With some Fed officials corroborating investors’ view of a quarter point increase, Wednesday’s FOMC gathering will likely be among the highlights of the week. Market participants will be eager to find out whether the consensus of policymakers also agrees with their view on the path of interest rates after the meeting, as this is where opinions between the financial community and the Fed diverge. What will the Fed signal and how may the market respond?

A bone of contention

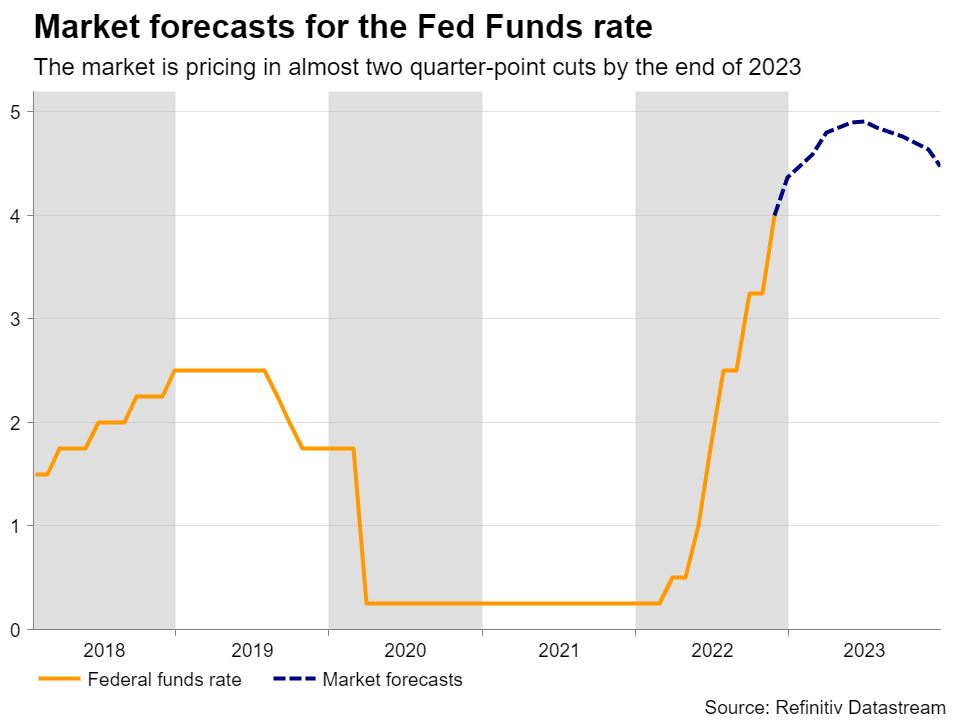

At their last meeting for 2022, Fed officials raised interest rates by 50bps after four consecutive 75bps hikes. However, despite the smaller increment, they sang a hawkish song, with the gist of the lyrics being that interest rates may rise above 5%, while Fed Chair Powell’s solo part at the press conference intended to push back against pivot expectations.

Since then, even if some policymakers admitted that shifting to a lower gear at the upcoming gathering may be appropriate, most of them have been adamantly sticking to their guns that interest rates will probably rise to slightly above 5%, in line with the December “dot plot”, and that they will stay there for a prolonged period thereafter. However, this has been a bone of contention as the market insists that interest rates are likely to rise to the 4.75-5.00% range, and that 50bps worth of rate cuts may be warranted by the end of the year.

