprise bounce on the month, though prices continued to decline across the country. Housing starts also declined, though remain at elevated levels.

U.S. – Consumer Resilience on a Timer

After a week of ballot counting, results from the midterm elections showed that the Democrats maintained control of the Senate but lost their majority in the House of Representatives. With the Republican’s now having narrow control of the House, we have returned to a divided Congress, limiting prospects of new legislation over the next two years.

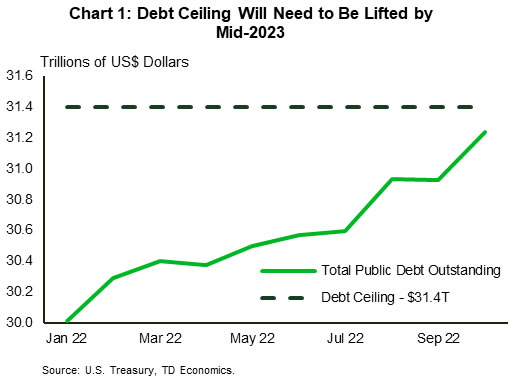

A partisan Congress raises the odds of another government shutdown or debt-ceiling showdown at some point next year (Chart 1). We could get a firsthand glimpse of what’s to come as early as next month when the current ‘continuing resolution’ funding government spending expires on December 16th. At a minimum, Congress will need to negotiate another short-term patch to keep the federal government open. The other challenge that will come up in the coming months is the need to raise the debt-ceiling. Fortunately, the U.S. Treasury is estimated to have enough wiggle room in its existing cash holdings to fund the government through at least mid-2023.

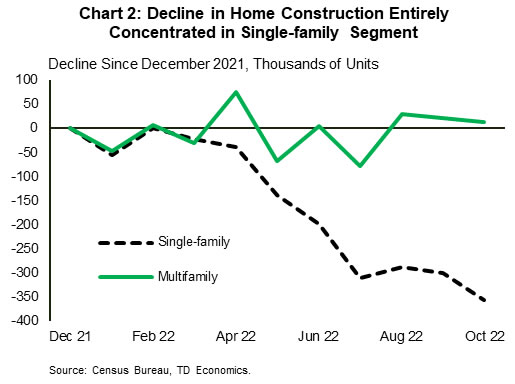

Looking to this week’s economic data, the impact of higher interest rates continued to tighten its grip on the housing sector. New home construction fell 4.2% m/m to 1.4 million units in October and is now down 19.4% since the beginning of the year. While the pullback continues to be concentrated across the single-family segment, the recent plateauing in multifamily permits suggests it too has peaked (Chart 2). Things look even more dire in the resale market. Mortgage rates reached 7.2% in October, and sales fell by another 5.9% m/m to 4.3 million and are now (outside of the pandemic lockdown period) at the lowest level since 2011. Inventory has remained tight so far and so the impact to prices has been small, with the median home price down just 3.5% from its peak. Because most homeowners hold mortgages originated at rates lower than today’s prevailing rate, listings are unlikely to spike like during the last housing crisis. As a result, the market will remain undersupplied for some time, limiting the downside pressure on prices.

In stark contrast to the housing sector, the U.S. consumer continued to show considerable staying power in October. Retail sales came in much better than expected, rising by 1.3% m/m. Indeed, some of the strength in October was already telegraphed earlier in the month when new vehicle sales jumped 10% m/m to 14.9 million units. However, even after stripping out autos, sales at gasoline stations, and building materials, the ‘control’ measure still rose by a healthy 0.8% m/m.

After incorporating the October retail sales data, our current tracking for Q4 GDP sits at 2.2%, with consumer spending expected to expand by 3%. This is an acceleration from Q3 and underscores the degree of resilience we’re still seeing from the U.S. consumer. However, it would be a stretch to believe that the rapid adjustment in interest rates won’t eventually take a toll. Let’s not forget, the Fed still has ‘a ways to go’ before even reaching its terminal rate. Moreover, it can take anywhere from 12-18 months to feel the full effect of higher interest rates. By this logic, we expect a broader demand adjustment to begin early next year, with growth expected to fall to a stall-speed in 2023.

