Following a hawkish ECB in December, market participants may be eagerly awaiting the preliminary Euro area inflation numbers, due out on Friday at 10:00 GMT, as they try to assess whether more 50 basis points worth of rate hikes are indeed warranted. Will the data confirm the ECB’s aggressive stance? And how may the euro react?

Appearing in a hawkish suit

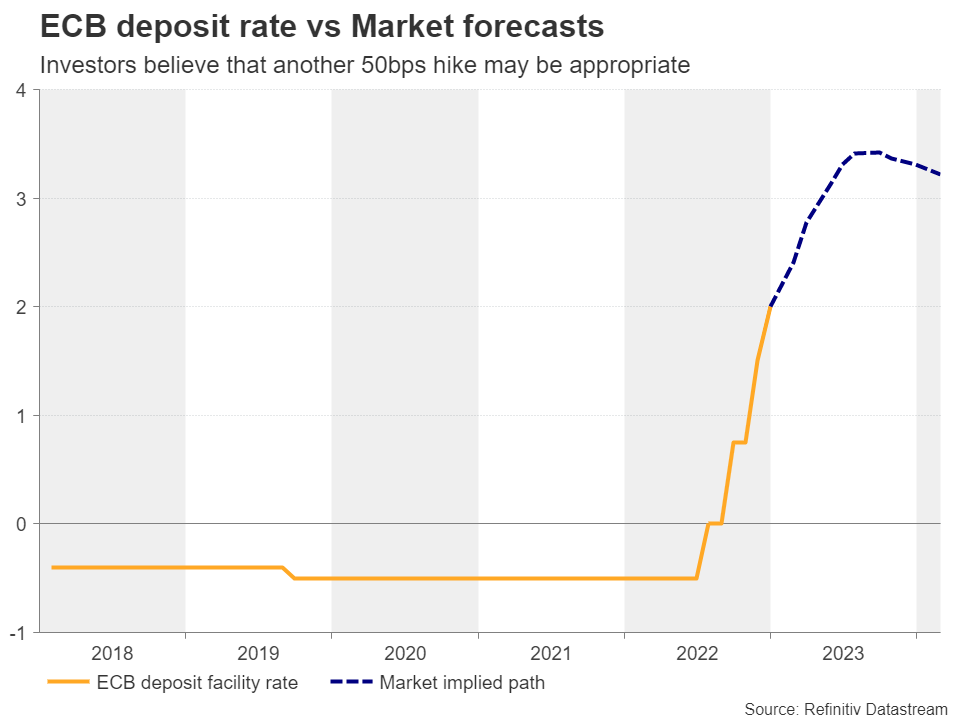

At its last meeting for 2022, the European Central Bank raised interest rates by 50bps after delivering two consecutive triple hikes in September and October. Though the slowdown was generally expected, at the press conference following the decision, President Lagarde appeared surprisingly hawkish. “Anybody who thinks this is a pivot for the ECB is wrong,” she said, adding that interest rates are likely to continue being raised at a 50bps pace for a period of time. That Bank also laid out a plan to start unwinding its bond holdings from March, another step towards tighter policy.