Market keeps gaze locked on data

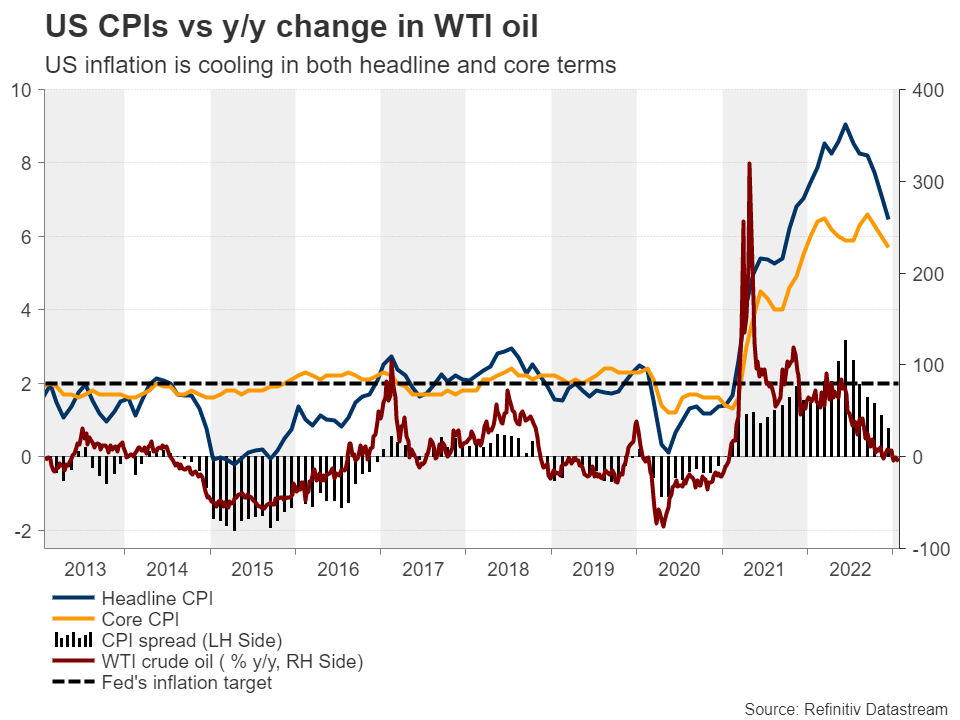

It seems that investors overly rely on economic data rather than the Fed communication, and especially the steady cooling of inflation. In December, the headline CPI slowed for the sixth straight month, with the core rate dropping as well, confirming the view that inflation may be on a sustained downtrend.

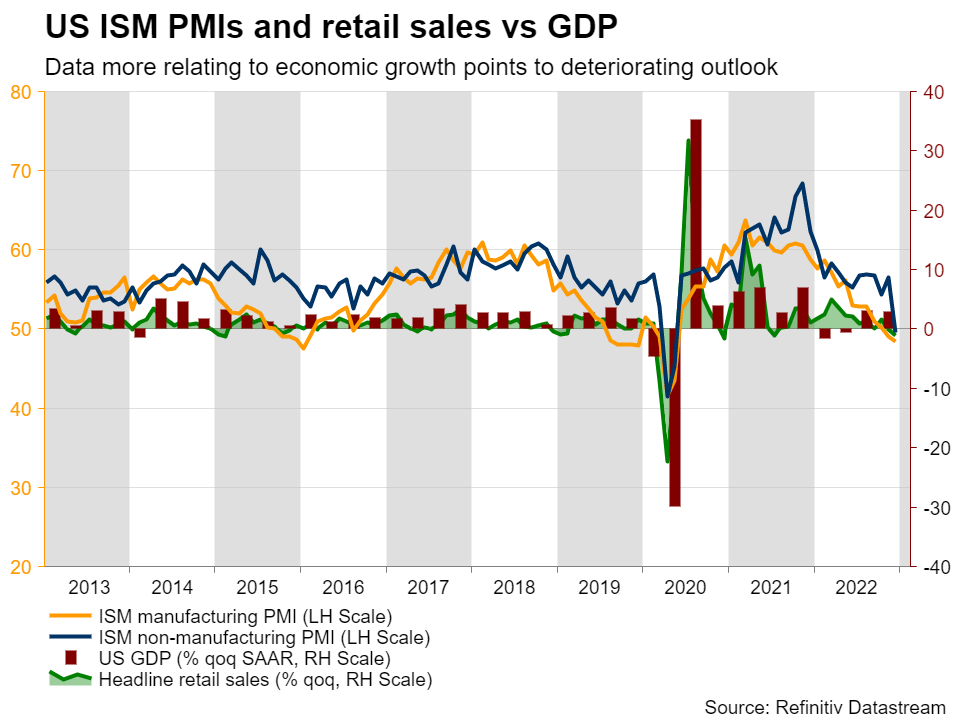

Furthermore, retail sales for December recorded their biggest drop in 12 months, a strong sign of deteriorating consumer demand, which could bring inflation further down in coming months but also adds to recession fears, especially after the ISM non-manufacturing PMI for December fell into contractionary territory for the first time since May 2020. Coming on top of the further contraction in the manufacturing sector, a shrinking service sector (which accounts for around 77.6% of US GDP) is anything but encouraging. Yes, the preliminary S&P Global PMIs for January suggested some improvement but still stayed below the boom-or-bust zone of 50.

On Friday, after the Fed decision, the employment report for December is expected to reveal a slowdown in job gains, but with the unemployment rate staying close to its five-decade low and wages accelerating, it would reflect a still-tight labor market, which may be the only argument in favor of the Fed’s narrative.

Dollar could gain, but not out of the woods yet

Recent history has shown that market participants are willing to sell dollars aggressively when data enhances their pivot view, but they are not buying with the same excitement when economic releases surprise to the upside.

Thus, even if the Fed continues to signal that interest rates are likely to rise above 5%, and even if Fed Chair Powell pours more cold water on rate-cut expectations at the press conference following the decision, the dollar is unlikely to skyrocket. It could rebound somewhat and perhaps extend its gains in the case of a solid NFP report, but with the first sign pointing to deeper economic wounds, investors may re-initiate short positions. That’s why dollar traders may pay even more attention to the ISM non-manufacturing PMI for January which is scheduled to be released on Friday after the NFPs. Another month of contraction could well weigh on the dollar, while a rebound back above 50 as the forecast currently suggests may extend a potential corrective rebound for a while longer.

