Summary

- As universally expected, the FOMC raised its target range for the federal funds rate by 25 bps at the conclusion of its policy meeting today. But the tightening cycle likely is not over yet as the FOMC noted that it “anticipates that ongoing increases in the target range will be appropriate.”

- The FOMC said that “inflation has eased somewhat,” which Chair Powell reiterated in his post-meeting press conference. But he also noted that the Committee “has more work to do” in terms of monetary tightening to bring inflation back to the FOMC’s target of 2% on a sustained basis. Powell also stated that policy will need to be restrictive for some time.

- We look for the FOMC to hike the fed funds target rate by 25 bps each at its next two policy meetings. That said, we do not have a high level of conviction regarding the exact amount of tightening that the Committee will need to deliver. The FOMC is in the fine-tuning stage of its tightening cycle, and future rate hikes will depend on incoming data in coming weeks and months.

- We have a higher degree of conviction around our belief that policy will need to remain restrictive for quite some time to bring inflation back to 2%. We forecast that the FOMC will not begin easing policy until early 2024.

- Stock and bonds rallied after Powell said that the disinflationary process appears to have started without any material weakening in the jobs market. It appears that market are buying into (hoping for?) the “soft landing” scenario.

“We Have More Work To Do”

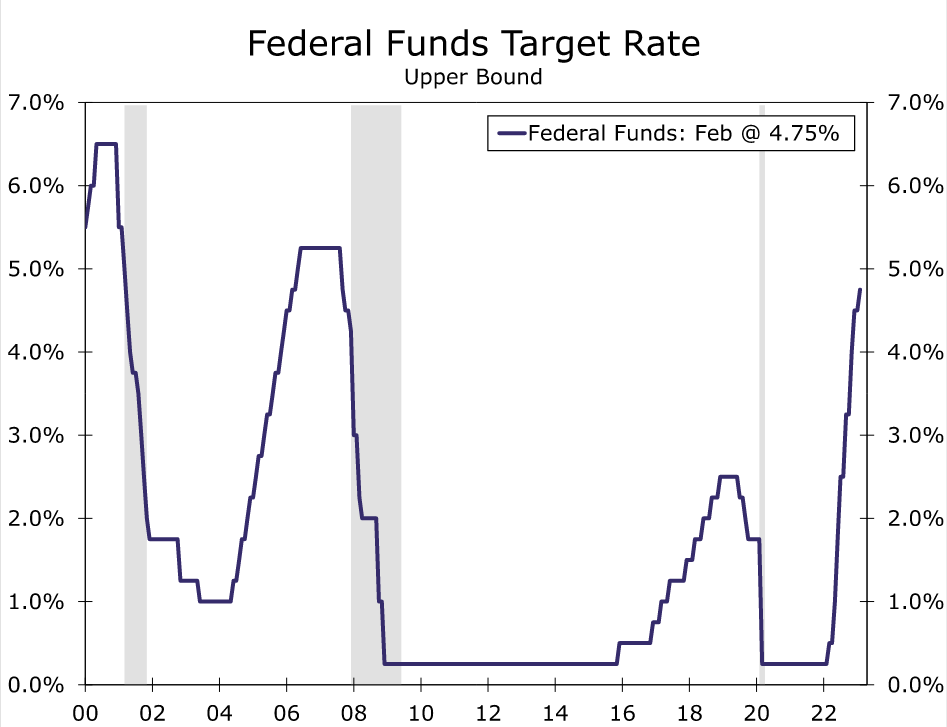

As universally expected, the Federal Open Market Committee (FOMC) unanimously agreed to raise its target range for the federal funds rate by 25 bps at the conclusion of its policy meeting today. The target range is now 4.50%-4.75%, which is 450 bps higher than where it was when the FOMC started its tightening cycle last March (chart).