Another 50bps hike is almost fully priced in

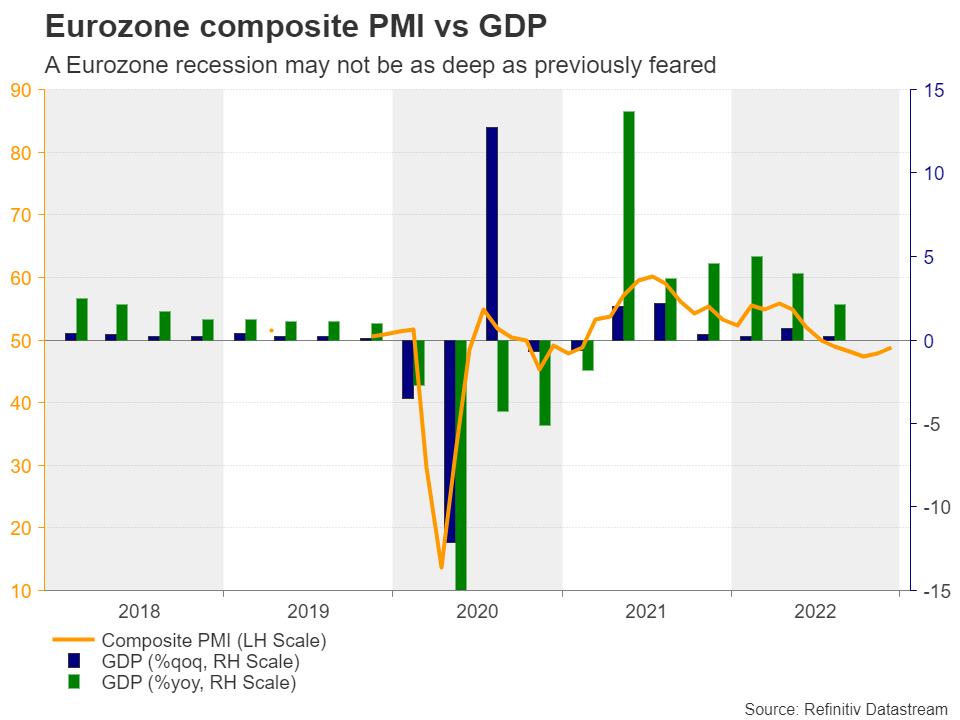

Just the next day, the preliminary PMIs for the month, despite staying in contractionary territory, improved by more than expected, with the surveys pointing to a reduced loss of orders, improving supply conditions, lower price pressures and an uplift in business confidence. Commenting on the flash data, the chief business economist at S&P Global Market Intelligence said that “While the further fall in business activity in December signals a strong possibility of recession, the survey also hints that any downturn will be milder than thought likely a few months ago.”

Combined with more hawkish remarks by ECB policymakers in the aftermath of the meeting, the PMIs may have prompted investors to believe that another 50bps hike at the February gathering is a nearly done deal. It is worth mentioning that on New Year’s Eve, President Lagarde noted that wages are growing faster than previously expected, something the Bank must prevent from adding to already-elevated inflation, while a few days earlier, ECB member Klaas Knot said that until July, the Bank would achieve a decent pace of tightening through half percentage point rises.

Inflation to slow but stay elevated

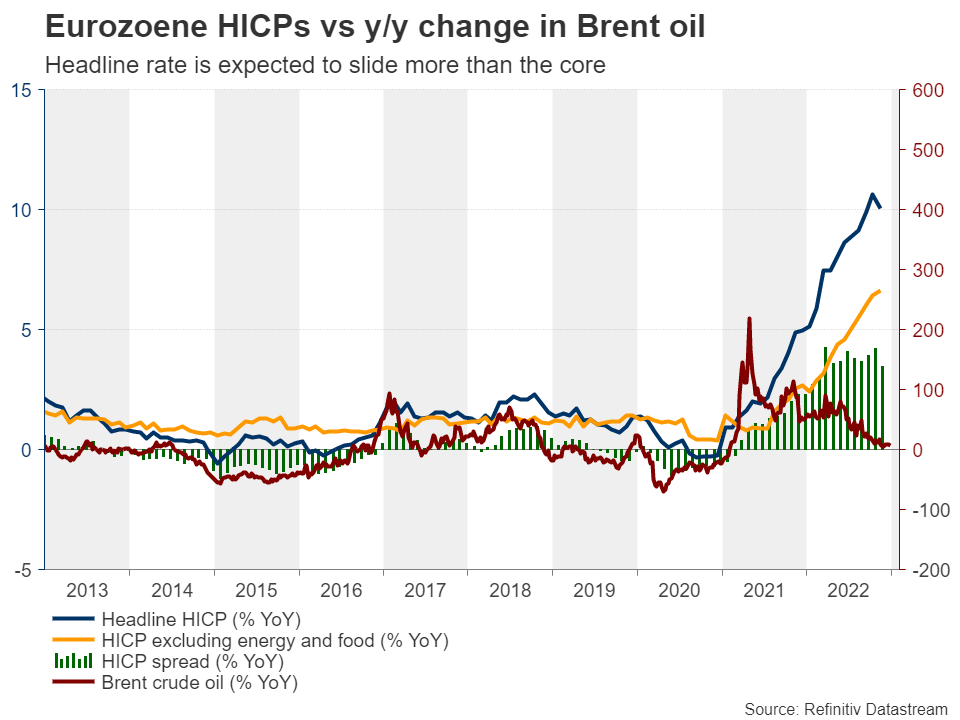

Friday’s data is expected to show that Eurozone’s headline harmonized index of consumer prices slowed further to 9.7% y/y in December from 10.1%, while the core rate is forecast to have ticked down to 6.5% y/y from 6.6%.

With underlying inflation not expected to have cooled much, the decent slide in the headline rate may be partly owed to the slide of the yearly change in oil prices. That change may turn negative in February or March as the war-related rally is thrown out of the year-on-year calculation, which could drag headline inflation even lower. However, should underlying inflation stay at levels more than triple the ECB’s objective, policymakers may have no other choice than keep delivering more double hikes. Despite their latest slowdown, producers’ prices remain extremely high, supporting the view that core consumer prices could stay elevated for longer.

Euro may be destined to trade north

Even if the euro corrects lower due a further slide in headline inflation, a still-elevated underlying metric could keep the losses limited and short-lived. Combined with a 70% probability for a further slowdown in Fed rate hikes to 25bps at its upcoming gathering and bets of nearly two quarter-point cuts by the end of the year, expectations that the ECB will continue with double hikes may result in a rebound in euro/dollar.