Canada – Gasoline Prices Keep Inflation Burning

It was a busy week for Canadian economic data. With inflation showing more persistence in October’s Consumer Price Index (CPI) data, Canadian yields rose across the curve on expectations that the Bank of Canada (BoC) will have to raise rates even more than previously thought. Adding to this was the release of housing data, which showed a surprise uptick in overall real estate sales activity even though prices continued to fall. Housing starts also declined, though remain at elevated levels.

Wednesday’s release of the Canadian Consumer Price Index was the main event this week. As expected, the headline index reaccelerated by 0.6% month-on-month (m/m), from 0.4% m/m in September and effectively no price change in August. October’s gain was largely attributed to the 9.2% m/m rise in gasoline prices, which caused CPI in year-on-year (y/y) terms to hold steady at 6.9%. Though the November tracking of gasoline prices indicates that this surge has abated, it goes to show how sensitive Canadian inflation is to externally driven products like gasoline.

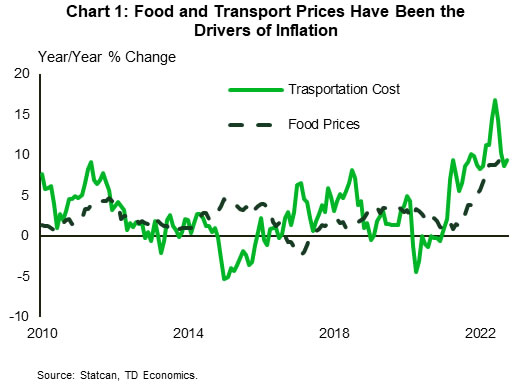

Food prices have also been a key source of inflation this year, and consumers got a bit of relief in October as prices decelerated to a 0.4% m/m gain. That is less than half the nearly 1% monthly average price increase that Canadian’s have had to eat over the last eight months! Though this is moving in the right direction, the overall food basket remains elevated, up 10.1% over the last year (Chart 1).

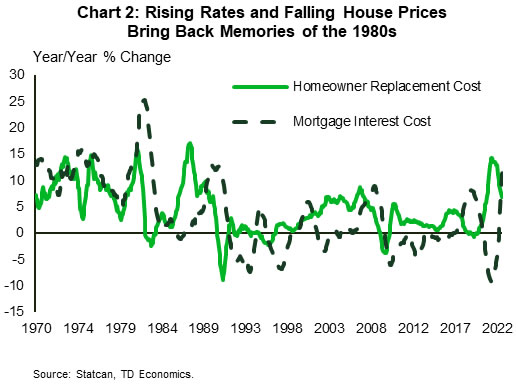

The other major category in focus was the rising price of shelter, which showed a large 0.8% m/m increase, translating to 10.8% y/y. Given the BoC’s aggressive rate hikes over 2022, mortgage interest costs have risen over 11% y/y and are set to surge further as homeowners renew their mortgages at higher rates in the coming months (Chart 2). The drop in house prices (homeowners’ replacement costs to be specific) has provided some offset . This previous source of inflationary pressure is likely to be deflationary over 2023. This trend was apparent in the recently released housing sales data. Though house sales increased for the first time in eight months (+1.3% m/m), the average house price dropped 0.6% m/m and is now down over 9% y/y.

The acceleration in overall inflation was a setback, but there are underlying trends in place that should cause inflation to decelerate in the coming months. Slowing global demand is expected to put further downward pressure on energy prices and rapidly declining shipping costs, the main drivers of high food and fuel inflation over the last year (assuming no new shock) should contribute to lower inflation in the coming months. The wildcard here is housing. There are significant lags from the impact of interest rate changes into CPI. With the BoC set to raise rates to 4% or higher in the coming months, it not only needs to assess the impact on economic growth, it is also needs to consider how its actions may continue to push shelter inflation even higher.

{kind=link}