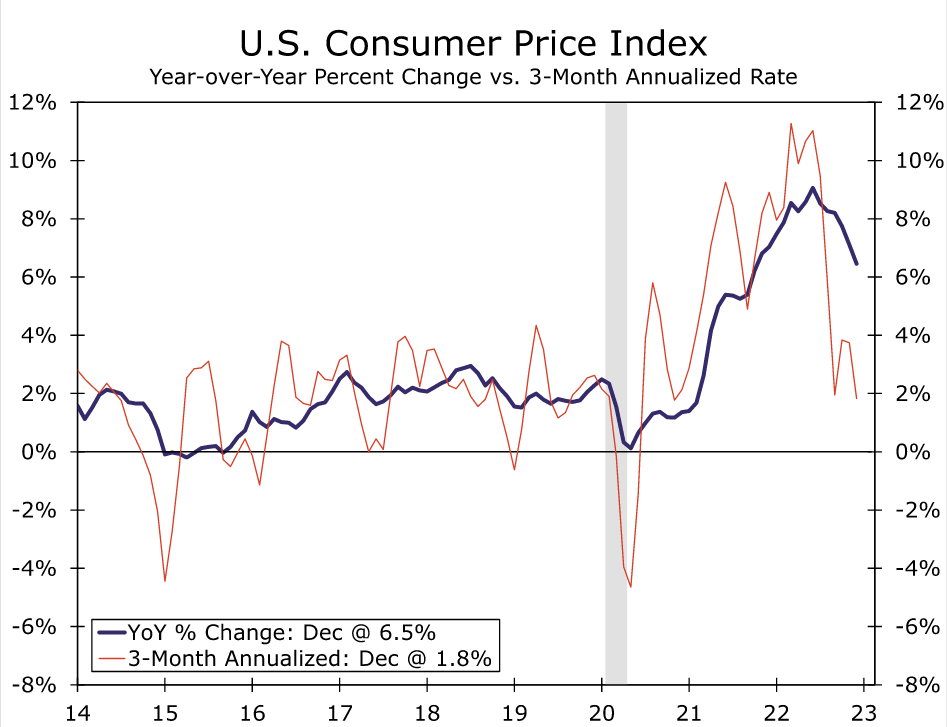

In announcing today’s move, the Committee noted that growth in spending and production appears to have been “modest” recently. Despite “modest” growth, “jobs gains have been robust in recent months, and the unemployment rate has remained low.” In short, the labor market remains tight in the Committee’s view. The statement noted that “inflation has eased somewhat.” The use of the verb “ease” is an acknowledgement of the deceleration in the consumer price index that has occurred in recent months on both a headline and core basis (chart). That said, the Committee chose to qualify “ease” with “somewhat,” and the statement continues to state that inflation remains elevated. In short, it would be premature to declare victory over inflation. In his post-meeting press conference, Chair Powell noted that the disinflationary process has started, but he also said that there are some sectors, notably in the broad service sector, where the Fed is not yet seeing signs of price moderation. Indeed, Powell explicitly stated that “we have more work to do.”

Policy Will Need To Be Restrictive For Some Time

The policy statement continued to note that “The Committee anticipates that ongoing (emphasis ours) increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” This sentence is a clear indication that further tightening likely lies ahead. In that regard, the FOMC authorized the continued reduction in the size of the Fed’s balance sheet via the roll-off of up to $60 billion worth of Treasury securities per month and up to $35 billion worth of mortgage-backed securities. Shrinkage in the size of the Fed’s balance sheet acts as another form of monetary tightening.

We look for the FOMC to hike the fed funds rate by 25 bps at each of its next two meetings on March 22 and May 3, which would bring the target range for the fed funds rate to 5.00%-5.25%. That said, we do not have a high level of conviction regarding the exact amount of further tightening that the FOMC will deliver. The Committee is in the fine-tuning stage of its tightening cycle, and the number of remaining rate hikes will depend on incoming economic data in coming weeks and months. We have a higher degree of conviction, however, in our belief that the FOMC will not be quick to ease policy. Committee members appear to be united in their view that inflation remains too high, and that policy will need to be restrictive in order to bring inflation back to the FOMC’s target of 2% on a sustained basis. In his press conference, Powell characterized the labor market as “extremely tight,” and he stated that policy will need to be “restrictive for some time (emphasis ours).” Although the end of the FOMC’s tightening cycle may be pulling into sight, after another rate hike or two, we believe there is a long way to go before the Committee begins to ease policy. In that regard, we do not look for rate cuts to begin until early 2024.

We look for the U.S. economy to slip into a mild recession this year, although we acknowledge that the Fed could potentially still pull off a “soft landing” in which inflation returns to 2% without a significant retrenchment in the labor market. In that regard, stocks and bonds rallied on Powell’s comment that the disinflationary process has started without notable weakening in the labor market. It appears that markets are increasingly buying into (hoping for?) the “soft landing” scenario.

{kind=link}