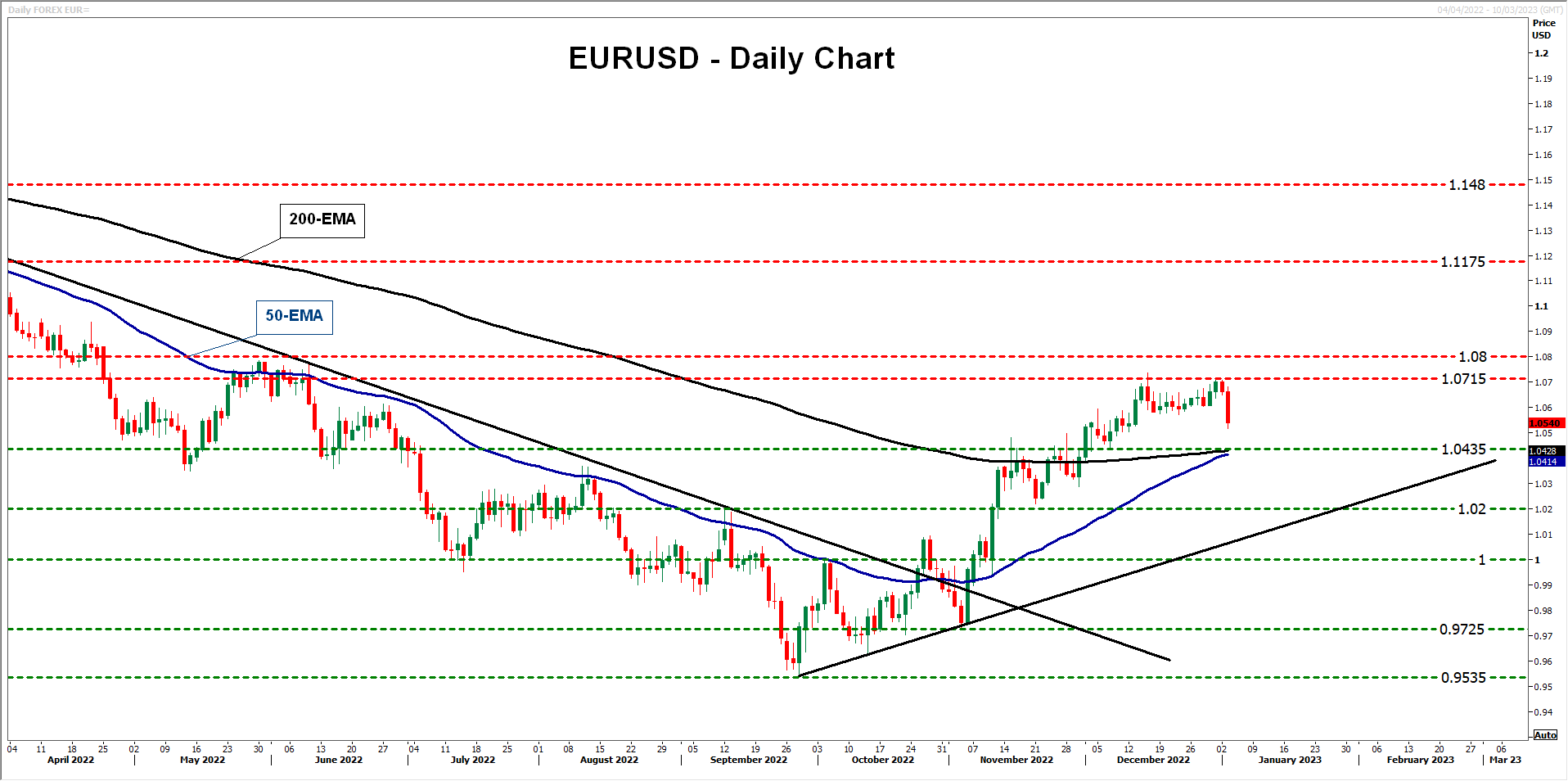

From a technical standpoint, the pair is trading above a prior downtrend line taken from the high of February 10, above a shorter-term upward sloping line drawn from the low of September 28, and above both the 50- and 200-day exponential moving averages (EMAs). Despite the strong setback on Tuesday, this keeps chances for a rebound well on the table.

With no clear catalyst to justify the strengthening of the dollar on Tuesday, the bulls may be tempted to re-enter the action from near the 1.0435 territory. Even if that zone breaks, they may have another opportunity at around 1.0200. A potential rebound could result in another test within the key resistance zone between 1.0715 and 1.0800, the break of which could add to the bullish narrative and may allow advances towards the peak of March 31, at around 1.1175.

Flipping the coin, should underlying inflation in the Euro area start easing fast, the euro could come under selling interest on speculation that the ECB may further scale down its rate increments. Euro/dollar could fall even more if the ECB is seen as turning more dovish than the Fed. The move signaling that the bears are back in control may be a break back below parity. Such a dip would take the pair below the short-term uptrend line and may initially target the 0.9870 zone. If that line doesn’t hold, the pair could fall to 0.9725, or even all the way down to its 20-year low of 0.9535, hit on September 28.

{kind=link}