An overly hawkish ECB on Thursday, confirming expectations of more 50bps rate increments beyond February, could also limit any dollar strength, as euro/dollar is by far the largest component of the index, with a 57.6% weigh.

The technical picture corroborates that view

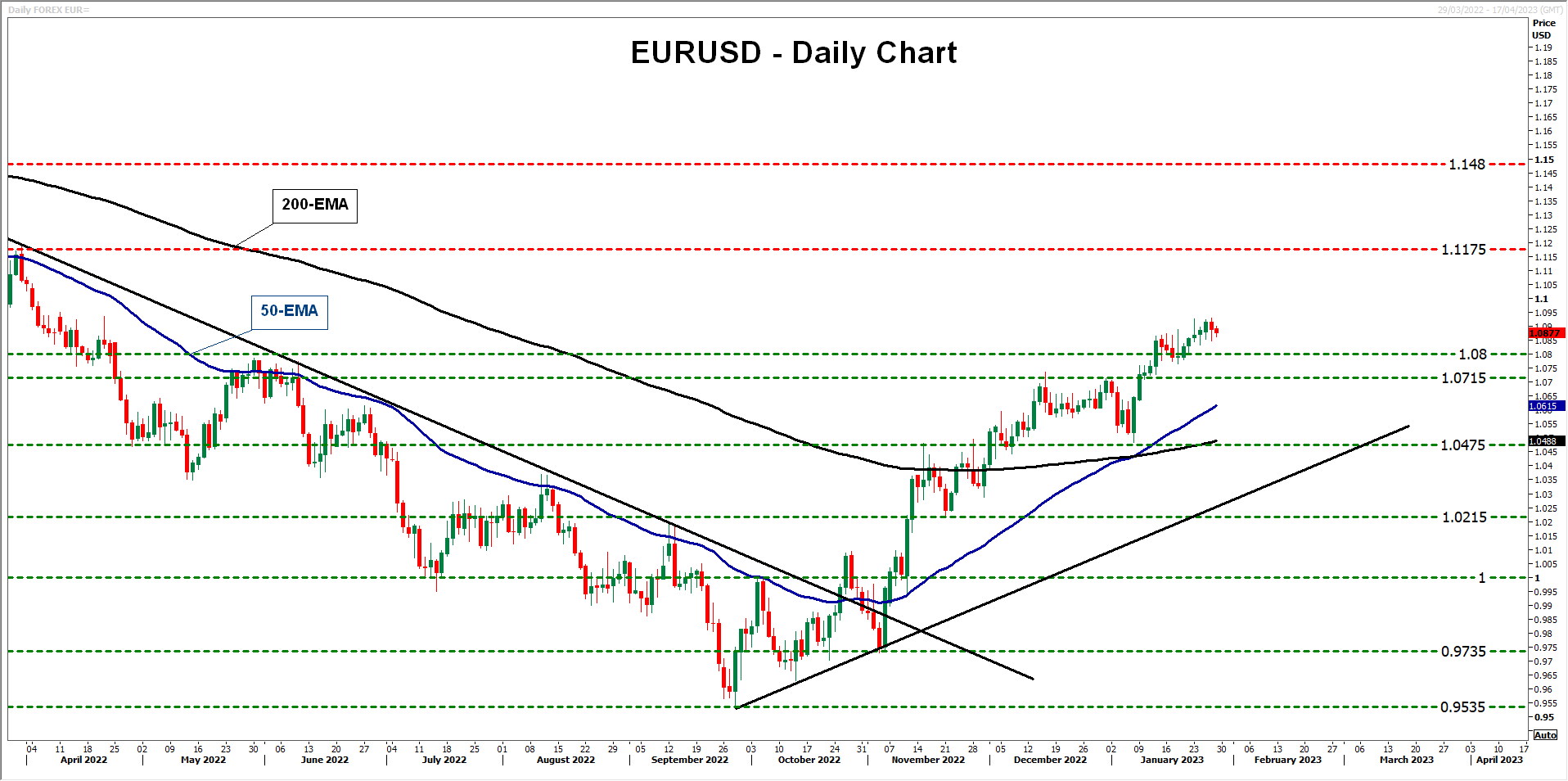

Should this week’s agenda end up net positive for the US dollar, euro/dollar could pull back and perhaps retest the 1.0715-1.0800 zone as support. Even if it breaks below 1.0715, the pair would still be trading above the uptrend line drawn from the low of September 9, which might keep the door open for a rebound.

If indeed the bulls regain control in the not-too-distant future and drive the price back above 1.0800, they may push it all the way up to the 1.1175 zone, defined as resistance by the high of March 31. That zone also acted as support between November 2021 and February 2022. For the outlook of euro/dollar to be considered bearish, the bears may need to be strong enough to dive below 1.0215, as this is the move that could solidify a potential dip below the aforementioned uptrend line.

{kind=link}